US DATA: Goods Pullback Weighs On Consumption But Still A Solid Q3

Dec-05 15:42

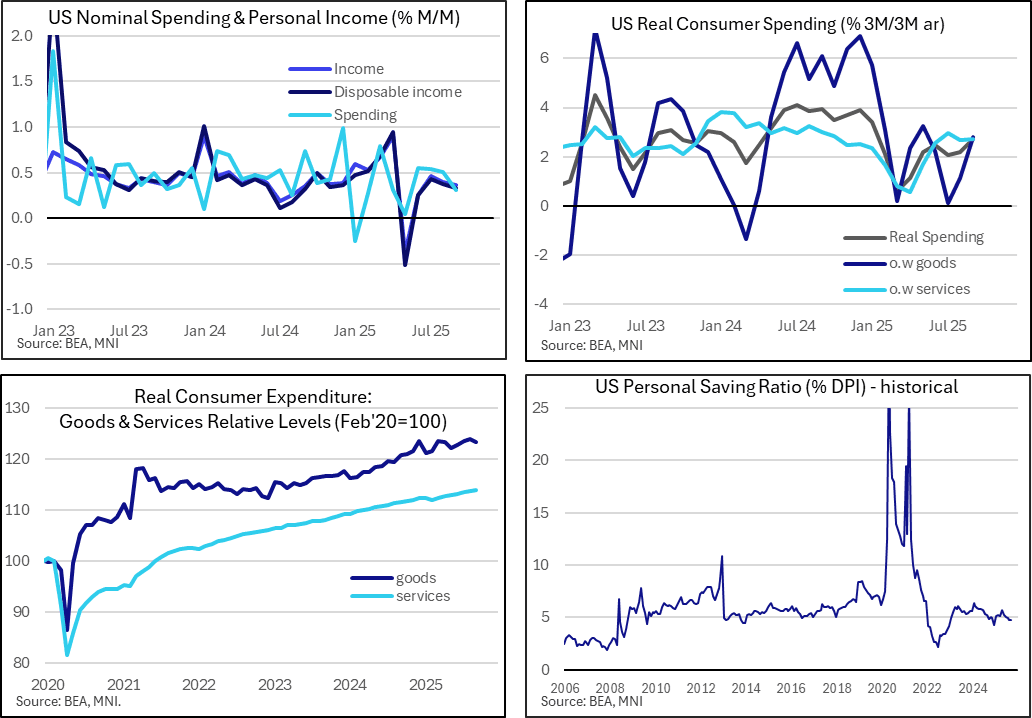

The delayed personal income and outlays report for September saw a decline in goods spending offset more-of-the-same for services consumption. It still left real spending up a solid 2.7% in Q3 whilst the savings rate saw a second month at its lowest since December.

- Real personal spending was softer than expected in September even if the extent of its miss was exaggerated by rounding, both with the 0.04% M/M in Sep (cons 0.1) and the downward revision to 0.25% from an initially reported 0.35% (which rounded to 0.2 from 0.4).

- We estimated that retail sale volumes slipped a heavy -0.4% M/M in last week’s September report and indeed, real goods spending fell -0.4% M/M in today’s’ release after a notably downward revised 0.3% (initial 0.7).

- Real services consumption maintained recent trends meanwhile, at 0.25% M/M after an average 0.22% M/M through Jun-Aug.

- Looking more broadly, the quarterly profile of overall consumption saw another solid quarter with 2.7% annualized in Q3 after 2.5% in Q2 having recovered from the 0.6% in Q1. It averaged 3.4% annualized in 2024.

- Y/Y consumption growth is a little weaker however, easing from 2.6% to 2.1% Y/Y for its softest since Jan 2024.

- Reverting to the nominal details, personal income increased 0.4% M/M as expected, with disposable income a little softer at 0.3% M/M. Combined with personal spending of 0.3% M/M and the household savings ratio held steady at 4.7%, consolidating a drop to its lowest since Dec 2024 after underwhelming income dynamics in August.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OPTIONS: Expiries for Nov6 NY cut 1000ET (Source DTCC)

Nov-05 15:41

- EUR/USD: $1.1400(E1.5bln), $1.1450(E560mln), $1.1500(E1.6bln), $1.1525(E604mln), $1.1550(E1.8bln), $1.1600(E1.6bln), $1.1715(E1.5bln)

- GBP/USD: $1.2900(Gbp2.0bln), $1.3100(Gbp1.0bln), $1.3350(Gbp770mln)

- USD/JPY: Y152.00($1.0bln), Y153.00-05($1.2bln), Y154.00-05($1.1bln), Y154.50-55($1.1bln), Y155.00($1.9bln), Y155.35($1.2bln)

- EUR/GBP: Gbp0.8800-10(E1.1bln)EUR/JPY: Y177.00-05(E561mln)

- AUD/USD: $0.6480-90(A$650mln)

GILTS: First Support Holds In Futures

Nov-05 15:34

Gilts still closely tracking U.S. Tsys after the firmer-than-expected ISM services survey and prices paid sub-component extended the sell off in the former.

- Still, Tsys have now stabilised allowing gilt futures to base around previously identified initial support (lows of 93.14 vs. support at 93.15).

- Yields 2-4.5bp higher, curve holds steeper.

- 10-Year yields still haven’t managed to close the gap that came after the softer-than-expected CPI data in late October (4.478%).

MNI: US EIA: CRUDE OIL STOCKS EX SPR +5.2M TO 421.2M OCT 31 WK

Nov-05 15:30

- US EIA: CRUDE OIL STOCKS EX SPR +5.2M TO 421.2M OCT 31 WK

- US EIA: DISTILLATE STOCKS -0.64M TO 111.5M IN OCT 31 WK

- US EIA: GASOLINE STOCKS -4.73M TO 206.0M IN OCT 31 WK

- US EIA: CUSHING STOCKS +0.3M TO 22.9M BARRELS IN OCT 31 WK

- US EIA: SPR +0.5M TO 409.6M BARRELS IN OCT 31 WK

- US EIA: REFINERY UTILIZATION WEEK CHANGE -0.6% TO 86.0% IN OCT 31 WK