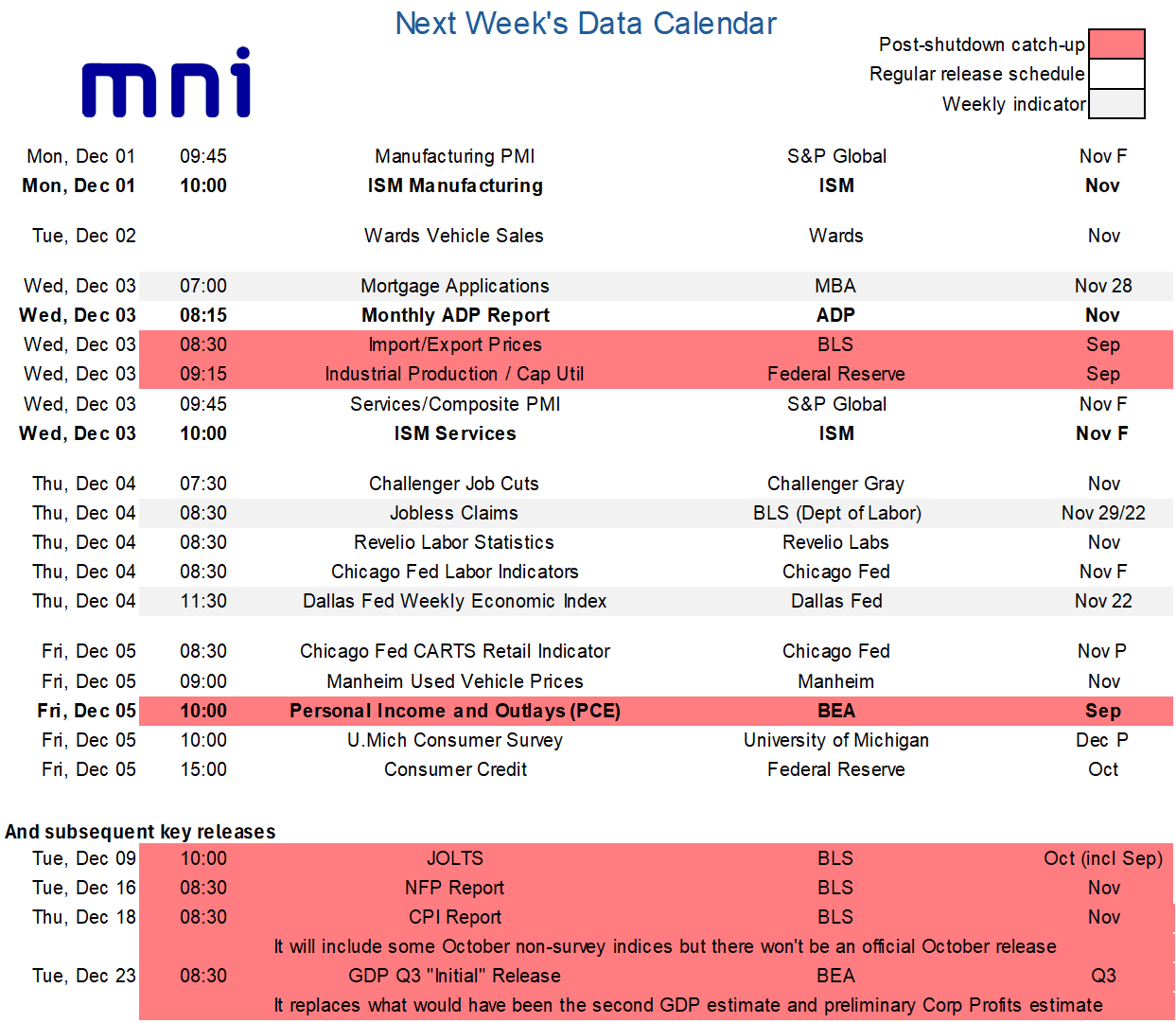

LOOK AHEAD: US Week Ahead: Last Pre-FOMC Labor Data, ISM Surveys & Delayed PCE

Next week would ordinarily have been geared towards a nonfarm payrolls report on Friday but that of course has been rescheduled for Dec 16 as the BLS continues to work its way through the shutdown-induced data backlog. Instead, expect the myriad of labor releases starting Wednesday along with ISM surveys and monthly PCE data to help finalize market expectations ahead of the Dec 9-10 FOMC meeting - we currently anticipate a hawkish cut.

- Within the labor releases, the monthly ADP employment report for November will continue to be important – with declines in recent weekly updates - but we also flag Thursday's releases for Challenger job cuts and Revelio Labs' labor statistics for November. The October Challenger report showed a sharp increase in layoffs to its highest for an October since 2003 along with tepid hiring plans over Sep-Oct combined, whilst the Revelio nonfarm payrolls estimate drew a dovish market reaction last month when it pointed to nonfarm payrolls growth of -9k in October.

- As for ISM surveys, consensus looks for little improvement in Monday’s manufacturing survey, with regional Fed surveys on balance slightly stronger on the month versus a sharp deterioration in the MNI Chicago PMI. The still early days for the services analyst survey sees a modest dip to 52.0 having oscillated between 52.0-52.5 in the previous four months. The service PMI – at 55.0 in the November flash – has been more optimistic in each of the prior six months but with varied beats each time.

- The delayed personal income and outlays report for September then rounds out the week on Friday. This week’s retail sales release will have dampened goods-related expectations for consumer spending. We’ll also watch income dynamics after they underwhelmed in the August report released two months ago, seeing the savings rate dropping to an eight-month low. Core PCE inflation estimates appears to be tracking around 0.22% M/M for September, similar to the 0.23% M/M in August and the 0.24% averaged through May-July although with some seeing scope for minor upward revisions to Aug and Jul.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURJPY TECHS: Bullish Trend Sequence

- RES 4: 181.07 Top of a bull channel drawn from the Feb 28 low

- RES 3: 180.00 Psychological round number

- RES 2: 178.94 1.236 proj of the Jul 31 - Sep 29 - Oct 2 price swing

- RES 1: 178.23 High Oct 27 / Record High

- PRICE: 177.32 @ 16:29 GMT Oct 29

- SUP 1: 176.13 20-day EMA

- SUP 2: 174.53 50-day EMA

- SUP 3: 173.92 Low Oct 6 and a gap high on the daily chart

- SUP 4: 173.24 High Oct 3 and a gap low on the daily chart

The trend structure in EURJPY is bullish and Monday’s fresh cycle high reinforces current conditions. Resistance and the bull trigger at 177.94, the Oct 10 high has been cleared, confirming a resumption of the primary uptrend. 178.94, a Fibonacci projection, is the next key upside level. First support to watch lies at 176.13, the 20-day EMA. Support at the 50-day EMA is at 174.53.

US TSYS: Extending Lows, TYA Testing Latest Support

- Treasuries have continued to extend losses after a hawkish Powell injected some uncertainty around a December rate cut.

- It leaves a solid bear flattening on the day, with yields 7-11.5bp higher on the day.

- 2Y yields have hit 3.604% (+11.6bp) for highs since the weak ADP report on Oct 1.

- They are through a 50d MA of 3.562% (equating to 104-07 in futures) that some might have been looking to fade off as the 2Y yield recovered from mid-October lows.

- 2s10s at 46.4bp (-2.4bp) has cleared September lows of 47.8bp for lows since ~40bp in late July.

- TYZ5 has dipped to a latest session low of 112-25 (-22) as it tests latest support at 112-27 (50-day EMA). Firm clearance could open 112-16+ (Oct 10 low).

- Swap spreads meanwhile have pared some of their initial decline on the FOMC announcement to QT changes, with the 10Y swap spread at -43.5bp vs lows of -44bp and -42.9bps pre-decision. They're still relatively close to yesterday’s -42bp at what was the highest since March.

FOREX: USD Surges as Fed Says December Cut Not Forgone Conclusion

- Fed Chair Powell prompted a significant rally for the dollar late Wednesday, as he explicitly said that an FOMC rate cut in December is not a foregone conclusion. In sympathy, the dollar index is up 0.6% as we approach the APAC crossover, with notable weakness for GBP and CHF standing out today.

- GBP had already been under severe pressure as ongoing fiscal concerns in the UK continue to dampen local sentiment. The greenback rally prompted GBPUSD to briefly extend the day’s declines to 1%. Lows for the session printed at 1.3141, bridging the gap to a key medium-term level on the chart, the August 1 low. The pair has bounced around 30 pips from this level, emphasising its significance.

- Below here, market participants will turn their attention to 1.3041, the Apr 14 low and 1.2971, the 1.382 projection of the Sep 17 - 25 - Oct 1 price swing.

- Elsewhere, USDCHF is currently up 1% on the day, having rallied back above the psychological 0.80 mark. Pressure on the Swiss Franc has been bolstered by EURCHF holding significant medium-term support earlier in the week, now roughly 80 pips above the key 0.9206 level.

- For USDJPY, price erupted through prior session highs at 152.54 to briefly retake the 153.00 handle as we approach the BOJ decision on Thursday. This will keep key resistance at 153.27 firmly in focus, the Oct 10 high and the bull trigger.

- The late dollar bid prompted a solid reversal for USDCAD, having initially been pressured following a hawkish Bank of Canada cut. Having initially broken below 50-day EMA support at 1.3915, the daily close back above this average looks likely to be a false break.

- EURUSD also fell sharply from 1.1640 to print as low as 1.1578 following the Fed. While the ECB meeting is on Thursday, market participants will be eagerly awaiting both GDP and inflation data from the Eurozone over the next two sessions.