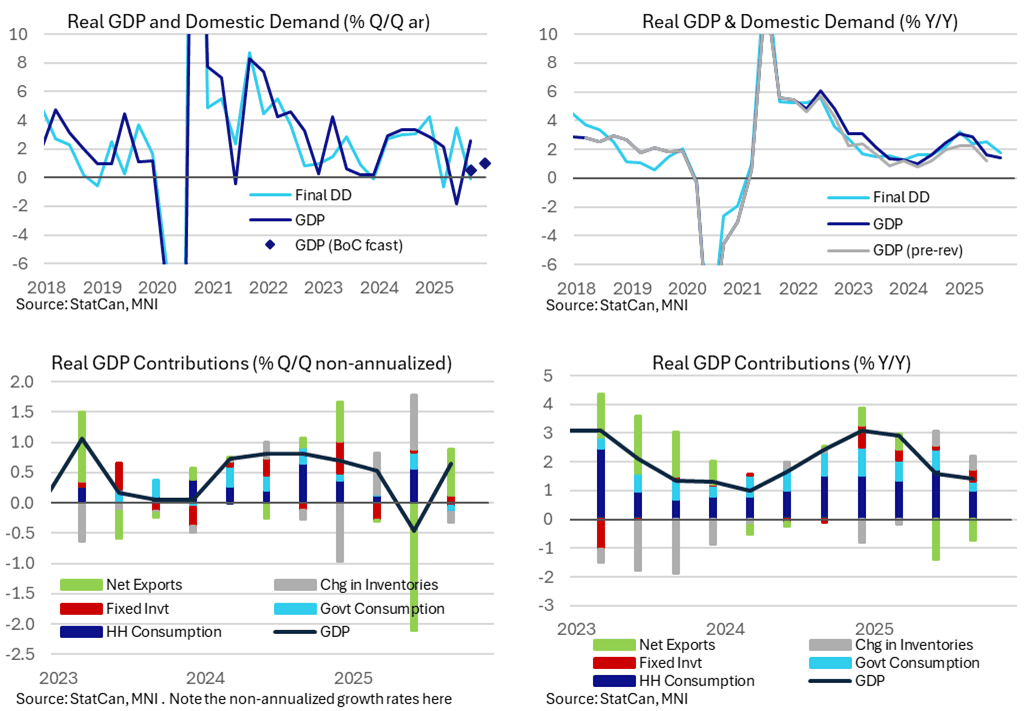

CANADA DATA: Surprise Q3 GDP Jump On Weak Imports, But Upward Revisions As Well

Real GDP growth was much stronger than expected in Q3 as imports fell heavily in continued heightened volatility within trade data. Final domestic demand meanwhile was flat on the quarter after a strong Q2. For a better idea of recent trends, real GDP growth eased two tenths to 1.4% Y/Y after some solid upward revisions whilst domestic demand is a little stronger at 1.7% Y/Y. The BoC last month forecast real GDP growth of 0.5% Y/Y in 4Q25 before 1.6% in both 4Q26 and 4Q27, whilst it estimates potential output growth of 1.6% in 2025, 1.0% in 2026 and 1.3% in 2027.

- As noted at the time, real GDP growth was far stronger than expected in Q3, rising 2.6% annualized vs the BoC forecast of 0.5%.

- There were some wide-ranging revisions to 2022-24, with the Q3 bounce following a larger than first thought decline of -1.8% (initial -1.6) in Q2 but also sizeable upward revisions to prior quarters.

- It left the Y/Y at 1.4% in Q3 after the 1.6% in Q2 was revised up from 1.2%.

- To clarify the confusion from some at the time of the release: Bloomberg shows the annualized print (2.6%) whereas StatCan reports non-annualized (0.6%, 0.645 to be precise).

- However, much of the Q3 strength was driven by a slump in imports (-8.6% annualized) on continued large trade distortions. This time, imports fell after Q2 saw a “significant” increase in “unwrought gold, silver and platinum group metals” along with a base effect from Q2’s import “of a large oil and gas platform module.”

- As cautioned beforehand, trade data are particularly susceptible to revisions, not least because a lack of US data for September, and indeed there was a large revision to Q2 imports (seen at -0.4% annualized vs the -5.1% initially reported). Indeed, “exceptionally this quarter, special estimates on Canadian international merchandise exports to the United States for the reference month of September were produced to compile third quarter statistics.”

- Ultimately, net trade added 3.1pps to real GDP growth on a crude annualized basis after a huge drag of 8.4pps in Q2 when exports slumped -25% annualized in US tariff fallout.

- Final domestic demand meanwhile was subdued at -0.1% annualized after 3.5% in Q2. It has swung from quarter to quarter recently, oscillating between roughly 4% and -0.5% in the past four quarters, but the moderation from 2.5% to 1.7% Y/Y for its softest since 2Q24 tells a clearer story. It tracks above the aforementioned 1.4% Y/Y for real GDP growth in Q3.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GBPUSD TECHS: Clears The Bear Trigger

- RES 4: 1.3527 High Oct 1

- RES 3: 1.3471 High Oct 17 and a key short-term resistance

- RES 2: 1.3422 50-day EMA

- RES 1: 1.3377 20-day EMA

- PRICE: 1.3216 @ 14:46GMT Oct 29

- SUP 1: 1.3195 Intraday low

- SUP 2: 1.3142 Low Aug 1 and a key support

- SUP 3: 1.3041 Low Apr 14

- SUP 4: 1.2971 1.382 proj of the Sep 17 - 25 - Oct 1 price swing

A bear threat in GBPUSD remains present and this week’s sell-off strengthens this theme. The pair has breached 1.3249, the Oct 14 low and a bear trigger. The break confirms a resumption of the downtrend that started Sep 17. Note too that 1.3220 has been pierced, a 0.764 projection of the Sep 17 - 25 - Oct 1 price swing. This signals scope for a move towards key support at 1.3142, Aug 1 low. Initial resistance is 1.3377, the 20-day EMA.

EURGBP TECHS: Resumes Its Uptrend

- RES 4: 0.8865 1.764 proj of the Sep 15 - 25 - Oct 8 price swing

- RES 3: 0.8848 1.618 proj of the Sep 15 - 25 - Oct 8 price swing

- RES 2: 0.8835 High May 3 2023

- RES 1: 0.8818 Intraday high

- PRICE: 0.8812 @ 14:43 GMT Oct 29

- SUP 1: 0.8751 High Sep 25

- SUP 2: 0.8710 20-day EMA

- SUP 3: 0.8688 50-day EMA

- SUP 4: 0.8656 Low Oct 8 and a key support

A bull trend in EURGBP remains intact. Tuesday’s strong gains resulted in a clear break of resistance 0.8769, the Jul 28 high and a bull trigger. This, together with today’s extension, confirms a resumption of the uptrend and maintains the bullish price sequence of higher highs and higher lows. The 0.8800 handle has been cleared, sights are on 0.8835, the May 3 2023 high. Initial support lies at 0.8751, the Sep 25 high.

US TSY OPTIONS: US 5yr Put buyer

FVZ5 108.75p, bought for '04 in 2k.