MNI ASIA MARKETS ANALYSIS:Tsy Ylds Decline Ahead Key Jobs Data

HIGHLIGHTS

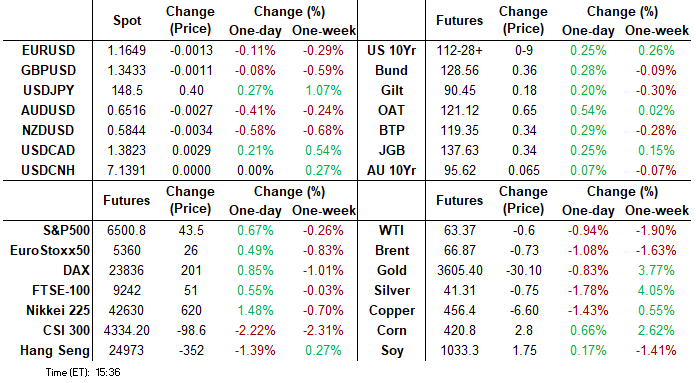

- Treasuries looking to extend late session highs, 10s testing initial technical resistance (112-28.5: 2.000 proj of the Jul 15 - 22 - 28 price swing) with focus on Friday's key employment data for August.

- Projected rate cuts into year end gained slightly (Dec'25 near -60bp priced in) despite this morning's mixed data kicked off by soft ADP private jobs gain (+54k vs. +68k est, 106k prior rev).

- US$ and Equities gained - undeterred by some slightly softer ADP and claims data, and moderately boosted by an above-expectation ISM services release.

US TSYS

MNI US TSYS: Rates Near Highs Ahead Friday's Key August Employ Report

- Treasuries look to finish moderately higher, near Thursday session highs after this morning's data. Treasury futures gapped higher then quickly reversed/pared gains after lower than expected ADP private jobs gain (+54k vs. +68k est) (prior up-revised slightly). ADP employment has pointed to subdued private sector hiring for some months now, with the three-month average inching up to 46k in August.

- Weekly jobless claims gained slightly (237k vs. 230k est, 229k prior) while continuing claims came out lower than expected (1.940M vs 1.959M est, prior down-revised to 1.944M). Unit Labor Cost slightly lower than expected - but prior is up-revised significantly.

- Meanwhile, August's ISM Services report was stronger than expected in most major categories, with the headline index rising to a 6-month high 52.0 from 50.1 prior (and vs 51.0 Bloomberg consensus). This was a solid report but there was still ample evidence of tariff-related effects on business activity.

- Currently, the Dec'25 10Y trades +8.5 at 112-28 (yld 4.1684 -.0483) - just off session high at 112-28.5 -- Initial technical resistance: 2.000 proj of the Jul 15 - 22 - 28 price swing. Support below at 112-01.5 (20-day EMA). Curves bull flatten: 2s10s -1.664 at 58.146, 5s30s -0.647 at 119.627.

- USD index slowly ground higher (BBDXY +1.54 at 1207.06) undeterred by some slightly softer ADP and claims data, and moderately boosted by an above-expectation ISM services release. Overall, the moves have been relatively contained (DXY up 0.25%) ahead Friday's key employ data.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.39% (+0.00), volume: $2.880T

- Broad General Collateral Rate (BGCR): 4.36% (+0.00), volume: $1.146T

- Tri-Party General Collateral Rate (TCR): 4.36% (+0.00), volume: $1.118T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $119B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $218B

FED Reverse Repo Operation

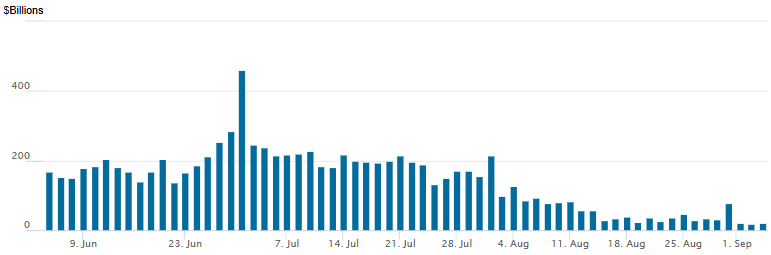

RRP usage inched up to $20.128B with 17 counterparties this afternoon from $17.923B yesterday - lowest levels since early April 2021. Compares to this year's high usage of $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury options remain mixed Through Thursday's session, underlying futures near moderate session highs ahead of Friday's August employment data. Projected rate cuts hold steady to mildly higher vs. morning (*) levels: Sep'25 steady at -24.7bp, Oct'25 at -38.6bp (-38.1bp), Dec'25 at -59.6bp (-58.9bp), Jan'26 at -71.6bp (-70.6bp).

SOFR Options:

6,000 SFRZ5 95.81/95.93/96.06 put flys

+7,000 0QV5 97.25 calls, 6.0 vs. 97.025/0.28%

+8,000 SFRX5 96.50 calls, 5.5 vs. 96.265/0.22%

+10,000 SFRV5 96.37/96.56 call spds, 3.0

+5,000 SFRV5 96.00/96.12 put spds 1.5 over 96.50/96.62 call spds vs. 96.25/0.25%

+2,000 0QV5 97.12/97.62 call spds 3.0 over SFRV5 96.31/96.62 call spd

-8,000 SFRV5 96.50/96.62 call spds, 1.25 ref 96.26

-6,000 SFRZ6 96.50 puts, 17.0 vs. 97.01/0.28%

-1,000 SFRU5 95.93 straddles, 7.75 ref 95.9275

-1,000 SFRU5 95.81/96.06 strangles, 2.0 ref 95.93

6,300 0QX5 96.50/97.50 strangles ref

Block, 2,500 SFRU5 95.81 put vs. 2QU5 96.87 put spd, 1.25 net

3,000 SFRV5 96.00/96.06 put spds ref 96.255

+2,500 SFRU5 96.12/96.25 call spds, 0.5

3,500 SFRU5 96.00/96.12 call spds

1,250 SFRX5 95.87/96.00/96.12 put flys ref 96.26

+2,000 SFRZ5 95.81/95.93/96.06 put flys, 1.75

-3,100 SFRZ5 95.75/95.87/96.00/96.12 put condors, 2.5

+4,000 SFRH6 96.43/96.56 call spds 4.5 over 95.75/95.87 put spds

5,000 0QZ5 97.00/97.62 1x2 call spds, 12.5 ref 97.025

+1,300 0QU5 97.00/97.12/97.25 call flys, 2.0 ref 96.93

Treasury Options:

2,750 FVV5 108/109 put spds ref 109-19.75

1,400 TYZ5 115.5 calls vs. 110/111 put spds ref 112-26.5

2,000 FVV5 110.5 calls, 10 total over 10,300

3,400 USZ5 107 puts, 23 ref 114-29

11,500 TYV5 108/109 put spds ref 112-23.5

-2,000 TYV5 113.5 calls, 22

+2,000 TYV5 112 puts, 22

+2,000 TYX5 110/111 put spds, 10 ref 112-23

+2,000 wk1 TY 112.5/113 2x3 call spds, 20 ref 112-22 (exp 9/5)

over 6,000 FVV5 108.75 puts, 9.5 last ref 109-17

over -5,900 FVX5 110.5 calls, 19.5 last

2,500 wk1 TY 112.25/113 1x2 call spds ref 112-17

4,000 FVV5 108.75 puts, 8.5 vs. 109-17/0.22%

4,000 TYV5 114/115 1x2 call spds, 1.0 ref 112-17

MNI BONDS: EGBs-GILTS CASH CLOSE: Long-End Relief Rally Extends

European long-end yields declined for a second day Thursday.

- The rally in core FI that started early Wednesday continued unimpeded for much of the morning session, helped in part by softer oil prices and solid digestion of European supply, including Spanish and French auctions.

- The latest BoE DMP survey pointed to a softening employment picture, while a strong 20Y linker auction saw a bull flattening move in Gilts extend. In other data, Eurozone July retail sales were on the soft side.

- The fall in yields was interrupted in mid-afternoon, with equities rallying and US ISM Services headline data proving stronger-than-expected, but yields ultimately closed lower on the day.

- The German and UK curves both bull flattened, with Gilts outperforming Bunds.

- Periphery/semi-core EGB spreads tightened by around 2bp alongside the pickup in equities and aforementioned smooth EGB auction digestion.

- Friday's European calendar includes German factory orders and UK retail sales data (as well as Eurozone Q2 GDP revisions/details and labour market figures), while global focus will be on the US employment report later in the session.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.2bps at 1.964%, 5-Yr is down 1bps at 2.27%, 10-Yr is down 2.1bps at 2.719%, and 30-Yr is down 1.9bps at 3.337%.

- UK: The 2-Yr yield is down 1.1bps at 3.949%, 5-Yr is down 2bps at 4.11%, 10-Yr is down 2.8bps at 4.72%, and 30-Yr is down 2.9bps at 5.574%.

- Italian BTP spread down 2.3bps at 85bps / French OAT down 2.3bps at 77.6bps

MNI EGB OPTIONS: Schatz / Bund Flow Focused On Put Structures

Thursday's Europe rates/bond options flow included:

- DUV5 107.10 puts 3K given at 9

- DUX5 107.20/107.10/107.00/106.80 put condor paper paid 0.5 on 5K

- RXV5 127/126 put spread paper paid 10.5 on 3K

- RXV5 127.00 puts 6K blocked at 17, looks like a buyer

- ERZ5 98.0625/98.125/98.25/98.375 call condor, paper pays 1.5 in 7.75k

- SFIZ5 96.25/96.35/96.45 call fly, paper sells 3k at 1.75

MNI FOREX: Dollar Firmer as Payrolls Awaited, NZDUSD Eyes Key Support

- Aside from a very brief dip in APAC trade, the USD index has been slowly grinding higher on Thursday, undeterred by some slightly softer ADP and claims data, and moderately boosted by an above-expectation ISM services release. Overall, the moves have been relatively contained (DXY up 0.25%) given the imminent release of the highly significant US employment report on Friday.

- These moves come despite solid demand for the major equity benchmarks and lower US yields, and therefore could be more reflective of positioning ahead of the Friday’s data.

- As usual, USDJPY has been an accurate reflection of the broader greenback price action, with a brief dip to 147.80 well supported in Asia, and the pair then rallying around 10 pips in steady fashion to session highs of 148.78. Solid resistance is seen at 149.12/14, a level that could come under threat should a further weakening of the US labour market not materialise.

- The stronger dollar in the aftermath of the US data continues to weigh most notably on the likes of AUD and NZD, which currently have session losses of 0.5 and 0.65% respectively.

- NZDUSD price action narrows the gap to the aforementioned key double bottom and psychological support at 0.5800. A break of this level would strengthen bearish conditions and signal a move towards 0.5728, the 61.8% retracement of the Apr-Jul rally.

- For AUDUSD, initial resistance between 0.6560/70 held well on Wednesday, despite the firmer-than-expected GDP reading. Support for the pair remains further out, at 0.6415, the Aug 21 / 22 low. A clear break of it would resume a bear leg and highlight a stronger reversal pattern.

- Kiwi weakness slightly outpacing its regional peer sees AUDNZD trade to fresh cycle highs of 1.1157, narrowing the gap to a key medium-term level at 1.1180.

MNI FX OPTIONS: Expiries for Sep05 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1550(E1.6bln), $1.1600(E2.1bln), $1.1700(E964mln), $1.1740-50(E1.6bln), $1.1775-80(E1.2bln), $1.1800(E1.3bln)

- USD/JPY: Y146.00($2.4bln), Y146.95-00($1.3bln), Y147.40-50($957mln), Y148.85-00($679mln)

- AUD/USD: $0.6400(A$1.1bln), $0.6500-10(A$1.5bln), $0.6600(A$1.0bln)

- USD/CAD: C$1.3720-30($917mln), C$1.3850-60($1.1bln)

MNI US STOCKS: Late Equities Roundup: Retail & Financial Shares Outperforming

- Stocks are drifting higher late Thursday, major indexes extending highs for the week ahead of Friday's headline employment report for August (+75k est vs. +73k prior). Optimism was cautious, however, after this morning's ADP employment came out softer than expected in August at 54k (cons 68k).

- Currently, the DJIA trades up 293.96 points (0.65%) at 45565.04, S&P E-Minis up 37 points (0.57%) at 6494, Nasdaq up 128.2 points (0.6%) at 21626.51.

- Consumer Discretionary and Financial sector shares continued to outperform in the second half, distribution and retail shares buoyed the former: Williams-Sonoma +4.68%, Amazon.com +4.10%, Genuine Parts +3.37% and PulteGroup Inc +3.33%.

- Banks and services shares supported the Financial sector: T Rowe Price Group +5.78%, Raymond James Financial +2.32%, Goldman Sachs Group +2.29% and Capital One Financial +2.16%.

- Meanwhile, a mix of Utilities and Consumer Staples sector shares underperformed in late trade, anchoring indexes rise somewhat ahead Friday's data risk: NiSource -5.83%, AES Corp -4.61%, Edison International -2.03% and American Electric Power -1.76% weighed on the Utilities sector, while Estee Lauder -4.39%, Dollar Tree -3.08%, The Campbell's Company -2.77% and Philip Morris International -1.94% weighed on Staples.

MNI EQUITY TECHS: E-MINI S&P: (U5) Remains Above Support

- RES 4: 6600.00 Round number resistance

- RES 3: 6585.83 2.0% 10-dma envelope

- RES 2: 6543.75 2.00 proj of the Apr 7 - 10 - 21 price swing

- RES 1: 6523.00 High Aug 28 and the bull trigger

- PRICE: 6497.75 @ 1455 ET Sep 4

- SUP 1: 6371.75 Low Sep 2

- SUP 2: 6340.81 50-day EMA

- SUP 3: 6313.25 Low Aug 6

- SUP 4: 6239.50 Low Aug 1 and a key support

A bull cycle in S&P E-Minis remains intact and the latest pullback is - for now - considered corrective. Price has traded through the 20-day EMA. The key support to watch lies at the 50-day EMA, at 6340.81. A clear break of this EMA is required to signal scope for a deeper retracement. This would open 6239.50, the Aug 1 low and a key support. Moving average studies still highlight a dominant uptrend. The bull trigger is 6523.00, the Aug 28 high.

MNI COMMODITIES: Crude Falls Further, Precious Metals Pull Back

- Oil prices have fallen further on Thursday despite a surprise US crude build as fears grow over potential further OPEC+ cut unwinds this weekend.

- WTI Oct 25 is down by 0.7% at $63.5/bbl.

- The US EIA said energy firms added 2.4mn barrels of crude into storage during the week ended August 29.

- A bear cycle in WTI futures remains intact and the latest bull phase appears to have been a correction. Yesterday’s move down highlights a possible early reversal signal and the end of the corrective phase.

- Initial support is seen at $61.29, the Aug 13 low and the bear trigger. Clearance of this level would pave the way for a move towards $57.71, the May 30 low.

- Meanwhile, precious metals have pulled back today after this week’s strong rally, with spot gold down by 0.4% at $3,546/oz and silver falling by 1.6% to $40.6/oz.

- The move has come as the US dollar has ground slowly higher today, ahead of tomorrow’s highly significant US employment report.

- For gold, a clear bull cycle remains in play, with initial resistance at $3,578.5, the Sep 3 high, followed by the $3,600 handle next.

- Trend signals for silver are also still bullish, with the metal holding on to the bulk of this week’s gains. Sights are on the $42.0 handle next.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 05/09/2025 | 0600/0800 | ** | Manufacturing Orders | |

| 05/09/2025 | 0600/0700 | *** | Retail Sales | |

| 05/09/2025 | 0645/0845 | * | Foreign Trade | |

| 05/09/2025 | 0800/1000 | * | Retail Sales | |

| 05/09/2025 | 0900/1100 | * | Employment | |

| 05/09/2025 | 0900/1100 | *** | EZ GDP 3rd (Regular) | |

| 05/09/2025 | 1230/0830 | *** | USDA Crop Estimates - WASDE | |

| 05/09/2025 | 1230/0830 | *** | Employment Report | |

| 05/09/2025 | 1230/0830 | *** | Employment Report | |

| 05/09/2025 | 1230/0830 | *** | Employment Report | |

| 05/09/2025 | 1230/0830 | *** | Employment Report | |

| 05/09/2025 | 1230/0830 | *** | Employment Report | |

| 05/09/2025 | 1230/0830 | *** | Employment Report | |

| 05/09/2025 | 1230/0830 | *** | Labour Force Survey | |

| 05/09/2025 | 1400/1000 | * | Ivey PMI | |

| 05/09/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 05/09/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |