CANADA DATA: Another Jobs Report That Nixes BoC Fears Of Weakening Labour Market

Dec-05 14:00

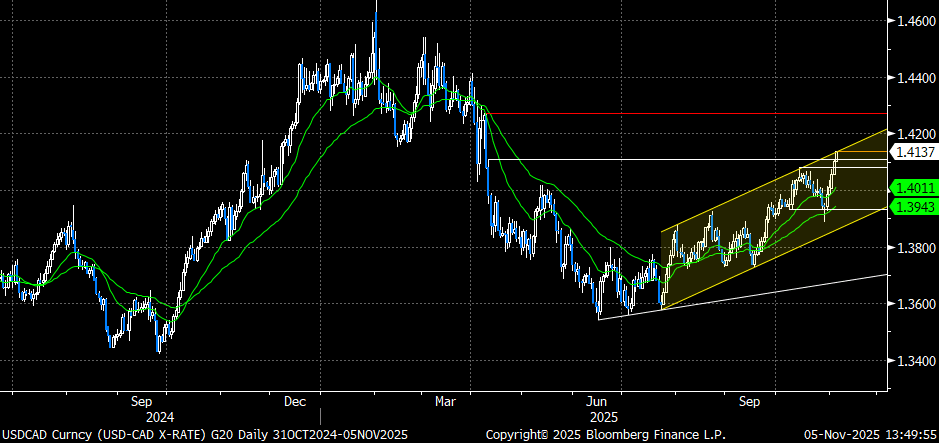

The November labour survey was much stronger than expected even after allowing for some caveats that undermine the extent of the beat, such as another part-time driven jobs gain and rounding for the u/e rate,. Markets have reacted strongly, with 5Y GoC yields currently 12.5bp higher post-release for +15.5bp on the day and USDCAD falling ~50 pips.

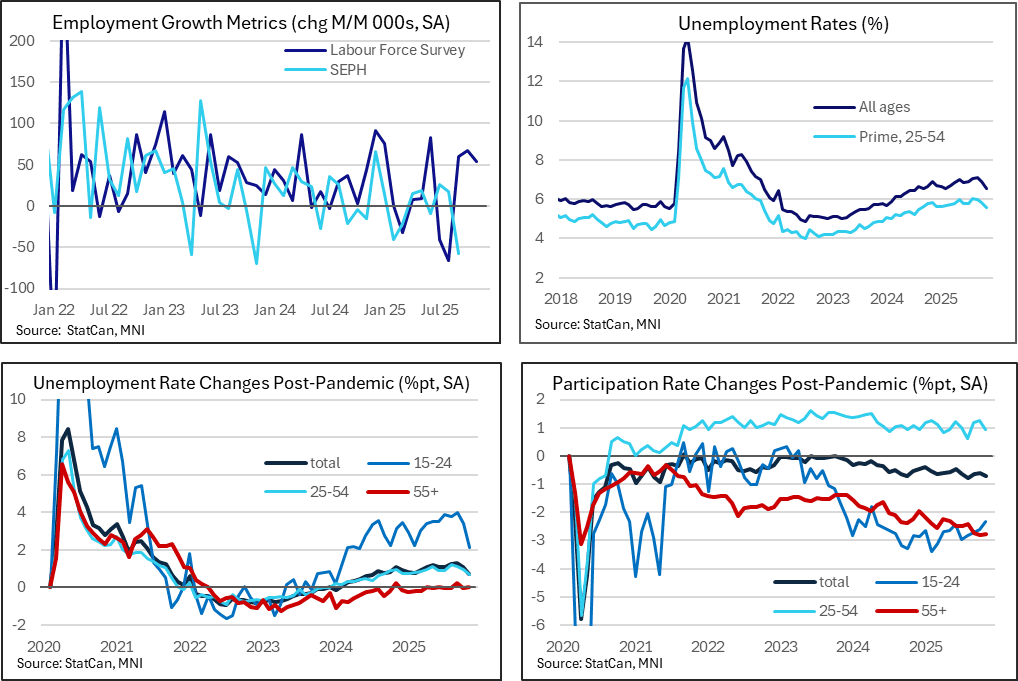

- Employment jumped 54k (sa, cons -2.5k) in November for a third consecutive very strong month. It follows increases of 67k in Oct and 60k in Sep after a cumulative 106k decline through Jul-Aug, highlighting the survey’s volatility.

- It was dominated by part-time job creation for a second month running, rising 63k after 85k in contrast to full-time jobs dropping by -9k after -19k.

- Highlighting these differences, overall employment growth stands at 1.5% Y/Y in November with full-time roles up 0.8% Y/Y (softest since Aug 2024) and part-time roles up 4.6% Y/Y (strongest since Aug 2024).

- The unemployment rate meanwhile fell from 6.88% to 6.54%, a large beat from consensus of 7.0% (albeit skewed slightly lower). This was the largest decline in the u/e rate in twenty years excluding pandemic distortions and it also sees the u/e rate return to levels from early in the year, having seen 6.55% in February.

- The decline was boosted by a large drop in the youth unemployment rate (from 14.1% to 12.8%, lowest since May 2024).

- However, the prime-age 25-54 u/e rate also still fell from 5.83% to 5.56% for its lowest since Aug 2024. It was a third consecutive decline having peaked at 6.06% in August at what was its highest since mid-2021.

- The latest two months of data since the last BoC decision on Oct 29 have seen a marked change in the assessment of the labour market, with the worry that weakness could persist and broaden not materializing. From the meeting deliberations: “Members agreed that the labour market was soft. Employment gains in September followed two months of large numbers of job losses, and the unemployment rate had risen to 7.1% from 6.6% in January and February. Members noted that employment growth was weak across the economy, but the decline in population growth meant that fewer new jobs were needed to keep the employment rate steady. Job losses since January have been concentrated in trade-related sectors, and firms in other sectors seemed to be retaining their workforces for now. Nevertheless, members expressed concern that weakness in the labour market could persist and broaden. Responses to the Business Outlook Survey showed that most businesses do not expect to increase staffing levels. And discussions with companies during regional outreach visits indicated that if demand from the United States were to weaken further, that could lead to more job losses.”

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: Bear Steepening Alongside Tsys

Nov-05 13:57

Gilts take cues from Tsys, which have softened in the wake of the ADP employment report and guidance from the U.S. Treasury re: future coupon issuance increases.

- Gilt futures trade to lowest levels of the day, breaking Monday’s lows.

- Still, bears don’t challenge initial support at the October 27 low (93.15). The bullish technical theme remains intact.

- Yields now 0.5-3.0bp higher, curve steeper.

- Medium-term uptrend support (drawn off the August ’23 low) remains intact in the 2s10s curve.

- A reminder that we flagged risks of steepening around a dovish outcome at tomorrow’s BoE decision.

FOREX: Dollar Maintains Supportive Tone Following Data/Refunding

Nov-05 13:52

- In the aftermath of both the ADP data and the US refunding announcement, pressure on treasuries has provided a supportive tone to the greenback, helping the USD index consolidate gains near recovery highs.

- The higher yields have most notably assisted USDJPY to the best levels of the session, now extending its bounce from the overnight lows to over 100 pips, trading just shy of 154.00. We highlighted yesterday that the pair stalled for a third time around the 154.45 level overnight - a potentially bearish short-term signal against the underlying bullish trend that has been in place in recent weeks.

- This area will remain in focus heading into the ISM services release later today. Above here, attention would be on 154.80, the Feb 12 high.

- Associated moderate pressure on the likes of EURUSD and GBPUSD, although both pairs remain off recent cycle lows, while USDCAD continues to pressure the top of the bullish channel drawn from the Jul 23 low and shown below:

EURIBOR OPTIONS: Large outright Call buyer

Nov-05 13:51

ERU6 98.50c, bought for 3.25 in 13.5k.