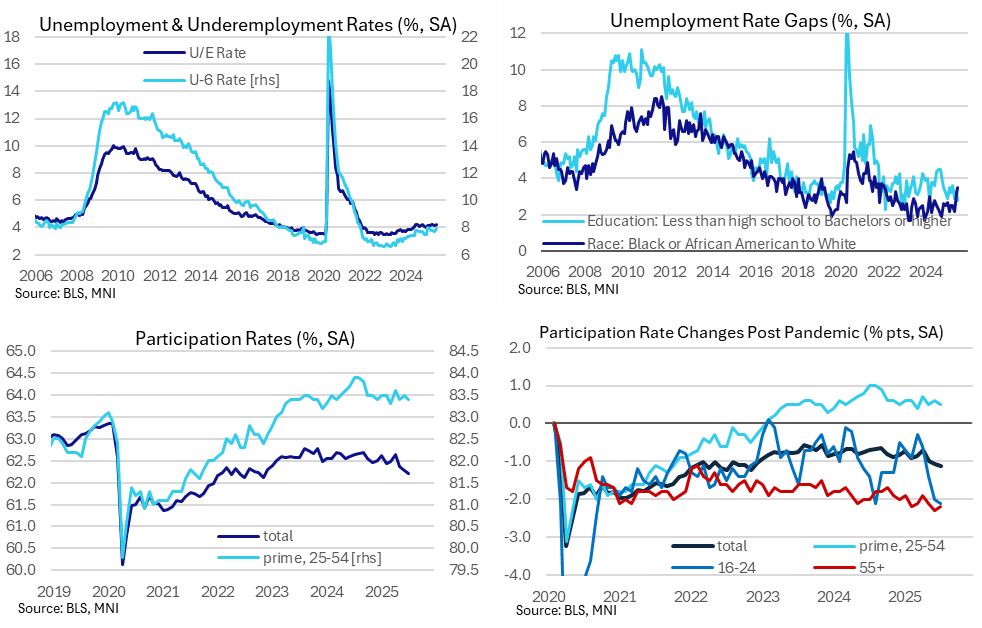

US DATA: Another Participation Rate Decline Helps Limit U/E Rate Increase

The participation rate surprisingly declined a little further in July, helping limit the unemployment rate climb on the month. The underemployment and 25-54 unemployment rates both increased on the month but remain just below cycle highs unlike the overall unemployment rate which poked above May’s latest high.

- The rise in the unemployment rate in July came along with the participation rate surprisingly falling further to 62.22% (cons 62.3%) after 62.28% in June for its lowest since late 2022.

- It marks a sizeable 0.4pp decline from 62.64% in April thanks to aforementioned heavy declines in the labor supply, albeit ones that petered out most recently in July.

- This latest decline in participation was led by the prime 25-54 falling back a tenth to 83.4% (broadly plateauing around 83.5% since Oct 2024) and 16-24 year olds ticking 0.1pp lower after -0.6pp in June to 54.8% (hitting its lowest since Sep 2020). 55+ participation meanwhile nudged 0.1pp higher to 38.1% after what had been its lowest since 2007.

- Back to unemployment rates, the 25-54 cohort saw a more pronounced bounce in July to 3.58% after 3.32% for a little above the 3.55% in May. However, unlike the overall rate at cycle highs, it’s still below recent highs seen in Nov 2024 (3.68%) and Jul 2024 (3.63%).

- Looking at broader measures of unemployment, those working part-time for economic reasons also bounced 219k after -159k in June, the strongest increase since a large 460k February. This helped the underemployment rate climb two tenths to 7.9%, although unlike the main unemployment rate, this is below the 8.0% seen in February on account of that jump in economic part-time positions.

- Different sectors are experiencing the labor market weakening at different paces, with the gap of Black/African American to White unemployment rate widening strongly again to 3.5pps for its highest since Jan 2022.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: 5s30s Capped By 140bp

5s30s unable to break decisively above 140bp at this stage, but still on track for the highest close of ’25.

- Looking a little more granularly, the next major point of upside interest beyond 140bp is probably located at the April intraday high (147.2bp according to BBG), although the lack of liquidity apparent at that time brings into question the true intraday high in the spread.

EURGBP TECHS: Bull Cycle Accelerates

- RES 4: 0.8781 2.236 pro of the Mar 3 - 11 - 28 price swing

- RES 3: 0.8738 High Apr 11 high and a key resistance

- RES 2: 0.8694 High Apr 14

- RES 1: 0.8661 Intraday high

- PRICE: 0.8655 @ 14:38 BST Jul 2

- SUP 1: 0.8521/8486 20- and 50-day EMA values

- SUP 2: 0.8459 Low Jun 11

- SUP 3: 0.8407 Low Jun 4

- SUP 4: 0.8356 Low May 29 and the bear trigger

The trend condition in EURGBP remains bullish and this week’s gains together with today’s acceleration, reinforce current conditions. Moving average studies are in a bull-mode position - highlighting a dominant uptrend. 0.8648, 76.4% of the Apr 11 - May 29 downleg, has been pierced. A continuation higher would open 0.8738, the Apr 11 high and a key resistance. Support to watch lies at 0.8521, the 20-day EMA.

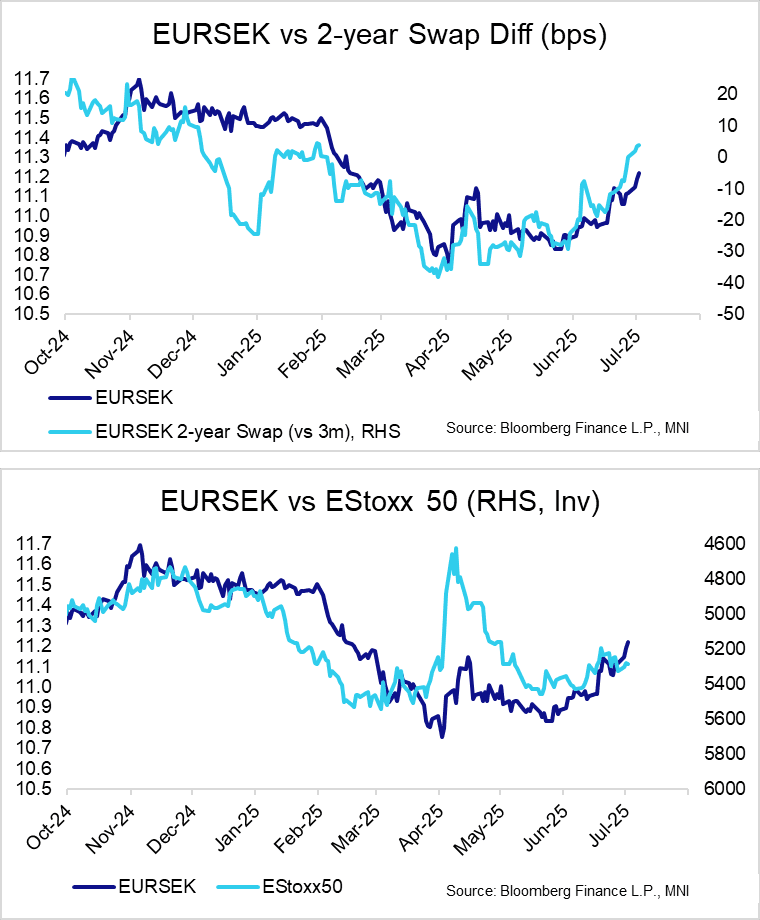

SEK: Has Underperformed G10 Over the Past Week On String Of Weak Domestic Data

The dovish June 18 Riksbank decision has been followed by a string of weak domestic data. Since June 23, the 2-year SEK swap rate has fallen 17bps, and markets now assign a ~50% implied probability of another rate cut as soon as August (up from ~25% a week ago, according to latest estimates from SEB). As such, the Swedish krona has underperformed the G10 basket over the past week.

- EURSEK is up another 0.25% today, hovering just below clustered resistance at the 200 DMA (11.2319) and April 11 high (11.2384). Beyond these levels, resistance is seen at 11.3203 (76.4% retrace of the Feb 3 to Apr 3 selloff).

- On the other hand, USDSEK remains close to multi-year lows amid the broader dollar-negative environment. The 50-day EMA at 9.6544 presents initial resistance.

- Data since the Riksbank’s June decision has included a weak Economic Tendency Survey (which had the hallmarks of the Riksbank’s June MPR “dovish” alternative scenario) and the weakest monthly retail sales print in 30 years. Meanwhile, the June manufacturing PMI eased a little to 51.9 (vs 53.1 prior). The services PMI is due tomorrow, with June flash inflation set to cross next Monday.

- We wrote earlier today that Scandinavian currencies have historically outperformed in July. From a more medium-term perspective, JP Morgan write that “SEK, and to a lesser extent NOK, have benefitted and can do so further from their large US equity holdings via either (1) increased FX hedging of USD exposure, (2) a rotation from US to RoW equities, or (3) outright sales and repatriation in equity drawdowns”.

- However, near-term risks may still be tilted towards further SEK weakness, given the Riksbank’s comfort with cutting further if justified by the data.