MNI ASIA OPEN: Data Disappoints, Trump to Fire BLS Admin

EXECUTIVE SUMMARY

- MNI FED: Bowman, Waller Cite Labor Concerns In Fed Dissents

- MNI BRIEF: Fed Hammack: Jobs Bear Watching, Inflation To Rise

- MNI FED: Bostic Still Sees Only One Cut This Year Despite Significant Jobs Data

- MNI US-RUSSIA: Trump Positions Two Nuclear Subs in Response to Medvedev Statements

- MNI US: Trump To Fire BLS Payrolls Head After Weak Jobs Report (Truth Social)

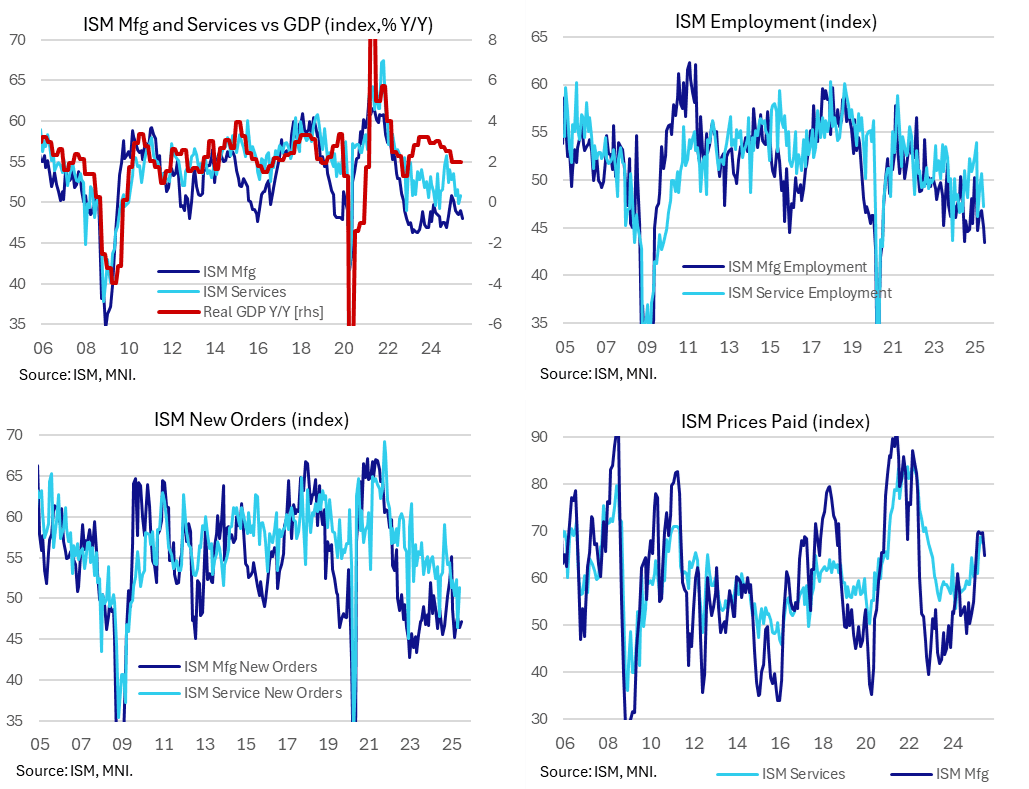

- MNI US DATA: ISM Manufacturing Weak Across The Board In July

- MNI US DATA: Huge Downward Revisions For Payrolls Set The Tone

US

MNI FED: Bowman, Waller Cite Labor Concerns In Fed Dissents

Federal Reserve governors Michelle Bowman and Christopher Waller said Friday that they voted against the central bank’s "wait and see" rate policy this week because upside risks to price stability have diminished and it was time to proactively hedge against further weakening in the economy and the risk of damage to the labor market. In separate statements, the two governors said inflation is moving closer to the central bank's 2% target and cited increased concerns about the Fed's employment mandate.

MNI BRIEF: Fed Hammack: Jobs Bear Watching, Inflation To Rise

"Disappointing signs" in the July jobs report bear careful watching, but the U.S. labor market remains largely in balance, Federal Reserve Bank of Cleveland President Beth Hammack said Friday after Bureau of Labor Statistics data showed a sharp slowdown in hiring over the past few months. "It looks like a healthy labor market that's still well in balance, but with some disappointing signs that we should watch very carefully," she told Bloomberg Television. Asked about a possible rate cut in September, she noted there are more data to come and, "I walk into every meeting with an open mind."

MNI FED: Bostic Still Sees Only One Cut This Year Despite Significant Jobs Data

Atlanta Fed’s Bostic (non-voter) speaking on CNBC notes the significant revisions in today’s nonfarm payrolls report but warns that the Fed still needs to determine what the trend of hiring will be. He hasn’t changed his view on rates and still expects one cut this year.

NEWS

MNI US-RUSSIA: Trump Positions Two Nuclear Subs in Response to Medvedev Statements

Trump: "Based on the highly provocative statements of the Former President of Russia, Dmitry Medvedev, who is now the Deputy Chairman of the Security Council of the Russian Federation, I have ordered two Nuclear Submarines to be positioned in the appropriate regions, just in case these foolish and inflammatory statements are more than just that. Words are very important, and can often lead to unintended consequences, I hope this will not be one of those instances. Thank you for your attention to this matter!"

MNI US: Trump To Fire BLS Payrolls Head After Weak Jobs Report (Truth Social)

Trump: "I was just informed that our Country’s “Jobs Numbers” are being produced by a Biden Appointee, Dr. Erika McEntarfer, the Commissioner of Labor Statistics, who faked the Jobs Numbers before the Election to try and boost Kamala’s chances of Victory. This is the same Bureau of Labor Statistics that overstated the Jobs Growth in March 2024 by approximately 818,000 and, then again, right before the 2024 Presidential Election, in August and September, by 112,000. These were Records — No one can be that wrong? We need accurate Jobs Numbers. I have directed my Team to fire this Biden Political Appointee, IMMEDIATELY."

MNI SWITZERLAND: Gov't Does Not Expect 39% Tariffs To Hit Pharma Sector

A spox for the Federal Department of Economic Affairs has told Reuters that the gov't does not expect the 39% 'reciprocal' tariffs to come into effect from 7 August on Swiss exports to the US to include the pharmaceuticals sector. The 39% rate puts Switzerland among the most heavily-penalised nations worldwide under the 'reciprocal' tariff regime, behind only Brazil (with whom's leader US President Donald Trump is involved in a bitter verbal spat), Syria, Laos and Myanmar.

MNI INDIA: US Team To Visit For FTA Talks 24 Aug As 25% Tariffs Confirmed By Trump

Reuters reports that according to an unnamed gov't source, the Indian gov't has engaged with the US for further trade talks, with a US delegation set to visit Delhi on 24 August. These will be the sixth round of talks on a formal bilateral trade agreement, with NDTV reporting in late July that an announcement on an interim deal could be announced as soon as September or October.

- Reuters source also claims that the gov't expects around USD40bln of Indian exports to be hit by the US' 25% 'reciprocal' tariffs confirmed by President Donald Trump on 31 July, and set to come into force by 7 August. The Trump administration has also indicated an "unspecified penalty" on India for continuing its purchases of Russian hydrocarbons.

US TSYS

MNI US TSYS: Tsys Gap Higher on Weak Jobs Data, Rate Cut Pricing Surges

- Treasury futures gapped higher after lower than expected jobs gain for July, June gains sharply down-revised, while unemployment rate held steady.

- Nonfarm payrolls growth was weaker than expected in July at 73k (cons 104k) after huge downward revisions in both June (-133k to just 14k) and May (-125k to 19k). The downward revisions came from a combination of large shifts in both private and public payrolls, equally spread over both May and June.

- Treasury futures extending highs (TYU5 +1-03 112-05) after lower than expected ISMs, lower UofM sentiment while 1Y inflation expectations climbs slightly. The ISM manufacturing survey was weaker than expected in July at 48.0 (cons 49.8) after 49.0 in June, falling to its lowest since October. Prices paid saw the largest downside surprise, falling to 64.8 (cons 70.0 from 8 responses vs 60 for the headline) from 69.7 in June for its lowest since February.

- Tsy Sep'25 10Y futures continued to extend highs in late trade (112-07.5), next level in focus at 112-12+ High Jul 1 and a bull trigger.

- Headline risk at least partially discounted: Pre Trump said to deploy two nuclear submarines due to provocative statements of the Former President of Russia, Dmitry Medvedev. Trump to fire "Biden Appointee, Dr. Erika McEntarfer, the Commissioner of Labor Statistics" for today's soft employment data.

OVERNIGHT DATA

MNI US DATA: Huge Downward Revisions For Payrolls Set The Tone

Nonfarm payrolls growth was weaker than expected in July at 73k (cons 104k) after huge downward revisions in both June (-133k to just 14k) and May (-125k to 19k). The downward revisions came from a combination of large shifts in both private and public payrolls, equally spread over both May and June.

MNI US DATA: Unemployment Rate Technically At Recent High But Largely Rangebound

On the household survey side of the payrolls report, the unrounded unemployment rate bounced from a surprise decline to poke to a new cycle high in July at 4.248%. An abrupt slowdown in labor supply is helping keep this rate from breaking more materially out of the recent range however, with the rate still for now quite comfortably below the 4.5% the median FOMC participant forecast for 4Q25. As posted shortly after the release, the unrounded unemployment rate came in on the high side in July at 4.248% (cons 4.2 with a few looking for 4.1).

MNI US DATA: Another Participation Rate Decline Helps Limit U/E Rate Increase

The participation rate surprisingly declined a little further in July, helping limit the unemployment rate climb on the month. The underemployment and 25-54 unemployment rates both increased on the month but remain just below cycle highs unlike the overall unemployment rate which poked above May’s latest high. The rise in the unemployment rate in July came along with the participation rate surprisingly falling further to 62.22% (cons 62.3%) after 62.28% in June for its lowest since late 2022.

MNI US DATA: ISM Manufacturing Weak Across The Board In July

The ISM manufacturing July release was weaker than expected across the board, with prices paid pulling back from receive highs, new orders chalking up a sixth consecutive monthly in contraction territory and the employment index at the lowest since mid-2020.

- The ISM manufacturing survey was weaker than expected in July at 48.0 (cons 49.8) after 49.0 in June, falling to its lowest since October. Prices paid saw the largest downside surprise, falling to 64.8 (cons 70.0 from 8 responses vs 60 for the headline) from 69.7 in June for its lowest since February.

- Employment fell to 43.4 (cons 46.8 from 4 responses) from 45.0, falling below the 43.6 in Jul 2024 for its lowest since Jun 2020. Whilst manufacturing is a small share of payrolls, at about 10%, the trend direction is notable.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA down 516.39 points (-1.17%) at 43613.94

S&P E-Mini Future down 105 points (-1.65%) at 6269.5

Nasdaq down 457.4 points (-2.2%) at 20665.49

US 10-Yr yield is down 15.6 bps at 4.2179%

US Sep 10-Yr futures are up 36/32 at 112-6

EURUSD up 0.013 (1.14%) at 1.1545

USDJPY down 3.04 (-2.02%) at 147.71

WTI Crude Oil (front-month) down $1.97 (-2.84%) at $67.29

Gold is up $59 (1.79%) at $3348.92

European bourses closing levels:

EuroStoxx 50 down 154.32 points (-2.9%) at 5165.6

FTSE 100 down 64.23 points (-0.7%) at 9068.58

German DAX down 639.5 points (-2.66%) at 23425.97

French CAC 40 down 225.81 points (-2.91%) at 7546.16

US TREASURY FUTURES CLOSE

3M10Y -10.544, -7.639 (L: -8.343 / H: 6.001)

2Y10Y +10.082, 51.568 (L: 41.287 / H: 52.131)

2Y30Y +16.312, 110.394 (L: 94.082 / H: 110.599)

5Y30Y +10.929, 103.514 (L: 92.759 / H: 103.614)

Current futures levels:

Sep 2-Yr futures up 15/32 at 103-30.75 (L: 103-14.875 / H: 103-31)

Sep 5-Yr futures up 27.5/32 at 109-1 (L: 108-00 / H: 109-01.5)

Sep 10-Yr futures up 1-04/32 at 112-6 (L: 110-23.5 / H: 112-07.5)

Sep 30-Yr futures up 1-16/32 at 115-22 (L: 113-10 / H: 115-25)

Sep Ultra futures up 1-17/32 at 118-27 (L: 116-05 / H: 118-30)

MNI US 10YR FUTURE TECHS: (U5) Cracks Resistance

- RES 4: 112-23 High May 1

- RES 3: 112-15 61.8% retracement of the Apr 7 - 11 sell-off

- RES 2: 112-12+ High Jul 1 and a bull trigger

- RES 1: 112-07+ High Aug 1

- PRICE: 112-06+ @ 1435E Aug 1

- SUP 1: 110-19+/08+ Low Jul 24 / Low Jul 14 & 16

- SUP 2: 110-03 76.4% retracement of the May 22 - Jul 1 bull leg

- SUP 3: 109-28 Low Jun 6 and 11

- SUP 4: 109.25 Low May 27

Treasury futures rallied sharply on the back of the soft NFP print, resulting in a break of key short-term resistance at 111-14+, the high on Jul 22 and 30 low. A clear break of this hurdle highlights a stronger reversal and sets the scene for a climb towards 111-28, the Jul 3 high. Clearance of 111-28 would open 112-12+, the Jul 1 high and the next key resistance. On the downside, key support is 110-08+, the Jul 14 and 16 low. First support lies at 110-19+, the Jul 24 low.

SOFR FUTURES CLOSE

Sep 25 +0.170 at 95.935

Dec 25 +0.290 at 96.260

Mar 26 +0.315 at 96.495

Jun 26 +0.30 at 96.730

Red Pack (Sep 26-Jun 27) 0.180 to +0.275

Green Pack (Sep 27-Jun 28) +0.145 to +0.165

Blue Pack (Sep 28-Jun 29) +0.120 to +0.135

Gold Pack (Sep 29-Jun 30) +0.105 to +0.120

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.39% (+0.07), volume: $2.933T

- Broad General Collateral Rate (BGCR): 4.36% (+0.05), volume: $1.134T

- Tri-Party General Collateral Rate (TCR): 4.36% (+0.05), volume: $1.111T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $92B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $208B

FED Reverse Repo Operation

RRP usage falls to $97.426B (lowest levels since April 25) this afternoon from $214.445B yesterday, total number of counterparties at falls to 21 from 52. Lowest usage of the year at $54.772B on Wednesday, April 16 -- in turn the lowest level since April 2021 - compares to July 1: $460.731B highest usage since December 31.

MNI FOREX: Accelerated Fed Timeline Undermines Week's USD Rally

- A rush forward in Fed rate cut expectations for September (and through the rest of 2025) followed a soft NFP print Friday, with pricing of a 25bps cut shifting from 10bps to over 20bps very swiftly - dragging the USD with it. The resultant USD downdraft tipped the USD Index well through both the Thursday and Wednesday lows. With payrolls growth weaker than expected in July, another huge downward revision in both June and May, the building pressure on the FOMC to move on rates will build - evident in the dissenting statement issued by Bowman and Waller Friday.

- Volatile markets Friday extended the spell of JPY uncertainty, with the currency rallying sharply against all others. USD/JPY has traded a wide range this week, and the correction lower in USD/JPY tips the price back below the 200-dma. Importantly for bulls, support at 147.63, the 20-day EMA, and 147.63, the 50-day EMA, remain intact.

- Focus in the coming week shifts to the BoE rate decision, at which anything other than a 25bp cut would be a major surprise. Markets are currently pricing a 93% probability of that outcome, and guidance is also widely expected to be unchanged with the "gradual", "restrictive" and "careful" buzzwords all likely to remain.

- Into the decision, a bearish theme in GBPUSD remains intact, despite the Friday bump higher. This week’s sell-off has resulted in a breach of the bear trigger at 1.3365, the Jul 16 low. The break confirms a resumption of the downleg that started Jul 1 and highlights a clear breach of the trendline drawn from the Jan 13 low.

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 04/08/2025 | 0630/0830 | *** | CPI | |

| 04/08/2025 | 0700/0300 | * | Turkey CPI | |

| 04/08/2025 | 1400/1000 | ** | Factory New Orders | |

| 04/08/2025 | 1400/1000 | ** | Factory New Orders | |

| 04/08/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 04/08/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 05/08/2025 | 2300/0900 | * | S&P Global Final Australia Services PMI | |

| 05/08/2025 | 2300/0900 | ** | S&P Global Final Australia Composite PMI | |

| 05/08/2025 | 0030/0930 | ** | S&P Global Final Japan Services PMI | |

| 05/08/2025 | 0030/0930 | ** | S&P Global Final Japan Composite PMI | |

| 05/08/2025 | 0145/0945 | ** | S&P Global Final China Services PMI | |

| 05/08/2025 | 0145/0945 | ** | S&P Global Final China Composite PMI |