OPTIONS: Sonia Call Structure Activity Remains Prevalent, With OATs Emerging

Oct-02 16:52

Thursday's Europe rates/bond options flow included:

- OATZ5 102p, bought for 2 in 1.25k

- RXX5 127.5/129.5RR, sold the call and receives half a tick in 2k

- RXX5 128/127ps 1x1.5, bought for 15 in 3k

- RXZ5 130.50c, bought for 25.5 and 26 in 11k

- RXX5 125p, bought for 1 in 3k.

- ERM6 98.12/98.25cs vs ERH6 97.93/97.81ps, bought the cs for 2.5 in 5k

- ERZ6 97.93/97.81/97.68/97.56p condor, bought for 1.5 in 3k

- SFIM6 96.30/96.40/96.50 call fly & 96.55/96.65/96.75 call fly paper paid 1.75 on 6K as strips

- SFIM6 96.60/96.80cs, bought for 3.5 in 3k

- 0NH6 96.50/96.70cs, bought for 6 in 3k

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

PIPELINE: Corporate Bond Update: Supply Blizzard Getting Underway

Sep-02 16:51

- Date $MM Issuer (Priced *, Launch #)

- 09/02 $1.75B #Sumitomo Mitsui $750M 3Y SOFR+75, $500M 5Y +65, $500M 11NC10 +115

- 09/02 $1.5B #ING PerpNC7 7.0%

- 09/02 $1B #Norinchukin $500M 5Y +93, $500M 10Y +108

- 09/02 $2B AIIB WNG 5Y SOFR +34a

- 09/02 $Benchmark Merck 2Y +45a, 2Y SOFR, 5Y +70a, 7Y +80a, 10Y +90a, 30Y +100a

- 09/02 $Benchmark CIBC 3NC2 +80a, 3NC2 SOFR, 6NC5 +100a, 6NC5 SOFR

- 09/02 $Benchmark Jersey Central Power +3Y +55, +5Y +70, +10Y +90

- 09/02 $Benchmark MUFG 6NC5 +105a, 11NC10 +120a, PerpNC10 6.875a

- 09/02 $Benchmark Volkswagen Grp of AM 2Y +110a, 3Y +120a, 5Y +135a

- 09/02 $Benchmark Royalty Pharma +5Y +93, 10Y +118, 30Y +128

- 09/02 $Benchmark Kingdom of Saudi Arabia Sukuk 5Y +95a, 10Y +105a

- 09/02 $Benchmark Mitsubishi 3Y +65a, 3Y SOFR, 5Y +75a, 10Y +90a

- 09/02 $Benchmark Cigna 5Y +105a, 7Y +115a, 10Y +125a, 30Y +140a

- 09/02 $Benchmark American Honda 3Y +85a, 3Y SOFR, 5Y +100a

- 09/02 $Benchmark BHP Billiton Finance +10Y +77, 30Y +83

- 09/02 $Benchmark Toyota Cr 3Y +70a, 3Y SOFR, 7Y +95a

- 09/02 $Benchmark Brazil 11/30 tap 5.25%, 30Y +7.55%

- 09/02 $Benchmark Credit Agricole PerpNC10 7.5%a

- 09/02 $Benchmark Nomura 10.75NC5.75 +160a

- 09/02 $Benchmark Jackson National Life 5Y +105a

- 09/02 $Benchmark Ford Motor Cr 5Y +198

- 09/02 $Benchmark Antofagasta 10Y +175a

- 09/02 $Benchmark Ares Capital +5Y +160

- 09/02 $Benchmark HSBC 11NC10 +147

- 09/02 $Benchmark Guardian Life 3Y, 7Y

- 09/02 $Benchmark OKB 5Y SOFR+46a

- 09/02 $500M #Orix Corp 5Y +75

FED: US TSY 52W AUCTION: NON-COMP BIDS $1.043 BLN FROM $50.000 BLN TOTAL

Sep-02 16:45

- US TSY 52W AUCTION: NON-COMP BIDS $1.043 BLN FROM $50.000 BLN TOTAL

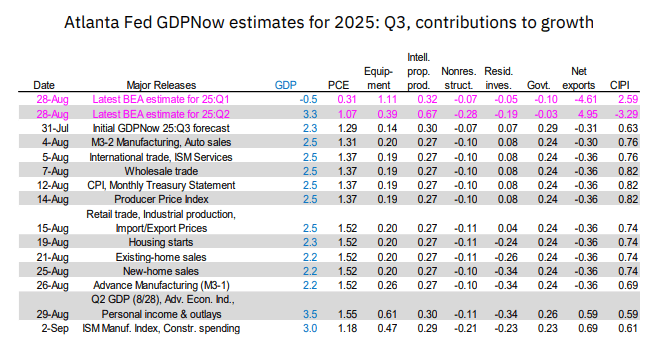

US DATA: GDPNow Trimmed After Recent Strong Uptick

Sep-02 16:28

- The Atlanta Fed’s GDPNow has seen a decent mark lower today on account of ISM manufacturing and construction spending data.

- Real GDP growth is currently seen at 3.0% in Q3 vs 3.5% in Friday’s update taking into account of Q2 national accounts and July PCE.

- PDFP meanwhile is seen running at circa 1.7% annualized in Q3 after two quarters of 1.9% (with that 1.9% in Q2 last week revised firmly higher from the 1.2% in the advance release) and 3.0% averaged in 2024.

- The downward revision to GDP growth tracking was driven by, somewhat surprisingly, consumer spending (-0.37pps) and, less surprisingly after further weak construction spending, non-residential investment (-0.25pps).

- Offsetting this was 0.11pp upward revision to the net exports contribution, leaving it an even more confusing 0.6pps considering the surprise strength in imports seen in July advance trade data. As noted last week, this is likely down to treatment of the industrial supplies series ahead of the full details being known on Sep 4 (when we can more accurately strip out gold).