MNI ASIA MARKETS ANALYSIS: Ylds Decline Ahead Sans-Jobs Friday

HIGHLIGHTS

- Treasuries look to finish modestly high, gradually see-sawing off early morning lows to near late session highs, curves flatter with bonds outperforming.

- No weekly jobless claims or factory orders today due to the Govt shutdown - most likely preventing the BLS September employment from being released Friday as well.

- September's ISM Services report expected tomorrow at 1000ET, seen showing a slight fading in activity vs August, along with a softening in inflationary pressures.

- Early Friday focus shifts back to Europe, with key releases including final PMI prints across the continent as well as the industrial/manufacturing production prints in France.

US TSYS

MNI US TSYS: Continue to Extend Highs Ahead No-Employment Data Friday

- US Treasuries hold narrow range in the second half after extend session highs into midday - no obvious headline or flow driver though US$ did scale back from midday highs (Bbg US$ index +1.39 at 1201.54 vs. 1204.58 high) while stocks finished stronger (SPX & Nasdaq making new record highs earlier).

- Currently, TYZ5 +3 at 112-30, 10Y yield -.0135 to 4.0846%. Initial firm resistance to watch is unchanged, at 113-00, the Sep 24 high. A break would be bullish with next levels to watch at: 113-12/29 (High Sep 18 / High Sep 11 and the bull trigger). Curves remain flatter: 2s10s -1.763 at 54.169, 5s30s -1.483 at 102.137.

- No weekly jobless claims or factory orders today due to the Govt shutdown - Challenger, Gray & Christmas, however, reported job cut announcements fell 25.8% Y/Y in September, less severe than consensus which had expected a 13.3% rise.

- Friday's September employment report from the BLS most likely will NOT be released tomorrow despite Sen Warren (Dem) telling CNN the "labor data has been collected and is likely ready to be released". "Let’s be clear," Warren added, "the jobs data scheduled to come out this Friday has undoubtedly been collected and the President must release it."

- Bloomberg consensus for ISM Services (1000ET) eyes a small increase to 51.5 from 50.8 in a second monthly improvement after the 49.9 in May was its lowest since Jun 2024, with prices paid looking to remain elevated.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.20% (-0.04), volume: $3.075T

- Broad General Collateral Rate (BGCR): 4.16% (-0.04), volume: $1.154T

- Tri-Party General Collateral Rate (TCR): 4.16% (-0.04), volume: $1.119T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.09% (+0.00), volume: $103B

- Daily Overnight Bank Funding Rate: 4.09% (+0.00), volume: $180B

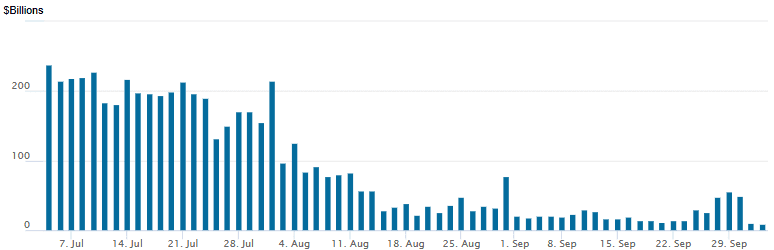

FED Reverse Repo Operation - New Multi Year Low

RRP usage continues to recede to the lowest level since early April 2021: $8.436B with 10 counterparties this afternoon, down from $10.179B Wednesday. Compares to the year's high usage of $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR/Treasury option trade continued to revolve around more consistent low delta call structures Thursday with the exception of some large put trades, highlight: large Dec'25 SOFR Put fly buyer* hedge for a no rate-cut hedge at year end. Underlying Tsy futures near modest session highs, SOFR steady to mixed - short end weaker as projected rate cut pricing drifts near late Wednesday levels (*): Oct'25 at -24.5bp (-25.3bp), Dec'25 at -46.8bp (-46.9bp), Jan'26 at -58.5bp (-58.8bp), Mar'26 at -70.6bp (-70.0bp).

SOFR Options:

Block: 12,750 SFRZ5 96.43 calls 1.25 over 96.12/96.25 put spds vs. 96.345/0.50%

+3,000 SFRF6 96.37/96.50/96.62/96.75 call condors, 3.75 ref 96.545

+5,000 SFRZ5 96.12/96.25 put spds 1.0 over 96.43 calls

+10,000 SFRV5 96.18/96.50 strangles

+8,000 SFRH6 96.50/96.68/96.87/97.06 call condors, 5.0 vs. 96.55/0.10%

+5,000 0QU6 98.00 calls, 5.0 ref 96.89

*+50,000 SFRZ5 96.12/96.18/96.25 put flys, .75 ref 96.34 (no cut hedge)

2,000 SFRZ5 96.37/96.50/96.62 call flys vs. 96.00/96.18 put spds ref 96.35

+5,000 SFRH6 95.75/95.87 put spds, .25 ref 96.56

3,000 0QZ5 97.06/97.37/3QZ5 96.75/97.00 call spd spd, 0.5 net

6,000 SFRZ5 96.25/96.31/96.50/96.56 call condors, 3.75 ref 96.345

Block, +2,500 SFRU6/2QU6 96.87/97.37 call spd spds 1.0 net steepener at 0657:46ET

Block, +5,000 SFRZ5 96.56/96.68 call spds, 1.0-1.25 at 0648:19ET

+5,000 SFRZ5 96.43/96.56 call spds, 1.75 ref 96.35

Block, +5,500 SFRZ5 96.31/0QZ5 97.12 call spds, 0.5-1.0 net at 0424:37ET-0643:53ET

-2,200 0QX5 96.37 puts, 0.5

9,000 0QZ5 96.25/96.56 2x1 put spds, 1.0 ref 96.975

5,000 0QZ5 96.25 puts, ref 96.975

Treasury Options:

-8,000 TYZ5 111.5/114 strangles, 45

over 22,000 USX5 108 puts ref 117-03 to -05

5,000 TYX5 112.5/113 strangles, 1-26

+20,000 FVX5 109.75 calls, 11.5 ref 109-11.75

+2,000 FVX5 110.25 calls, 6.5 ref 109-15

7,100 TYX5 114 calls, 11 ref 112-28.5

+2,600 TYZ5 112.5/113/114/114.5 call condors, 9 ref 112-30.5

5,000 wk2 TY 113.5 calls (exp 10/10)

-1,600 TYX5 111.75 puts, 10 vs. 112-24/0.20%

MNI BONDS: EGBs-GILTS CASH CLOSE: Gilts Marginally Underperform Bunds

Bunds outperformed Gilts Thursday.

- After a flat start, yields started to descend in mid-morning London trade, with the implications of the US government shutdown still being digested.

- There was a sharp rise in yields in early afternoon however, with no discernable trigger (some cited US Treasury Secretary Bessent indicating an imminent "breakthrough" in relations with China).

- However the move faded as equities turned lower, leading core yields to close near their session lows (in the case of Bund) or in the middle of the daily range (Gilt).

- UK fiscal woes remained a background theme, with an FT report has reaffirmed existing estimates surrounding the fiscal "black hole" (~GBP30bln).

- In data, the UK DMP survey has "got something for both the more dovish and more hawkish members", as MNI's Macro team wrote, so didn't change the BOE outlook. Also, Swiss CPI inflation printed unchanged and marginally below consensus at 0.2% Y/Y in September.

- The German curve bull flattened on the day, with Gilts bear steepening. Periphery/semi-core EGB spreads widened slightly.

- Friday's calendar includes final Services/Composite PMIs (the only reading, in Italy and Spain's case), along with French industrial production and Italian fiscal data. There are multiple central bank speakers scheduled including ECB's Lagarde and BOE's Bailey.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.3bps at 2.01%, 5-Yr is down 0.4bps at 2.297%, 10-Yr is down 1.4bps at 2.699%, and 30-Yr is down 2.4bps at 3.274%.

- UK: The 2-Yr yield is up 1.9bps at 3.984%, 5-Yr is up 2bps at 4.137%, 10-Yr is up 1.4bps at 4.71%, and 30-Yr is up 0.6bps at 5.517%.

- Italian BTP spread up 0.7bps at 82bps / French OAT up 0.5bps at 82.2bps

MNI EGB OPTIONS: Sonia Call Structure Activity Remains Prevalent, With OATs Emerging

Thursday's Europe rates/bond options flow included:

- OATZ5 102p, bought for 2 in 1.25k

- RXX5 127.5/129.5RR, sold the call and receives half a tick in 2k

- RXX5 128/127ps 1x1.5, bought for 15 in 3k

- RXZ5 130.50c, bought for 25.5 and 26 in 11k

- RXX5 125p, bought for 1 in 3k.

- ERM6 98.12/98.25cs vs ERH6 97.93/97.81ps, bought the cs for 2.5 in 5k

- ERZ6 97.93/97.81/97.68/97.56p condor, bought for 1.5 in 3k

- SFIM6 96.30/96.40/96.50 call fly & 96.55/96.65/96.75 call fly paper paid 1.75 on 6K as strips

- SFIM6 96.60/96.80cs, bought for 3.5 in 3k

- 0NH6 96.50/96.70cs, bought for 6 in 3k

MNI FOREX: USD Rallies to End Losing Streak, Lack of Data Unlikely to Deter Fed

- After several sessions of losses, the USD clawed back lost ground into the Thursday close, snapping losses posted into the beginning of the US government shutdown. While weekly jobless claims data was another victim of the agency closures, markets looked to private sector proxies as a guide, with some alternative metrics pointing to a stronger labor market turnout in September than expected.

- Friday's NFP print will not go ahead, and while this leaves the Fed with fewer datapoints to aide their decision-making, it's not expected to deter the FOMC from a second rate cut at their October meeting. The USD rally into the close stood out for EUR, prompting EUR/USD to trade through to new weekly lows, with the move accelerating on the break of both 1.1712 and 1.1696 - both intraday retracements for the bounce of last week's lows.

- A break higher for USD/CAD into the European close also drew focus. The pair made light work of resistance into the late August highs at 1.3925 as well as last week's highs of 1.3959. Resultantly, spot traded to the best level since May to challenge the 200-dma of 1.3989. Clearance here would be a major bullish development and isolate 1.4016 as the bull trigger.

- Lastly for GBP/USD, weakness Thursday on the 15min candle chart shows the breakdown in GBP/USD has pressed price through the up-trendline drawn off the pullback low at 1.3324. The pullback has steadied into 1.3426 - a retracement level - but clearance here opens 1.3372-1.3402 intraday.

- Focus Friday shifts back to Europe, with key releases including final PMI prints across the continent as well as the industrial/manufacturing production prints in France. While there will be no BLS payrolls data, the ISM Services Index will still go ahead, and may raise extra market attention given the lack of official government releases.

MNI FX OPTIONS: Expiries for Oct03 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1700(E1.3bln), $1.1845-55(E2.2bln), $1.1875(E1.2bln)

- USD/JPY: Y146.00($1.3bln), Y147.00($845mln), Y148.00($1.0bln)

- EUR/GBP: Gbp0.8785-05(E1.1bln)

- AUD/USD: $0.6600(A$1.9bln)

- NZD/USD: $0.6450(N$1.2bln)

MNI US STOCKS: Late Equities Roundup: Late Session Rally, DJIA Nearing Record High

- Stocks are gaining again late Thursday - attempting to surpass early session highs* after the Nasdaq & SPX indexes quietly made new record highs (the DJIA still off record high of 46,714.27 from September 23).

- Currently, the DJIA is up 131.64 points (0.28%) at 46,572.77, S&P E-Minis up 8.5 points (0.13%) at 6,770.25 (*6782.25 record high), Nasdaq up 94.6 points (0.4%) at 22,849.91 (*22900.60 record high).

- Information Technology and Materials sector shares continued to outperform in the second half, Advanced Micro Devices +3.55%, Intel Corp +3.01%, Applied Materials +2.78% and First Solar +2.62% buoyed the Tech sector.

- On a side note, financial services company Fair Isaac Corp surged +21.07% after launching FICO Mortgage Direct License Program this morning.

- Meanwhile, the Materials sector was buoyed by: CF Industries Holdings +3.75%, Albemarle +3.56%, Eastman Chemical +3.36% and Dow Inc +3.04%.

- A combination of Energy, Real Estate and Consumer Discretionary sector shares continued to underperform in the second half. Oil and gas stocks weighed on the Energy sector as crude prices declined (WTI -1.27 at 60.51): Occidental Petroleum -7.90%, Coterra Energy -3.59%, Targa Resources -3.22% and APA -3.13%.

- Office & health care investment trusts weighed on the Real Estate sector: Welltower -1.79%, BXP -1.47%, UDR -1.16% and Federal Realty Investment Trust -1.13%.

- Auto- and travel-related shares weighed on the Discretionary sector: Tesla -4.11%, General Motors -2.81%, Airbnb -1.43% and TJX -1.05%.

MNI EQUITY TECHS: E-MINI S&P: (Z5) Fresh Cycle High

- RES 4: 6812.29 2.382 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 3: 6800.00 Round number resistance

- RES 2: 6787.63 1.382 proj of the Aug 1 - 15 - 20 price swing

- RES 1: 6782.25 Intraday high

- PRICE: 6779.00 @ 14:36 BST Oct 2

- SUP 1: 6666.25 20-day EMA

- SUP 2: 6611.00 Low Sep 17

- SUP 3: 6550.28 50-day EMA

- SUP 4: 6506.50 Low Sep 5

A bull cycle in S&P E-Minis remains intact. The contract has again traded to a fresh cycle high to confirm a resumption of the uptrend and maintain the positive price sequence of higher highs and higher lows. Sights are on 6787.63, a Fibonacci projection. Initial support to watch is at the 20-day EMA, at 6666.25. It has recently been pierced, a clear break of it would signal scope for a deeper pullback, potentially towards the 50-day EMA, at 6550.28.

MNI COMMODITIES: Crude Extends Losses, Gold Pulls Back From Fresh Record High

- Crude prices have fallen to their lowest since June amid oversupply concerns ahead of Sunday’s OPEC meeting.

- WTI Nov 25 is down by 2.0% at $60.6/bbl.

- OPEC is expected to continue to unwind previous output reductions when it meets. It increased the October target by 137kb/d and at least that amount is likely in November although with conflicting reports on the size of a potential hike.

- Following the G7 finance ministers meeting, meanwhile, an agreement on substantial additional sanctions on Russia’s means to finance its war in Ukraine is close, Bloomberg said.

- Today’s move lower has seen WTI futures pierce key support at $60.85, the Aug 13 low. A clear break of this level would reinstate the downtrend, opening $57.50, the May 30 low.

- Meanwhile, spot gold has extended the pull away from fresh all-time highs of $3,896.9/oz reached earlier in the session, leaving round number resistance at $3,900/oz intact.

- Spot is currently 0.5% lower on the session at $3,847.

- The move lower seems to be a function of the stronger USD today, potentially exacerbated by profit taking.

- Nonetheless, a bull cycle in gold remains in play, with moving average studies in a bull-mode position, highlighting a dominant uptrend.

- Beyond the $3,900 level, sights are on $3,909.4, a Fibonacci projection. On the downside, support to watch lies at $3,714.1, the 20-day EMA. A pullback would be considered corrective.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 03/10/2025 | 0645/0845 | * | Industrial Production | |

| 03/10/2025 | 0700/0300 | * | Turkey CPI | |

| 03/10/2025 | 0715/0915 | ** | S&P Global Services PMI (f) | |

| 03/10/2025 | 0715/0915 | ** | S&P Global Composite PMI (final) | |

| 03/10/2025 | 0745/0945 | ** | S&P Global Services PMI (f) | |

| 03/10/2025 | 0745/0945 | ** | S&P Global Composite PMI (final) | |

| 03/10/2025 | 0750/0950 | ** | S&P Global Services PMI (f) | |

| 03/10/2025 | 0750/0950 | ** | S&P Global Composite PMI (final) | |

| 03/10/2025 | 0755/0955 | ** | S&P Global Services PMI (f) | |

| 03/10/2025 | 0755/0955 | ** | S&P Global Composite PMI (final) | |

| 03/10/2025 | 0800/1000 | * | Retail Sales | |

| 03/10/2025 | 0800/1000 | ** | S&P Global Services PMI (f) | |

| 03/10/2025 | 0800/1000 | ** | S&P Global Composite PMI (final) | |

| 03/10/2025 | 0830/0930 | ** | S&P Global Services PMI (Final) | |

| 03/10/2025 | 0830/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 03/10/2025 | 0900/1100 | ** | EZ PPI | |

| 03/10/2025 | 0940/1140 | ECB Lagarde Speech At Knot Farewell Symposium | ||

| 03/10/2025 | 1000/0600 | NY Fed's John Williams | ||

| 03/10/2025 | 1230/0830 | *** | Employment Report | |

| 03/10/2025 | 1230/0830 | *** | Employment Report | |

| 03/10/2025 | 1230/0830 | *** | Employment Report | |

| 03/10/2025 | 1230/0830 | *** | Employment Report | |

| 03/10/2025 | 1230/0830 | *** | Employment Report | |

| 03/10/2025 | 1230/0830 | *** | Employment Report | |

| 03/10/2025 | 1320/1420 | BOE Bailey Keynote At Knot Farewell Symposium | ||

| 03/10/2025 | 1345/0945 | *** | S&P Global Services Index (final) | |

| 03/10/2025 | 1345/0945 | *** | S&P Global US Final Composite PMI | |

| 03/10/2025 | 1350/1550 | ECB Schnabel In Panel At Knot Farewell Symposium | ||

| 03/10/2025 | 1400/1000 | *** | ISM Non-Manufacturing Index | |

| 03/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 03/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 03/10/2025 | 1740/1340 | Fed Vice Chair Philip Jefferson | ||

| 03/10/2025 | 2200/1800 | NY Fed's John Williams |