MNI ASIA OPEN: Consumer Sentiment Improves Ahead December FOMC

EXECUTIVE SUMMARY

- MNI US-CHINA: Bessent & Greer Hold "In Depth" Call w/Chinese Vice Premier He Lifeng

- MNI FED: Hassett Backs Bessent On Regional President Change With Feb Renewal Eyed

- MNI US DATA: Goods Pullback Weighs On Consumption But Still A Solid Q3

- MNI US DATA: Core PCE Inflation On The Soft Side, FOMC Forecast Likely To Be Lowered

- MNI US DATA: U.Mich Consumer Sentiment Improves But Conditions See Fresh Series Low

US

MNI US: Trump's NatSec Strategy Formalises Pivot To Western Hemisphere

The Trump administration released its 33-page National Security Strategy, outlining security priorities that it claims will ‘correct’ strategies that have “fallen short” since the end of the Cold War. The NSS is a document that is typically released once every presidential term, shaping policy and budgets related to national security.

- The document notes, “After the end of the Cold War, American foreign policy elites convinced themselves that permanent American domination of the entire world was in the best interests of our country. Yet the affairs of other countries are our concern only if their activities directly threaten our interests.”

- Politico notes that the NSS “has some brutal words for Europe, suggesting it is in civilizational decline, and pays relatively little attention to the Middle East and Africa. It has an unusually heavy focus on the Western Hemisphere that it casts as largely about protecting the US homeland.”

- The document explicitly states that the strategy is a “corollary” to the Monroe Doctrine, laid out in 1828 and broadly seen a formalising the Western Hemisphere with the US sphere of influence.

- Indeed, Politico notes, “the strategy spends an unusual amount of space on Latin America, the Caribbean and other U.S. neighbors. That’s a break with past administrations, who tended to prioritize other regions and other topics, such as taking on major powers like Russia and China or fighting terrorism.”

NEWS

- "*HASSETT: NOT DISCUSSED FED PRESIDENTS ISSUE WITH TRUMP

- *HASSETT: I BACK BESSENT'S VIEW ON FED RESERVE BANK PRESIDENTS

- *HASSETT: NOT DISCUSSED DERAILING APPROVAL OF PRESIDENTS IN FEB." - bbg

Bloomberg reported earlier this week that Treasury Secretary Scott Bessent will push for a new rule that candidates for regional Federal Reserve presidents must have lived in that district for at least three years. Three current Fed presidents don’t meet his criteria and he will start advocating for it going forward rather than retroactively. It should be viewed in the context of the upcoming renewal of regional Fed presidents’ five-year terms in February 2026, although Hassett appears cautious on publicly discussing any attempts to "derail" these picks at this stage.

In other Hassett headlines, he reiterates that it's time for the Fed to cautiously reduce rates. He is optimistic on growth ahead but sees it comes along with strong productivity growth in moves that will quell inflationary pressures:

- "*HASSETT: EXPECT SHUTDOWN HAD BIGGER HIT THAN EXPECTED

- "*HASSETT: THERE'LL BE BIGGER REBOUND IN FIRST QUARTER

- *HASSETT: MASSIVE MOMENTUM INTO NEXT YEAR AS FACTORIES OPEN

- *HASSETT: WOULD BE DISAPPOINTED WITH 3% GROWTH FOR Q1, Q2

- *HASSETT: COULD BE LOOKING AT A 4% PRODUCTIVITY FIGURE FOR 2026" - bbg

MNI US-CHINA: Bessent & Greer Hold "In Depth" Call w/Chinese Vice Premier He Lifeng

Reuters reporting that Chinese Vice Premier He Lifeng held a call with US Treasury Secretary Scott Bessent and United States Trade Representative Jamieson Greer. According to Reuters, He said the sides had an “in depth” and “constructive” exchange and agreed to “expand lists for cooperation.”

US TSYS

MNI US TSYS: Ylds Rise Ahead Expected 25Bp Cut from Fed, Potential Hawkish Messaging

- US treasuries look to finish moderately weaker Friday, near midday lows despite heavy buy blocks in Mar'26 5- and 10Y futures (+97k and +80k respectively).

- Currently, the TYH6 contract trades -6 at 112-17 vs. 112-15 low. Price traded through the 50-day EMA at 112-27 earlier in week. A clear breach of this average undermines a recent bull theme and signals scope for a deeper retracement, potentially towards 112-07, the Nov 5 high and a bear trigger.

- Sentiment was cautiously positive ahead of an expected 25bp rate cut from the Fed next week (potential for hawkish messaging), while the morning's mixed data spurred some position squaring.

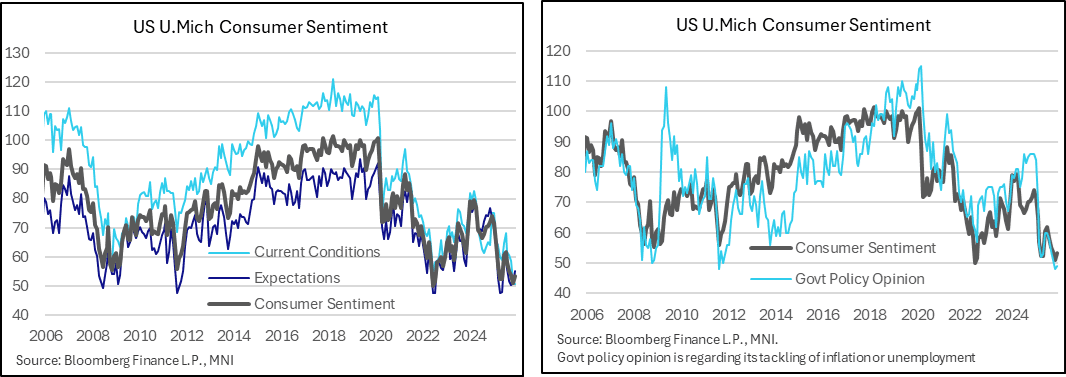

- U.Mich consumer sentiment was higher than expected in the preliminary December release, as better expectations offset disappointing current conditions. It was supported by lower inflation expectations but we continue to caution reading too much into these preliminary results.

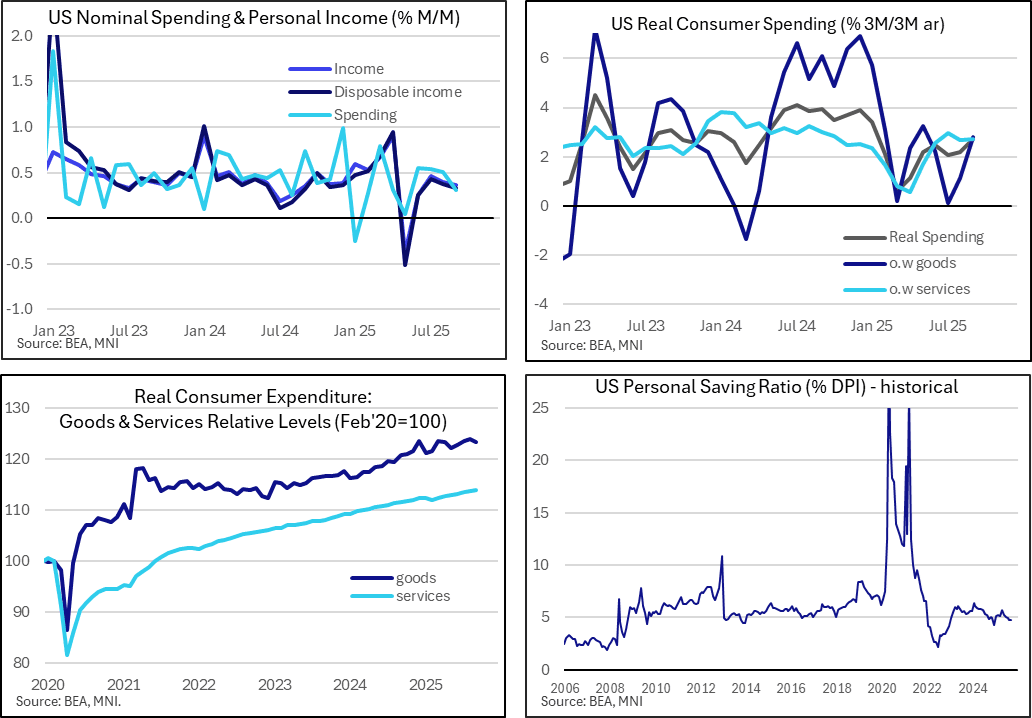

- The delayed personal income and outlays report for September saw a decline in goods spending offset more-of-the-same for services consumption. It still left real spending up a solid 2.7% in Q3 whilst the savings rate saw a second month at its lowest since December.

- Next week is dominated by the FOMC decision, widely expected to deliver a third consecutive 25bp cut after NY Fed Williams’ uncharacteristic guidance following the delayed September payrolls report. It’s likely to be a contentious meeting though with many FOMC members preferring to have paused.

- Being a SEP meeting, the dot plot distribution will be watched keenly whilst we expect the economic projections to show an upward revision for GDP growth and downward revision for core PCE inflation.

OVERNIGHT DATA

MNI US DATA: U.Mich Consumer Sentiment Improves But Conditions See Fresh Series Low

U.Mich consumer sentiment was higher than expected in the preliminary December release, as better expectations offset disappointing current conditions. It was supported by lower inflation expectations but we continue to caution reading too much into these preliminary results.

- Consumer sentiment increased to 53.3 in December (cons 52.0) from 51.0 after what had been its lowest since Jun 2022 which in turn was the lowest on record. Current conditions fell further to 50.7 (cons 52.1) from 51.1 for a fresh series low, whilst expectations increased 4pts to 55.0 (cons 52.7).

MNI US DATA: Goods Pullback Weighs On Consumption But Still A Solid Q3

The delayed personal income and outlays report for September saw a decline in goods spending offset more-of-the-same for services consumption. It still left real spending up a solid 2.7% in Q3 whilst the savings rate saw a second month at its lowest since December.

- Real personal spending was softer than expected in September even if the extent of its miss was exaggerated by rounding, both with the 0.04% M/M in Sep (cons 0.1) and the downward revision to 0.25% from an initially reported 0.35% (which rounded to 0.2 from 0.4).

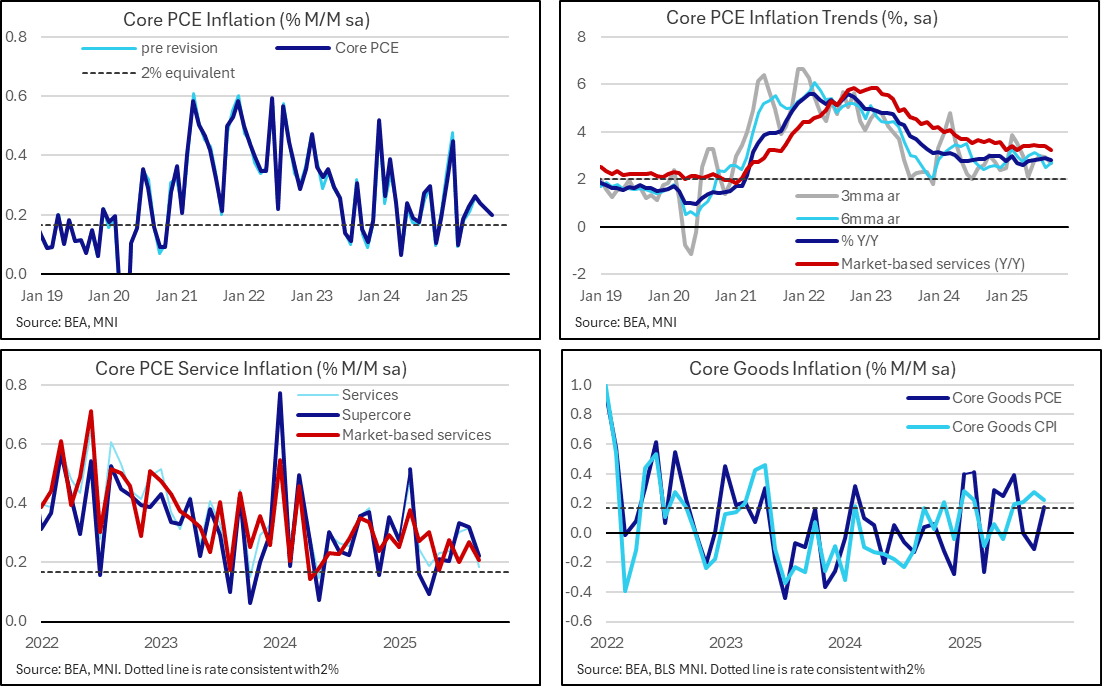

MNI US DATA: Core PCE Inflation On The Soft Side, FOMC Forecast Likely To Be Lowered

Core PCE inflation came in at 0.20% M/M in September, at the low end of the 0.20-0.23 range we’d seen for unrounded estimates that had centered on a 0.22% print. Further, some expectations of a net upward revision to the prior two months weren’t see, a marginal downward revision to Aug offsetting an equally small upward revision to Jul.

- It leaves core PCE inflation at 0.20% M/M after 0.22% in Aug and an average 0.24% through May-Jul, with the peak monthly rate for the post-tariff period being 0.26% M/M back in June.

MNI CANADA DATA: Another Jobs Report That Nixes BoC Fears Of Weakening Labour Market

The November labour survey was much stronger than expected even after allowing for some caveats that undermine the extent of the beat, such as another part-time driven jobs gain and rounding for the u/e rate,. Markets have reacted strongly, with 5Y GoC yields currently 12.5bp higher post-release for +15.5bp on the day and USDCAD falling ~50 pips.

- Employment jumped 54k (sa, cons -2.5k) in November for a third consecutive very strong month. It follows increases of 67k in Oct and 60k in Sep after a cumulative 106k decline through Jul-Aug, highlighting the survey’s volatility.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA up 113.29 points (0.24%) at 47965.76

S&P E-Mini Future up 12.75 points (0.19%) at 6879.5

Nasdaq up 61 points (0.3%) at 23565.16

US 10-Yr yield is up 3.7 bps at 4.1351%

US Mar 10-Yr futures are down 6/32 at 112-17

EURUSD down 0.0003 (-0.03%) at 1.1641

USDJPY up 0.21 (0.14%) at 155.3

WTI Crude Oil (front-month) up $0.39 (0.65%) at $60.05

Gold is down $2.5 (-0.06%) at $4205.34

European bourses closing levels:

EuroStoxx 50 up 5.85 points (0.1%) at 5723.93

FTSE 100 down 43.86 points (-0.45%) at 9667.01

German DAX up 146.11 points (0.61%) at 24028.14

French CAC 40 down 7.29 points (-0.09%) at 8114.74

US TREASURY FUTURES CLOSE

Curve update:

3M10Y +4.323, 42.982 (L: 37.238 / H: 44.082)

2Y10Y -0.073, 57.269 (L: 55.4 / H: 58.255)

2Y30Y -0.258, 122.741 (L: 121.371 / H: 124.144)

5Y30Y -0.343, 107.673 (L: 107.096 / H: 109.147)

Current futures levels:

Mar 2-Yr futures down 2.125/32 at 104-8.5 (L: 104-08 / H: 104-11.5)

Mar 5-Yr futures down 4.5/32 at 109-7.75 (L: 109-06.5 / H: 109-15)

Mar 10-Yr futures down 5.5/32 at 112-17.5 (L: 112-15 / H: 112-27.5)

Mar 30-Yr futures down 14/32 at 115-19 (L: 115-14 / H: 116-11)

Mar Ultra futures down 16/32 at 118-21 (L: 118-15 / H: 119-17)

MNI US 10YR FUTURE TECHS: (H6) Bear Threat Still Present

- RES 4: 114-00 Round number resistance

- RES 3: 113-29+ High Oct 17 and a key resistance

- RES 2: 113-23 High Oct 23

- RES 1: 113-07/22+ High Dec 3 / High Nov 25

- PRICE: 112-18 @ 17:00 GMT Dec 5

- SUP 1: 112-16+ Low Dec 05

- SUP 2: 112-10+ Low Nov 20

- SUP 3: 112-07 Low Nov 5 and a key support

- SUP 4: 112-02+ Low Sep 25

A bearish theme in Treasuries remains intact. Price has traded through the 50-day EMA, at 112-27. A clear breach of this average undermines a recent bull theme and signals scope for a deeper retracement, potentially towards 112-07, the Nov 5 high and a bear trigger. A reversal higher is required to once again refocus attention on the key resistance and bull trigger at 113-29+, the Oct 17 high.

SOFR FUTURES CLOSE

Current White pack (Dec 25-Sep 26):

Dec 25 -0.003 at 96.270

Mar 26 -0.015 at 96.435

Jun 26 -0.025 at 96.645

Sep 26 -0.035 at 96.790

Red Pack (Dec 26-Sep 27) -0.05 to -0.045

Green Pack (Dec 27-Sep 28) -0.045 to -0.045

Blue Pack (Dec 28-Sep 29) -0.04 to -0.035

Gold Pack (Dec 29-Sep 30) -0.035 to -0.025

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.92% (-0.03), volume: $3.300T

- Broad General Collateral Rate (BGCR): 3.87% (-0.03), volume: $1.320T

- Tri-Party General Collateral Rate (TCR): 3.87% (-0.03), volume: $1.298T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.89% (+0.00), volume: $87B

- Daily Overnight Bank Funding Rate: 3.89% (+0.00), volume: $173B

FED Reverse Repo Operation

RRP usage slips to $1.485B with 8 counterparties this afternoon from $2.233B Thursday. Compares to last Tuesday November 18: $0.905B - lowest level since mid-March 2021; this years highest excess liquidity measure: $460.731B on June 30.

MNI PIPELINE: Corporate Bond Update: Over $40.5B Debt Issued on Week

No new issuance Friday, likely to remain slow into next Wednesday's FOMC policy announcement. $10.25B Priced Thursday, $40.675B/wk:

- Date $MM Issuer (Priced *, Launch #)

- 12/04 $3.5B *Rep of South Africa $1.75B 12Y 6.25%, $1.75B 30Y 7.375%

- 12/04 $3B *Venture Global $1.75B 5NC 6.125%, $1.25B 8.5NC 6.5%

- 12/04 $1.5B *Telus $800M 30.5NC5.25 6.375%, $700M 30.5NC10.25 6.25%

- 12/04 $1B *OneMain Finance 7.75NC3 6.75% (double initial size)

- 12/04 $500M *Yapi Kredi WNG 10.5NC5.5 7.55%

- 12/04 $750M *MercadoLibre 7Y +130

EGBS

Futures | Change (Price) | Change (%) | |

| One-day | |||

| Bund | 128.44 | -0.18 | -0.14% |

| Gilt | 91.76 | 0.08 | 0.09% |

| OAT | 120.84 | -0.26 | -0.21% |

| BTP | 120.39 | -0.24 | -0.20% |

| AU 10Yr | 95.285 | -0.06 | -0.06% |

MNI FOREX: DXY Consolidates Weekly Decline, CAD Soars Post Employment Report

- Two-way swings left the USD index close to unchanged on Friday, but importantly the index is consolidating a solid 0.5% decline this week, as a short-term bearish bias dominates the narrative. Fed easing expectations and associated risk-on dynamics continue to weigh on the greenback.

- There has been an impressive 0.9% selloff for USDCAD on Friday following the impressive employment report for November, where the unemployment rate dipped to the 6.5%, the lowest level since July 2024.

- Tepid trade talk optimism and technical breaks have exacerbated the USDCAD declines. Both the breach of the bull channel around 1.3940, and the clean break of key 1.3888 support significantly bolster the renewed bearish theme, placing 1.3812 and 1.3727 as the next chart points of note. As a reminder, we have both the BOC and FOMC rate decisions next week, likely to keep the spotlight on USDCAD in coming sessions.

- Elsewhere, AUDUSD traded further above the late October highs of 0.6618 to reach a session peak of 0.6649, the highest level since mid-September. The pair has now posted 10 consecutive sessions of higher highs, as the bullish impulsive wave extends. With a number of resistance points being cleared, targets on the topside are now found at 0.6660 (Sep 18 high) and 0.6723, the Oct 21 2024 high.

- In emerging markets, the Brazilian real came under significant pressure on Friday as reports were confirmed that Ex-President Jair Bolsonaro will throw his support behind his son Flavio for next year’s presidential candidate. USDBRL rose over 2% on the sharp increase in potential political uncertainty ahead.

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 08/12/2025 | 0700/0800 | ** | Industrial Production | |

| 08/12/2025 | - | *** | Trade | |

| 08/12/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 08/12/2025 | 1430/1430 | BOE Taylor Panel on Growth/Wealth/Debt | ||

| 08/12/2025 | 1500/1600 | ECB Cipollone Lecture at Frankfurt School of Finance & Management | ||

| 08/12/2025 | 1600/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 08/12/2025 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 08/12/2025 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 08/12/2025 | 1800/1300 | *** | US Note 03 Year Treasury Auction Result | |

| 08/12/2025 | 1830/1830 | BOE Lombardelli Panel on Women in Economics | ||

| 08/12/2025 | - | FOMC Meetings with S.E.P. | ||

| 09/12/2025 | 0001/0001 | * | BRC-KPMG Shop Sales Monitor | |

| 09/12/2025 | 0330/1430 | *** | RBA Rate Decision |