US DATA: Core PCE Inflation On The Soft Side, FOMC Forecast Likely To Be Lowered

Dec-05 15:20

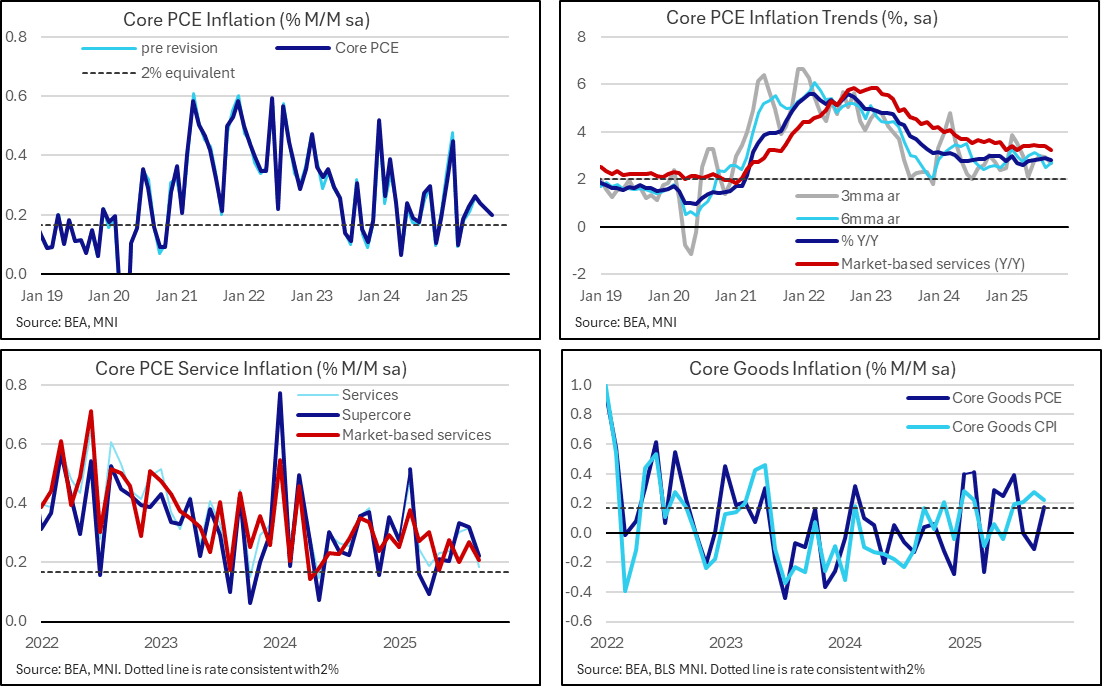

- Core PCE inflation came in at 0.20% M/M in September, at the low end of the 0.20-0.23 range we’d seen for unrounded estimates that had centered on a 0.22% print.

- Further, some expectations of a net upward revision to the prior two months weren’t see, a marginal downward revision to Aug offsetting an equally small upward revision to Jul.

- It leaves core PCE inflation at 0.20% M/M after 0.22% in Aug and an average 0.24% through May-Jul, with the peak monthly rate for the post-tariff period being 0.26% M/M back in June.

- Monthly drivers came from core goods inflation firming to 0.18% M/M after -0.11% M/M whilst non-housing core services appears to have been behind the small miss as it was relatively subdued at 0.22% M/M (Nomura had estimated 0.26, MS 0.28) after two months averaging 0.33% M/M.

- Looking at broader trends, core PCE inflation eased to 2.83% Y/Y after the 2.90% in August was its highest since February, and more recent run rates eye some further moderation with both the three- and six-month averages at 2.7% annualized.

- With services an area of increased concern recently in previous signs of tariff spillover, we note that market-based services inflation eased to 3.2% Y/Y after five consecutive months at 3.4%. Highlighting its still elevated nature though, this series averaged 2.2% in 2017-19.

- Core inflation therefore is still stubbornly above the 2% inflation target but it still looks increasingly likely we'll see downward revisions to the FOMC median core PCE forecast of 3.1% Y/Y in 4Q25 with next week’s SEP.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY FUTURES: BLOCKs: Large Dec'25 10Y Buys

Nov-05 15:18

- +10,000 TYZ5 112-15 - post time bid at 1005:10ET - still said to be a buy, DV01 $661,000

- +8,000 TYZ5 112-14, post time offer at 1009:23ET, DV01 $529,000.

- The 10Y contract trades 112-15 last (-10)

RIKSBANK: MNI Riksbank Review: November 2025 - No New Signals

Nov-05 15:13

FOR THE FULL PUBLICATION PLEASE CLICK HERE

EXECUTIVE SUMMARY:

- The Riksbank’s November decision brought few surprises. The policy rate was held at 1.75% in a unanimous decision, and the guidance language was unchanged: “The policy rate is expected to remain at this level for some time to come."

- In the press conference, Governor Thedéen was careful not to give any policy hints away. He suggested that the risks to the policy rate are balanced, in line with the horizontal rate path through Q3 2026 presented in September.

- There was no material market reaction in SEK FX and rates markets.

- We continue to think that the bar to a rate move over the next 6-12 months is fairly high, but caution that the risk of a hike back to 2.00% appears greater than the risk of another cut to 1.50%.

- Analysts are in favour of the policy rate remaining at 1.75% through the course of next year, with a handful expecting one or two rate hikes in 2027.

US TSYS: Post-ISM Services Data React

Nov-05 15:04

- Treasuries holding near lows after ISM Services data comes out higher than expected.

- Currently, the Dec'25 10Y contract trades -11.5 at 112-13.5 vs. 112-12.5 low, 10Y yield 4.1415% (+.0564), curves steeper - stable (2s10s +1.302 at 52.031; 5s30s +0.604 at 97.313).

- USD rallies in response to the solid prices paid data, helping EURUSD pressure earlier lows. A break below 1.1469 puts EURUSD again at the lowest level since August 1st. The response for USDJPY is again narrowing the gap with key resistance into 154.48, the weekly and reversal high.