MNI ASIA MARKETS ANALYSIS: US$ Strength, Stocks Reverse Bid

HIGHLIGHTS

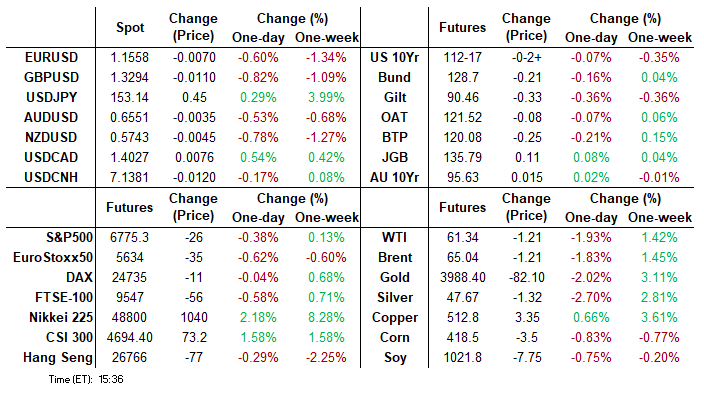

- Treasuries retreated Thursday, initially tracking Bunds in the first half; Tsys held weaker levels after the $22B 30Y auction re-open tailed (912810UM8): 4.734% high yield vs. 4.729% WI.

- Fed Gov Barr calls for a "cautious" approach on adjusting rates and unlike many of his colleagues, doesn't suggest that some further easing toward a more neutral stance is warranted.

- USD strength continues to play out across G10 FX, with EUR/USD and GBP/USD both trading with heavy losses - and taking out key support in the process.

- Stocks remain weaker late Thursday, unwinding gains from the open with the Nasdaq managing to set a new record high of 23,062.62 briefly before reversing course.

US TSYS

MNI US TSYS: Treasuries Decline, Fed Gov Barr Urges Caution on Rate Adjust

- Treasuries look to finish modestly lower after reversing early session gains, mirroring German Bunds in the first half. Currently, the Dec'25 10Y contract trades -2.5 at 112-17 (112-14 low) - initial technical support at 112-13/01 (50-day EMA / 50.0% of Jul 15 - Sep 11 upleg).

- Thursday's weekly Jobless Claims and Wholesale Trade Sales/Inventories suspended due to the Gov shutdown.

- Nevertheless - individual state-by-state estimates should trickle in, which should allow for some rough estimates of the nation-wide figure to emerge from various analysts starting later Thursday and overnight. MNI will provide an estimate for initial (week of Oct 4) and continuing (week of Sep 27) claims by Friday morning.

- Fed Gov Barr calls for a "cautious" approach on adjusting rates and unlike many of his colleagues, doesn't suggest that some further easing toward a more neutral stance is warranted. "If we didn't have any concerns at all about the labor market, we wouldn't need to cut interest rates in that environment" Barr added.

- Tsys held weaker levels after the $22B 30Y auction re-open tailed (912810UM8): 4.734% high yield vs. 4.729% WI; bid-to-cover steady at 2.38x.

- USD strength continues to play out across G10 FX, with EUR/USD and GBP/USD both trading with heavy losses - and taking out key support in the process. This exposed fresh levels in the two pairs at: 1.3282, the Aug 6 low for GBPUSD, and 1.1516, a Fibonacci retracement in EURUSD.

- Looking ahead: Friday's UMichigan preliminary October consumer sentiment survey could prove to be the week's most important single data release.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.12% (-0.02), volume: $2.924T

- Broad General Collateral Rate (BGCR): 4.09% (-0.03), volume: $1.167T

- Tri-Party General Collateral Rate (TCR): 4.09% (-0.03), volume: $1.135T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.10% (+0.01), volume: $76B

- Daily Overnight Bank Funding Rate: 4.10% (+0.01), volume: $156B

FED Reverse Repo Operation

RRP usage slips to new low of $4.496B (lowest level since early April 2021) with 10 counterparties this afternoon vs. $5.231B yesterday. Compares to this year's high usage of $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR and Treasury option flow remains mixed, the former leaning towards low delta calls again even as underlying futures reversed early gains - look to finish near session lows. Curves mixed: 2s10s +1.043 at 54.531, 5s30s -.115 at 99.058. Projected rate cut pricing holding largely steady vs. morning levels (*): Oct'25 holds at -23.7bp, Dec'25 at -44.8bp (-44.5bp), Jan'26 at -54.7bp (-54.6bp), Mar'26 at -65.2bp (-65.1bp).

SOFR Options:

-8,000 SFRZ5 96.00/96.12/96.50/96.62 call condors, 10.5 ref 96.325

+6,000 0QZ5 96.75/96.87/97.00 put trees, 0.0 ref 96.905

+8,000 SFRZ5 96.18/96.25/96.31 put flys, cab ref 96.325

+5,000 0QZ5 97.25/97.50 call spds, 2.75

over 9,300 SFRZ5 96.37 calls largely vs. to 96.43 calls on ratio

+59,000 SFRZ5 96.68/96.81 call spds, 0.25-0.5

Block, 2,500 0QF6 96.87/97.00/97.12/97.37 broken call condors, 0.5

+5,000 SFRU6 96.75/0QU6 96.62 put spds, 0.5

+2,000 SFRZ5 96.12/96.18/96.25/96.31 put condors, 1.0 ref 96.32

+2,000 SFRZ5 96.25/96.37/96.50/96.62 call condors, 6.25 ref 96.32

+4,000 SFRZ5 96.50/96.62 call spds, 1.0 ref 96.315

+2,000 0QX5 96.31 calls, 2.5 ref 96.935

Treasury Options:

2,000 TYX5 112.75 calls, 18 ref 112-16.5

3,000 FVX5 108.25 puts ref 109-05.25

1,500 TYX5 112.5 puts, 25 ref 112-16.5, total volume over 11,500

over 7,700 TYX5 113 calls, 14 ref 112-17.5

5,000 FVX5 108.5/109.5 strangles, 13 ref 109-05.25

over +10,900 TYX5 111.75 puts, 7 ref 112-18.5

over 5,200 TYZ5 112.5 puts, 43-44

+2,000 wk3 TY 112.25/112.5/112.75/113 call condors, 6.0 vs. 112-21-0.05%

4,350 TUZ5 104/104.25 2x1 put spds, 1.0 vs. 104-06/0.10%

MNI BONDS: EGBs-GILTS CASH CLOSE: OATs Weaker, But Outperform Peers

European curves bear steepened Thursday.

- Periphery/semi-core EGB spreads widened modestly on a session that was only light on data and macro developments, largely in a late risk-off move late as equities weakened.

- OATs outperformed peers however after the Government announced post-cash close Wednesday that President Macron will announce a new prime minister Friday, potentially averting the need to hold snap elections.

- BoE's Mann pointed to another vote in favour of maintaining rather than cutting Bank Rate.

- The ECB's September meeting accounts broadly echoed President Lagarde's view that policy is in a good place, citing no immediate pressure to change rates.

- As noted, it was a limited session for data (amid the US gov't shutdown). The German trade surplus outperformed expectations in August.

- Both the UK and German curves bear steepened, with Gilts underperforming.

- Apart from the French PM announcement which is the most anticipated event of the day, Friday's calendar includes Italian industrial production data and an appearance by ECB's Escriva. S&P is due to rate Italy after Friday's cash close.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.8bps at 1.997%, 5-Yr is up 2.4bps at 2.295%, 10-Yr is up 2.4bps at 2.703%, and 30-Yr is up 1.5bps at 3.279%.

- UK: The 2-Yr yield is up 0.9bps at 4.004%, 5-Yr is up 2.7bps at 4.176%, 10-Yr is up 3.6bps at 4.745%, and 30-Yr is up 3.6bps at 5.546%.

- Italian BTP spread up 0.8bps at 80.5bps / Spanish bond spread up 0.2bps at 54.1bps

MNI OPTIONS: Upside Theme Continues In Both Sonia And Euribor

Thursday's Europe rates/bond options flow included:

- ERM6 98.25/98.37 call spread paper paid 2.25 on 10K

- ERM6 98.4375/98.50/98.5625c fly, bought for 0.25 in 2.5k.

- SFIG6 96.60/70 call spread paper paid 0.75 on 10K

- SFIH6 96.35/96.50cs, bought for 3.5 in 4k (Adding to the 16k bought Wednesday)

- SFIZ6 96.05p vs SFIM6 96.00p with SFIZ6 97.00c, sold the Dec put at 0.75 in 3k

MNI FOREX: USD Recovery Picks Up, Despite JPY Bounce

- USD strength continues to play out across G10 FX, with EUR/USD and GBP/USD both trading with heavy losses - and taking out key support in the process. This exposed fresh levels in the two pairs at: 1.3282, the Aug 6 low for GBPUSD, and 1.1516, a Fibonacci retracement in EURUSD.

- The dollar strength persists across the US government shutdown - but is not a reflection of increased expectations of economic resilience, but may be more a factor of market uncertainty as well as increasing risk abroad - particularly political risk in France and Japan.

- The USD has fast reversed the weakness posted off the early August high - taking out 99.304, the 76.4% retracement for the Aug - Sep downleg in the process. Markets still firmly expect a further Fed rate cut at the next meeting, even without the security of the latest NFP print and as next week's inflation print is likely delayed. Instead, markets remain on watch for private sector labour market and inflation measures.

- JPY underwent a spell of volatility as Takaichi spelt out that her government will not pursue JPY weakness excessively - a comment that helped trigger a sharp - albeit brief - spell of JPY strength. Volumes similarly spiked, with JPY futures trading a cash equivalent of $2bln in just two minutes - easily the best volumes of the week.

- Scandi currencies underperformed. SEK and NOK were the poorest performers on the day, with the looming Verisure IPO a potential trigger - sell-side estimates have gauged as much as €2bln in EURSEK demand set to cross as the IPO settles on Friday.

FX OPTIONS: Expiries for Oct10 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1450(E1.1bln), $1.1500-20(E2.5bln), $1.1570-75(E780mln), $1.1600(E1.9bln), $1.1625-30(E1.1bln), $1.1650(E1.9bln), $1.1670-75(E695mln), $1.1700(E1.9bln), $1.1720-25(E907mln), $1.1740-50(E2.5bln), $1.1780-00(E2.8bln

- USD/JPY: Y152.30-50($951mln)

- GBP/USD: $1.3400(Gbp942mln), $1.3470(Gbp638mln)

- AUD/USD: $0.6545(A$658mln)

- USD/CNY: Cny7.1034($600mln)

MNI US STOCKS: Late Equities Roundup: Materials, Industrials, Energy Underperforming

- Stocks remain weaker late Thursday, unwinding gains from the open with the Nasdaq managing to set a new record high of 23,062.62 briefly before reversing course. Currently, the DJIA is down 276.89 points (-0.59%) at 46,324.14, S&P E-Minis down 34.75 points (-0.51%) at 6,767, Nasdaq down 96.7 points (-0.4%) at 22,948.95.

- A mix of Materials (partially tied to a reversal in Gold after setting record high of 4042.03 yesterday), Industrials and Energy sector shares underperformed in the second half:

- Newmont Corp -4.26%, Mosaic -3.42%, Dow Inc -3.19% and LyondellBasell Industries -2.69%.

- Stanley Black & Decker -4.25%, Boeing -3.29%, Uber Technologies -3.16% and Ingersoll Rand -3.04%.

- Targa Resources -3.82%, Coterra Energy -3.61%, APA -3.25% and Diamondback Energy -3.19%.

- On the positive side, Consumer Staples sector shares added to midweek gains: Kenvue +3.67%, PepsiCo +3.34%, Costco Wholesale +2.13% and Lamb Weston Holdings +0.70%.

- Health Care sector shares followed with pharmaceuticals outperforming: IQVIA Holdings +1.43%, Merck & Co +1.19%, Regeneron Pharmaceuticals +0.73% and Boston Scientific +0.71%.

MNI EQUITY TECHS: E-MINI S&P: (Z5) Fresh Cycle High

- RES 4: 6850.87 1.618 proj of the Aug 1 - 15 - 20 price swing

- RES 3: 6831.38 2.500 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 2: 6819.25 1.500 proj of the Aug 1 - 15 - 20 price swing

- RES 1: 6812.29 2.382 proj of the Aug 20 - 28 - Sep 2 price swing

- PRICE: 6786 @ 1440 ET Oct 9

- SUP 1: 6710.17 20-day EMA

- SUP 2: 6680.00 Low Oct 1

- SUP 3: 6624.25 Low Sep 25

- SUP 4: 6591.35 50-day EMA

The trend condition in S&P E-Minis is unchanged and the direction remains up. Fresh cycle highs this week confirm a continuation of the uptrend and maintain the positive price sequence of higher highs and higher lows. Sights are on 6812.29 and 6819.25, Fibonacci projection points. Initial support to watch is at the 20-day EMA, at 6710.17. It has recently been pierced, a clear break of it would signal scope for a deeper pullback.

MNI COMMODITIES: Gold, Crude Pull Back As Geopolitical Risks Ease

- The bid in the US dollar, amid news that an agreement has been reached to end the war between Israel and Hamas, has weighed on gold today, which has fallen back below $4,000/oz after retesting yesterday’s all-time high.

- Spot is currently down by 2.0% at $3,961/oz.

- The agreement will allow the release of Israeli hostages and Palestinian prisoners possibly as soon as the weekend, aid into Gaza, withdrawal of the IDF to a particular line and the end of Hamas in Gaza.

- Despite the pullback in gold, a bull cycle remains in play and this week’s breach of the $4,000 handle reinforces the uptrend. Sights are on $4,074.54, a Fibonacci projection, while support to watch is at $3,816.4, the 20-day EMA.

- Meanwhile, WTI crude is also lower as the news of the ceasefire agreement reduces geopolitical risk in the Middle East. This comes after prices have risen so far this week following a more cautious OPEC November output increase and US product drawdowns.

- WTI Nov 25 is down by 1.8% at $61.4/bbl.

- A bearish theme in WTI futures remains intact, with sights on initial support at $60.40, the Oct 2 low. Clearance of this level would pave the way for an extension towards $57.50, the May 30 low.

- Initial firm resistance is at $66.42, the Sep 29 high.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 10/10/2025 | 0600/0800 | *** | CPI Norway | |

| 10/10/2025 | 0600/0800 | ** | Private Sector Production m/m | |

| 10/10/2025 | 0900/1100 | * | Industrial Production | |

| 10/10/2025 | - | ECB de Guindos at ECOFIN Meeting | ||

| 10/10/2025 | 1230/0830 | *** | Labour Force Survey | |

| 10/10/2025 | 1230/0830 | *** | Labour Force Survey | |

| 10/10/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 10/10/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 10/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 10/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 10/10/2025 | 1700/1300 | St Louis Fed's Alberto Musalem | ||

| 10/10/2025 | 1800/1400 | ** | Treasury Budget |