FOREX: USD Index Prints Pullback Lows into Month-End, CAD Outperforming

- Despite a constructive start for the USD index on Friday, the week’s theme of a softer dollar took over across the US session. There was a notable extension of greenback weakness into the month-end WMR fix, prompting fresh pullback lows for the DXY. Sentiment this week has been bolstered by December easing expectations for the Fed, alongside speculation over a Hassett led FOMC next year prompting a dovish repricing further out the curve.

- Price adjustments across the G10 have been mixed Friday, perhaps owing to the lower volumes following the US thanksgiving holiday and an associated lack of conviction ahead of the weekend. However, outperformance for the Canadian dollar has certainly stood out.

- Canada's economy rebounded much faster than expected in the third quarter led by a drop in imports. USDCAD plumbed fresh lows for November on the headline data beat, and then extended below support at the 50-day EMA which intersected at 1.3995. The move south reached as low as 1.3939 into the WMR fix, exposing the base of a bull channel at 1.3923, drawn from the Jul 23 low.

- A solid rebound for NZDUSD also saw the pair reach recovery highs at 0.5744, extending the impressive bounce following the hawkish cut from the RBNZ this week. NZDUSD is threatening a close above its 50-day EMA, signalling scope for a stronger recovery to the medium-term pivot of 0.5800.

- GBPUSD has consolidated its post-budget squeeze, trading within a 1.3200-55 range Friday. While there have been some tepid reversal signs this week, plenty of fiscal concerns and likely BOE easing in December remain notable GBP headwinds, underpinning the dominant bearish theme.

- Perhaps to be expected USDJPY has traded in a much more contained manner this week, remaining within a 1% range. Spot is currently down just 25 pips from last Friday’s close, as firmer risk sentiment has been offset by the weaker greenback. Overall, the trend set-up in USDJPY remains bullish. The pair has recently entered overbought territory and a deeper retracement, if seen, would allow this condition to unwind. All focus turns to BOJ Governor Ueda’s speech to business leaders in Nagoya City on Monday.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Modest Selling Seen Ahead Of FOMC

- Treasuries are extending session lows across the curve, translating to yields 2.5-3.5bp higher on the day.

- TYZ5 at 113-09, with support at 113-04 (Oct 27 low) after the later cleared the 20-day EMA, after which lies 112-26 (50-day EMA).

- That said recent weakness is deemed corrective from a technical backdrop with a bullish structure still in place with resistance at 113-24 (post-CPI high) before 114-02 (Oct 17 high).

- 2Y yields at 3.514% (+2.4bp), off week to date lows of 3.480% and mid-Oct lows of 3.374%. From a longer-term sense, some might look to fade off the 50d MA of 3.562% (equating to 104-07) as the 2Y yield recovers.

- 10Y yields at 4.010% (+3.6bp) with risks look tilted to the downside again on a medium-term basis with the 50d MA providing resistance since August. The October low is 3.9342% whilst next support moves back up to circa 3.90% (23.6% retrace of the 2020/2023 range). Currently at 3.987%.

- SOFR futures see the day’s losses of up to 3 ticks in the M6. The terminal implied yield of 3.015% (H7) last closed higher on Oct 9, i.e. prior to the increase in US-China trade tensions on Oct 10.

- S&P 500 futures have come close to session lows of 6929.75 after fresh record highs of 6952.00 earlier on. That earlier high came close to projected resistance at 6953.25 (2.00 proj of Aug 1-15-20 price swing) after which lies 6974.04 (3.382 proj), whilst support is seen at 6812.25 (Oct 9 high).

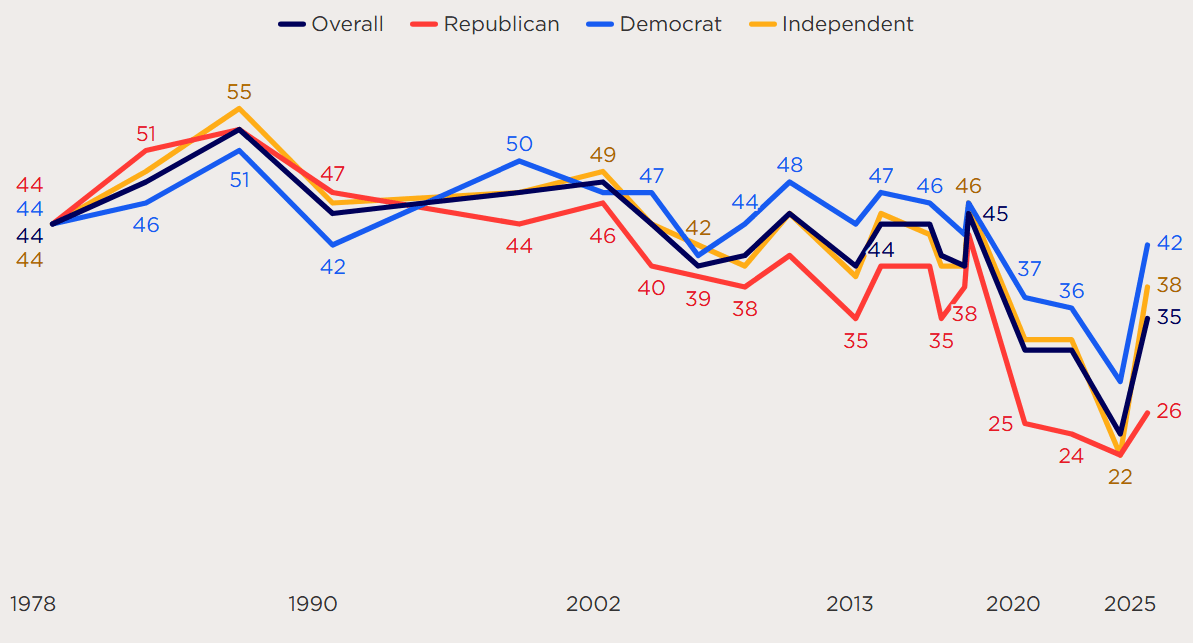

US-CHINA: US Public Sentiment More Positive On China Ahead Of Trump-Xi Meeting

US public sentiment may be shifting back towards a more positive view of China, according to a new survey from the Chicago Council on Global Affairs. The report found that “the bipartisan embrace of US-China competition no longer holds among the public, with partisan differences in perceived threats from China and disagreements on current US-China trade policy.”

- The report notes, “While Republicans continue to favor limiting China’s rise, as well as reductions in trade, and view US-China trade as detrimental to US national security, Democrats have moved in the other direction. Driven by shifts among Democrats and Independents, a majority of Americans now favor a policy of cooperation and engagement with Beijing, oppose higher tariffs, and oppose cuts to bilateral trade.”

- Lingling Wei at the WSJ writes that US President Donald Trump is “poised to relaunch the kind of engagement with Beijing embraced by predecessors from Bill Clinton to Barack Obama—but on Trump’s terms.” Wei notes that Trump's second-term engagement with China is more pragmatic, writing on the expected trade truce extension, "Beyond high-level diplomacy, the truce sets the stage for a tactical stabilization of the relationship over the next year."

Figure 1: American Views of China (100 = more favourable)

Source: Chicago Council on Global Affairs

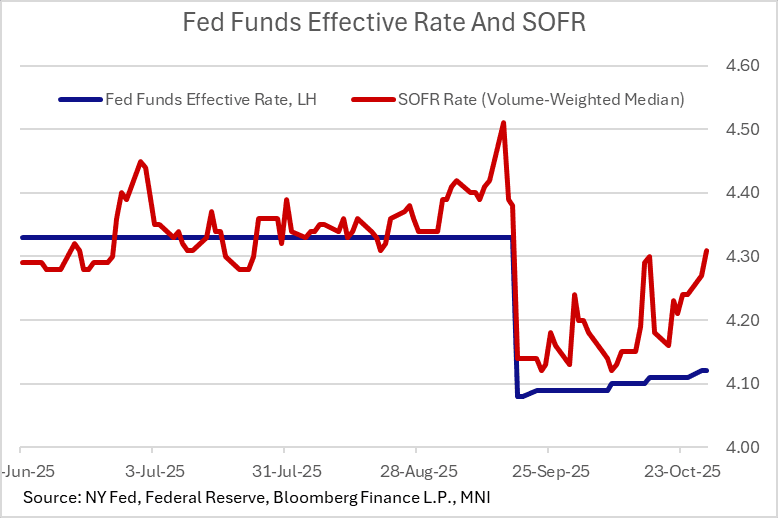

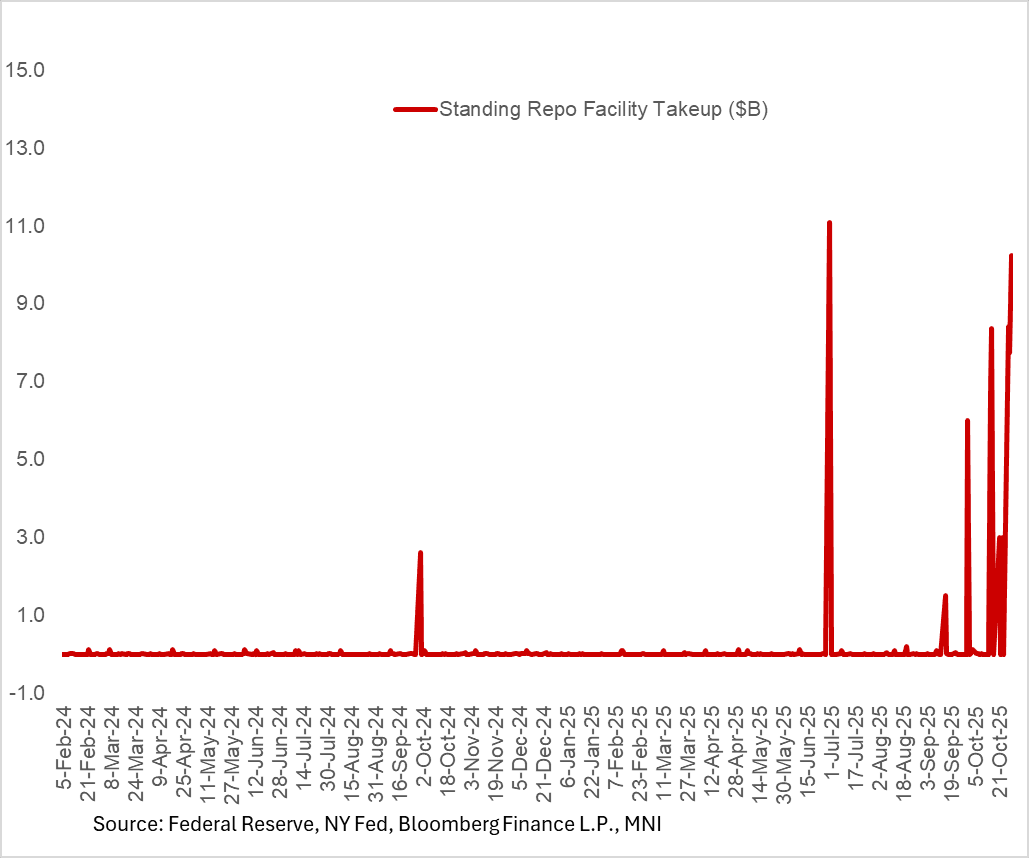

STIR: Effective Fed Funds Steady, But Standing Repo Takeup Rises Again

There was no further upward shift in the effective Fed funds rate Tuesday after Monday's 1bp increase: it printed 4.12%.

- However that comes after 4 increases since the September FOMC meeting (was 4.08%), and Standing Repo Facility takeup rose this morning to a fresh post-June high of $10.2B.

- Both are reminders that funding market pressures were building as the Fed's October decision approached.

New York Fed EFFR for prior session (rate, chg from prev day):

* Daily Effective Fed Funds Rate: 4.12%, no change, volume: $92B

* Daily Overnight Bank Funding Rate: 4.12%, 0.01%, volume: $178B