- Treasuries look to finish Friday's shortened post-Thanksgiving holiday session weaker across the board, volumes stepped up by the early close (TYH6 1.1M) despite the CME Group tech issue closure overnight.

- CME overnight: "Due to a cooling issue at CyrusOne data centers, our markets are currently halted. Support is working to resolve the issue in the near term and will advise clients of Pre-Open details as soon as they are available." CME markets were closed for over 9 hours overnight/into Friday's session.

- No obvious headline or flow driven trigger as Treasuries extend lows midmorning, TYH6 taps 113-09 low (-9.5) vs. 113-11 close, initial support below at 112-30, the 20-day EMA. Support at the 50-day EMA, lies at 112-25.

- Otherwise, a bullish theme in Treasuries remains intact and Tuesday’s gains reinforce current conditions. The recent breach of the 112-31 level, an area of congestion since Nov 5, marks an important short-term bullish development. This exposes 113-29+, the Oct 17 high and a key resistance

- Trading desks reported pre-emptive rate locks ahead corporate issuance next week as well as nascent month end selling ahead of today's early close at 1315ET.

- Reminder - the Fed enters policy blackout after midnight tonight through December 11, the day after the final FOMC of 2025. Monday look ahead: S&P Global Mfg PMI, ISM Mfg data.

MNI ASIA OPEN: CME Tech Glitch Hampered Shortened Session

Nov-30 20:06By: Bill Sokolis

US Treasuries+ 6

EXECUTIVE SUMMARY

- MNI US: MNI POLITICAL RISK - Trump Calls For Immigration Crackdown

- MNI INDIA: US-India Trade Deal Expected By Year End - Indian Trade Secretary

- MNI US Week Ahead: Last Pre-FOMC Labor Data, ISM Surveys & Delayed PCE

- MNI CANADA DATA: Surprise Q3 GDP Jump On Weak Imports, But Upward Revisions As Well

US

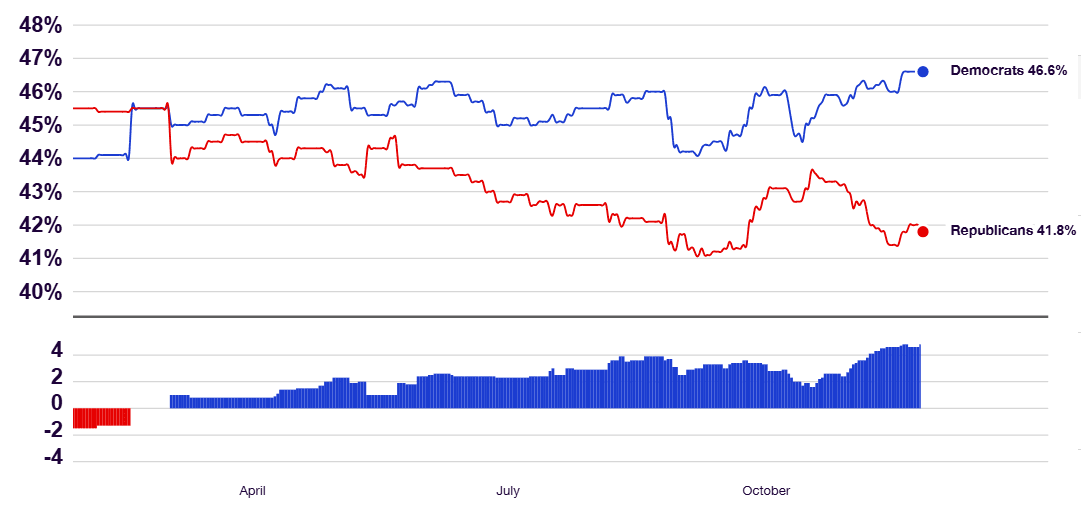

MNI US: Democrats Extend Advantage On 2026 Generic Congressional Ballot

Democrats have extended their advantage on the 2026 generic Congressional ballot to nearly five percentage points, following a tepid month of polling for President Donald Trump and an underwhelming Republican performance at off-year elections on November 5. Note: The generic ballot asks survey respondents which party’s candidate they would vote for if the 2026 midterm elections were held that day.

- The New York Times writes, “The party out of power typically gains ground in midterm elections, and these early surveys suggest this may be taking shape ahead of 2026. Democrats lead in the vast majority of recent polls, though by single-digit margins. However, with redistricting efforts underway in several states, the national vote share that Democrats need to retake the House will depend on the extent of these changes.”

- Going into the weekend, President Trump's approval shows signs of bottoming out after plunging for much of November. According to Silver Bulletin, his approval rating is back to around -14% after hitting -15% earlier in the week. But, Silver Bulletin notes, "Americans who strongly approve of Trump is still decreasing: it hit a second term low of 24.0 percent yesterday," suggesting that Trump may be losing some support amongst his core MAGA base.

Figure 1: 2026 Generic Congressional Vote Source: RealClearPolitics

NEWS

MNI US: MNI POLITICAL RISK - Trump Calls For Immigration Crackdown

President Donald Trump remains at his Mar-a-Lago resort in Florida. There are no public events in his diary for today or the weekend. He is scheduled to return to the White House on Sunday evening. Trump called for an immigration crackdown, including ‘reverse migration’, in a series of posts on Truth Social, following a fatal attack on National Guard troops near the White House.

MNI SECURITY: Yermak Resignation Sows Uncertainty Over Peace Process

The resignation of Ukrainian President Volodymyr Zelenskyy's Chief of Staff, Andriy Yermak, has increased uncertainty over the peace process, leaving Kyiv without its chief negotiator ahead of a critical meeting in Moscow next week.

MNI INDIA: US-India Trade Deal Expected By Year End - Indian Trade Secretary

Reuters reports Indian Trade Secretary Piyush Goyal stating, “India expects to have a deal with the US before year-end as most issues already resolved.” Goyal adds negotiators are holding “virtual talks”, noting remaining issues could be addressed at the political level. Commerce Secretary Rajesh Agrawal said Monday negotiators are close to finalising a package covering US market access to India, and reducing 25% reciprocal/25% additional oil tariffs, per the Times of India.

US TSYS

MNI US TSYS: Thanks Given for Early Market Close

OVERNIGHT DATA

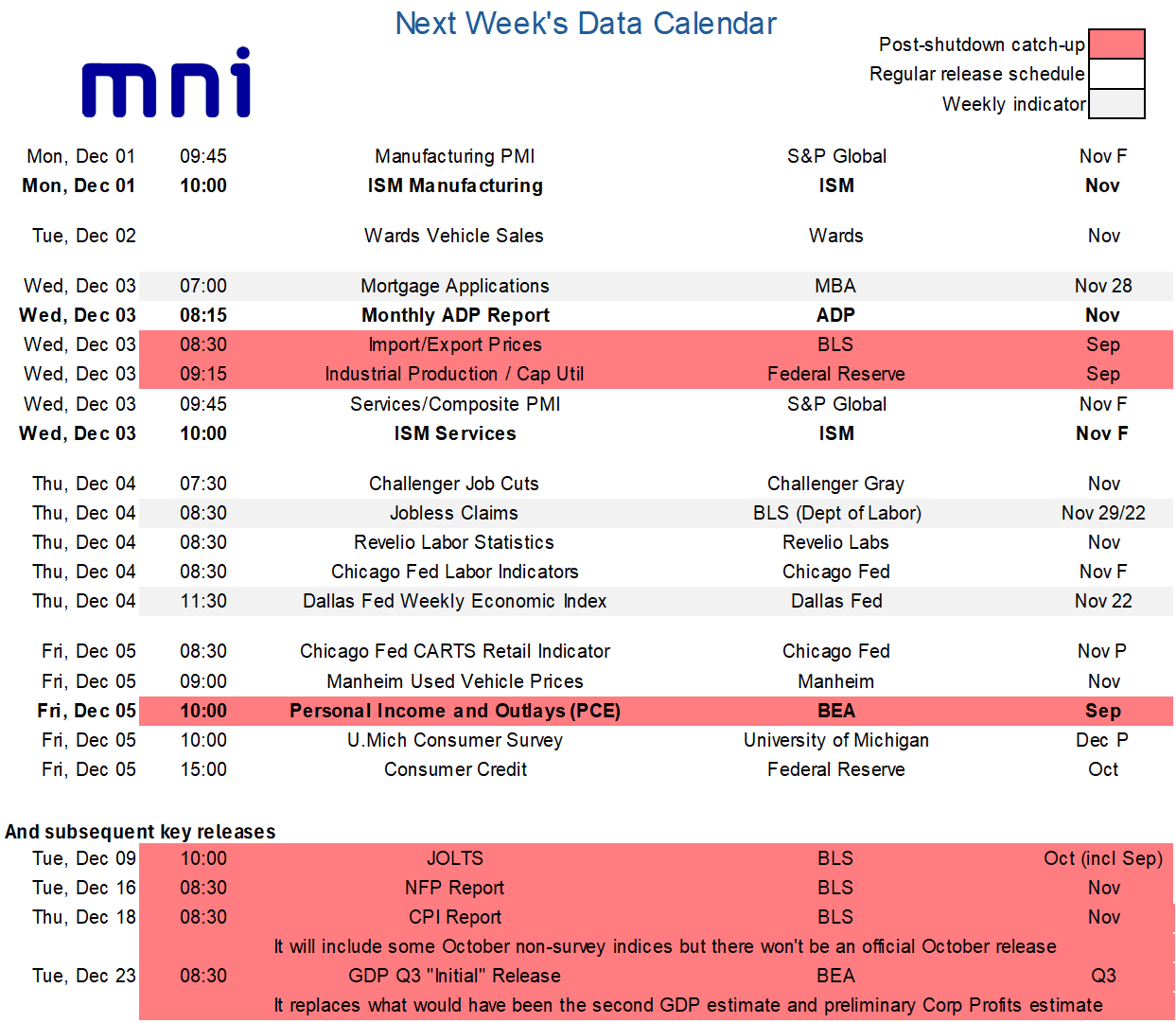

MNI US Week Ahead: Last Pre-FOMC Labor Data, ISM Surveys & Delayed PCE

Next week would ordinarily have been geared towards a nonfarm payrolls report on Friday but that of course has been rescheduled for Dec 16 as the BLS continues to work its way through the shutdown-induced data backlog. Instead, expect the myriad of labor releases starting Wednesday along with ISM surveys and monthly PCE data to help finalize market expectations ahead of the Dec 9-10 FOMC meeting - we currently anticipate a hawkish cut.

- Within the labor releases, the monthly ADP employment report for November will continue to be important – with declines in recent weekly updates - but we also flag Thursday's releases for Challenger job cuts and Revelio Labs' labor statistics for November. The October Challenger report showed a sharp increase in layoffs to its highest for an October since 2003 along with tepid hiring plans over Sep-Oct combined, whilst the Revelio nonfarm payrolls estimate drew a dovish market reaction last month when it pointed to nonfarm payrolls growth of -9k in October.

- As for ISM surveys, consensus looks for little improvement in Monday’s manufacturing survey, with regional Fed surveys on balance slightly stronger on the month versus a sharp deterioration in the MNI Chicago PMI. The still early days for the services analyst survey sees a modest dip to 52.0 having oscillated between 52.0-52.5 in the previous four months. The service PMI – at 55.0 in the November flash – has been more optimistic in each of the prior six months but with varied beats each time.

- The delayed personal income and outlays report for September then rounds out the week on Friday. This week’s retail sales release will have dampened goods-related expectations for consumer spending. We’ll also watch income dynamics after they underwhelmed in the August report released two months ago, seeing the savings rate dropping to an eight-month low. Core PCE inflation estimates appears to be tracking around 0.22% M/M for September, similar to the 0.23% M/M in August and the 0.24% averaged through May-July although with some seeing scope for minor upward revisions to Aug and Jul.

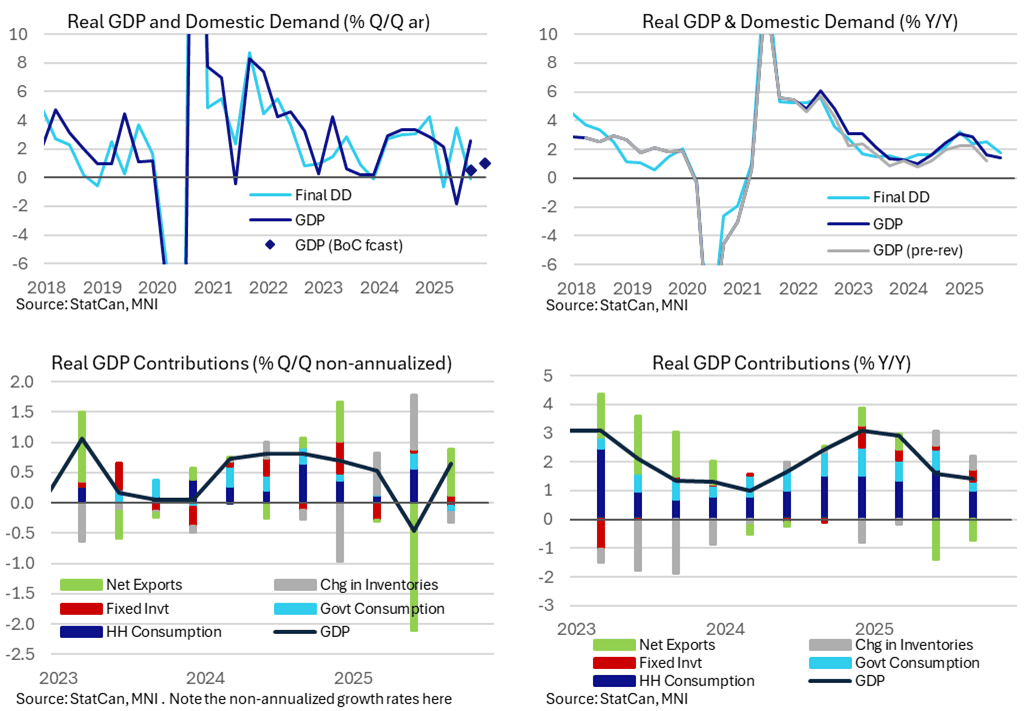

MNI CANADA DATA: Surprise Q3 GDP Jump On Weak Imports, But Upward Revisions As Well

Real GDP growth was much stronger than expected in Q3 as imports fell heavily in continued heightened volatility within trade data. Final domestic demand meanwhile was flat on the quarter after a strong Q2. For a better idea of recent trends, real GDP growth eased two tenths to 1.4% Y/Y after some solid upward revisions whilst domestic demand is a little stronger at 1.7% Y/Y. The BoC last month forecast real GDP growth of 0.5% Y/Y in 4Q25 before 1.6% in both 4Q26 and 4Q27, whilst it estimates potential output growth of 1.6% in 2025, 1.0% in 2026 and 1.3% in 2027.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA up 289.3 points (0.61%) at 47716.42

S&P E-Mini Future up 31.5 points (0.46%) at 6859.5

Nasdaq up 151 points (0.7%) at 23365.69

US 10-Yr yield is up 2.1 bps at 4.0152%

US Mar 10-Yr futures are down 7.5/32 at 113-11

EURUSD up 0.0005 (0.04%) at 1.1601

USDJPY down 0.16 (-0.1%) at 156.15

WTI Crude Oil (front-month) up $0.83 (1.42%) at $59.50

Gold is up $59.02 (1.42%) at $4216.28

European bourses closing levels:

EuroStoxx 50 up 15 points (0.27%) at 5668.17

FTSE 100 up 26.58 points (0.27%) at 9720.51

German DAX up 68.83 points (0.29%) at 23836.79

French CAC 40 up 23.24 points (0.29%) at 8122.71

US TREASURY FUTURES CLOSE

Curve update:

3M10Y +6.875, 21.444 (L: 12.969 / H: 23.179)

2Y10Y +0.267, 51.768 (L: 47.031 / H: 53.163)

2Y30Y +0.303, 116.535 (L: 114.098 / H: 118.536)

5Y30Y -0.791, 106.295 (L: 105.509 / H: 109.384)

Current futures levels:

Mar 2-Yr futures down 1.125/32 at 104-13.75 (L: 104-13.12 / H:104-15.37)

Mar 5-Yr futures down 3.75/32 at 109-24.5 (L: 109-22.25 / H: 109-28.75)

Mar 10-Yr futures down 7.5/32 at 113-11 (L: 113-09 / H: 113-19.5)

Mar 30-Yr futures down 13/32 at 117-14 (L: 117-05 / H: 117-30)

Mar Ultra futures down 18/32 at 120-30 (L: 120-21 / H: 121-20)

MNI US 10YR FUTURE TECHS: (H6) Bull Cycle Exposes Key Resistance

- RES 4: 114-00 Round number resistance

- RES 3: 113-29+ High Oct 17 and a key resistance

- RES 2: 113-23 High Oct 23

- RES 1: 113-22+ High Nov 25

- PRICE: 113-17 @ 11:17 GMT Nov 26

- SUP 1: 113-08/112-30 Low Nov 25 / 20-day EMA

- SUP 2: 112-25 50-day EMA

- SUP 3: 112-10+ Low Nov 20

- SUP 4: 112-07 Low Nov 5 and a key support

A bullish theme in Treasuries remains intact and Tuesday’s gains reinforce current conditions. The recent breach of the 112-31 level, an area of congestion since Nov 5, marks an important short-term bullish development. This exposes 113-29+, the Oct 17 high and a key resistance. On the downside, initial support is at 112-30, the 20-day EMA. Support at the 50-day EMA, lies at 112-25.

SOFR FUTURES CLOSE

Current White pack (Dec 25-Sep 26):

Dec 25 +0.008 at 96.268

Mar 26 -0.005 at 96.450

Jun 26 -0.015 at 96.695

Sep 26 -0.020 at 96.870

Red Pack (Dec 26-Sep 27) -0.03 to -0.025

Green Pack (Dec 27-Sep 28) -0.03 to -0.025

Blue Pack (Dec 28-Sep 29) -0.035 to -0.035

Gold Pack (Dec 29-Sep 30) -0.045 to -0.04

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.05% (+0.04), volume: $3.297T

- Broad General Collateral Rate (BGCR): 4.02% (+0.05), volume: $1.288T

- Tri-Party General Collateral Rate (TCR): 4.02% (+0.05), volume: $1.258T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.88% (+0.00), volume: $89B

- Daily Overnight Bank Funding Rate: 3.88% (+0.00), volume: $171B

MNI FOREX: USD Index Prints Pullback Lows into Month-End, CAD Outperforming

- Despite a constructive start for the USD index on Friday, the week’s theme of a softer dollar took over across the US session. There was a notable extension of greenback weakness into the month-end WMR fix, prompting fresh pullback lows for the DXY. Sentiment this week has been bolstered by December easing expectations for the Fed, alongside speculation over a Hassett led FOMC next year prompting a dovish repricing further out the curve.

- Price adjustments across the G10 have been mixed Friday, perhaps owing to the lower volumes following the US thanksgiving holiday and an associated lack of conviction ahead of the weekend. However, outperformance for the Canadian dollar has certainly stood out.

- Canada's economy rebounded much faster than expected in the third quarter led by a drop in imports. USDCAD plumbed fresh lows for November on the headline data beat, and then extended below support at the 50-day EMA which intersected at 1.3995. The move south reached as low as 1.3939 into the WMR fix, exposing the base of a bull channel at 1.3923, drawn from the Jul 23 low.

- A solid rebound for NZDUSD also saw the pair reach recovery highs at 0.5744, extending the impressive bounce following the hawkish cut from the RBNZ this week. NZDUSD is threatening a close above its 50-day EMA, signalling scope for a stronger recovery to the medium-term pivot of 0.5800.

- GBPUSD has consolidated its post-budget squeeze, trading within a 1.3200-55 range Friday. While there have been some tepid reversal signs this week, plenty of fiscal concerns and likely BOE easing in December remain notable GBP headwinds, underpinning the dominant bearish theme.

- Perhaps to be expected USDJPY has traded in a much more contained manner this week, remaining within a 1% range. Spot is currently down just 25 pips from last Friday’s close, as firmer risk sentiment has been offset by the weaker greenback. Overall, the trend set-up in USDJPY remains bullish. The pair has recently entered overbought territory and a deeper retracement, if seen, would allow this condition to unwind. All focus turns to BOJ Governor Ueda’s speech to business leaders in Nagoya City on Monday.

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 01/12/2025 | 0730/0830 | ** | Retail Sales | |

| 01/12/2025 | 0815/0915 | ** | S&P Global Manufacturing PMI (f) | |

| 01/12/2025 | 0845/0945 | ** | S&P Global Manufacturing PMI (f) | |

| 01/12/2025 | 0850/0950 | ** | S&P Global Manufacturing PMI (f) | |

| 01/12/2025 | 0855/0955 | ** | S&P Global Manufacturing PMI (f) | |

| 01/12/2025 | 0900/1000 | ** | S&P Global Manufacturing PMI (f) | |

| 01/12/2025 | 0930/0930 | ** | BOE Lending to Individuals | |

| 01/12/2025 | 0930/0930 | ** | BOE M4 | |

| 01/12/2025 | 0930/0930 | ** | S&P Global Manufacturing PMI (Final) | |

| 01/12/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 01/12/2025 | 1445/0945 | *** | S&P Global Manufacturing Index (final) | |

| 01/12/2025 | 1500/1000 | *** | ISM Manufacturing Index | |

| 01/12/2025 | 1530/1530 | DMO to hold FQ4 consultations with investors / GEMMs | ||

| 01/12/2025 | 1530/1530 | BOE Dhingra Keynote at UK Trade Policy Observatory | ||

| 01/12/2025 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 01/12/2025 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 02/12/2025 | 0001/0001 | * | BRC Monthly Shop Price Index | |

| 02/12/2025 | 0030/1130 | * | Building Approvals | |

| 02/12/2025 | 0030/1130 | Balance of Payments: Current Account |

Related stories

Related by topic

US Treasuries

Federal Reserve

US

FI

India

Canada

Geo-Political