US TSYS: Treasuries Decline, Fed Gov Barr Urges Caution on Rate Adjust

Oct-09 2025 19:29

- Treasuries look to finish modestly lower after reversing early session gains, mirroring German Bunds in the first half. Currently, the Dec'25 10Y contract trades -2.5 at 112-17 (112-14 low) - initial technical support at 112-13/01 (50-day EMA / 50.0% of Jul 15 - Sep 11 upleg).

- Thursday's weekly Jobless Claims and Wholesale Trade Sales/Inventories suspended due to the Gov shutdown.

- Nevertheless - individual state-by-state estimates should trickle in, which should allow for some rough estimates of the nation-wide figure to emerge from various analysts starting later Thursday and overnight. MNI will provide an estimate for initial (week of Oct 4) and continuing (week of Sep 27) claims by Friday morning.

- Fed Gov Barr calls for a "cautious" approach on adjusting rates and unlike many of his colleagues, doesn't suggest that some further easing toward a more neutral stance is warranted. "If we didn't have any concerns at all about the labor market, we wouldn't need to cut interest rates in that environment" Barr added.

- Tsys held weaker levels after the $22B 30Y auction re-open tailed (912810UM8): 4.734% high yield vs. 4.729% WI; bid-to-cover steady at 2.38x.

- USD strength continues to play out across G10 FX, with EUR/USD and GBP/USD both trading with heavy losses - and taking out key support in the process. This exposed fresh levels in the two pairs at: 1.3282, the Aug 6 low for GBPUSD, and 1.1516, a Fibonacci retracement in EURUSD.

- Looking ahead: Friday's UMichigan preliminary October consumer sentiment survey could prove to be the week's most important single data release.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

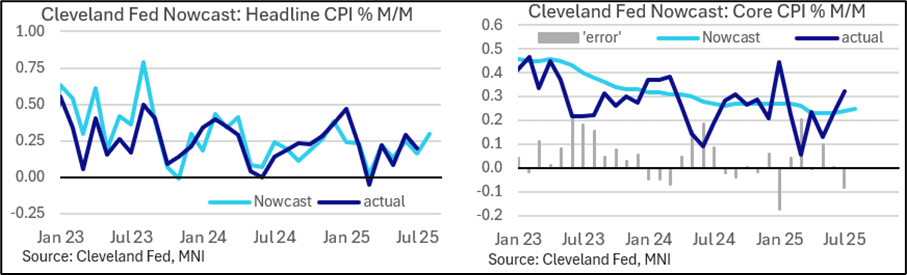

US INFLATION: Cleveland Fed Nowcast CPI Tracker Points To August Pickup

Sep-09 2025 19:28

The Cleveland Fed nowcast has headline CPI at 0.30% M/M and core CPI at 0.25% M/M in August. That headline estimate is the nowcast’s highest of the year (the only one higher in the last 15 months was December 2024’s 0.38%) and comes after two consecutive 0.04pp underestimates of the actual figure (July: 0.16% vs actual 0.20%).

- The core tracker meanwhile is a the highest since March, after undershooting the actual in July (0.24% vs 0.32% actual, biggest undershoot since January) after an accurate reading in June (0.23%).

- MNI median unrounded est for core is 0.32% M/M, and for headline 0.36%

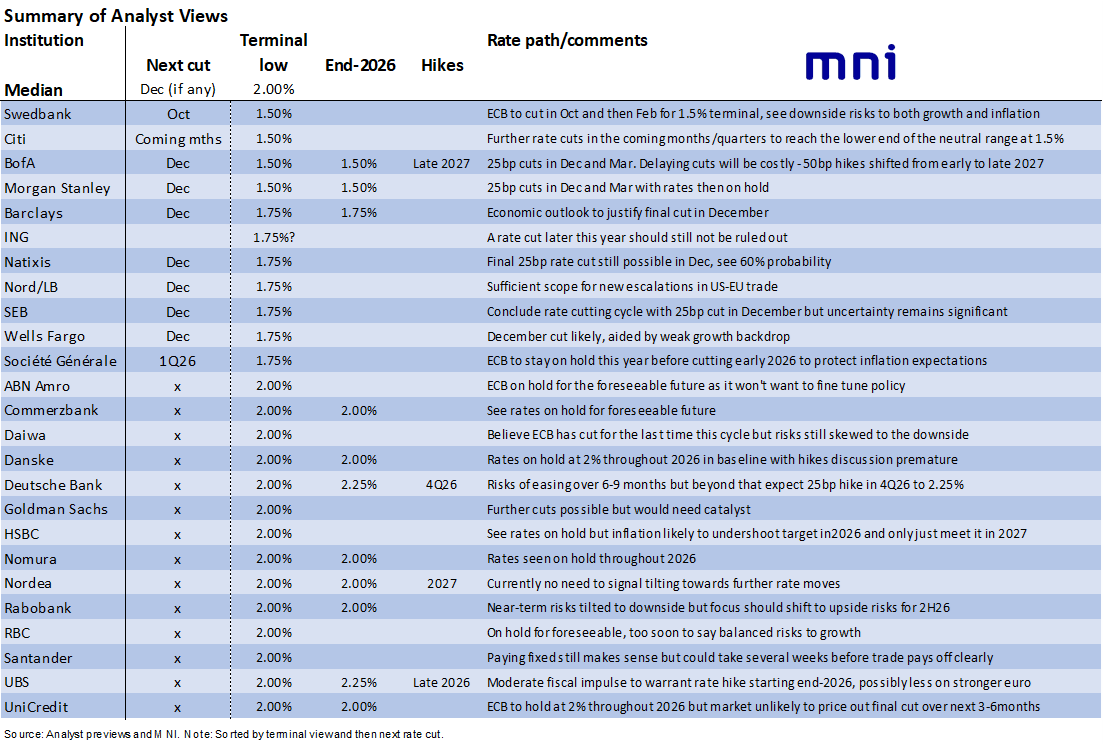

ECB: Median Analyst Sees No Further Cuts, But With Clear Dovish Skew Remaining

Sep-09 2025 19:26

- The median of 25 analysts reviewed below sees no more rate cuts ahead, with the deposit rate at 2.00%.

- There is still a dovish skew to that, with 7 looking for one cut to 1.75% and 4 looking for two cuts to 1.50%, but it’s nevertheless a sizeable change from ahead of the July meeting when there was a clearcut consensus for a terminal 1.75% rate.

- Where analysts do expect a cut, December looks most likely, on the assumption that it could take a while for softer conditions to materialise and presumably with the added perk of being a projections meeting.

- Explicit rate hike expectations are starting to feature a little more prominently but remain firmly in the minority, with the earliest seen by Deutsche Bank and UBS in late 2026.

US TSYS: Late SOFR/Treasury Options Leaning Toward Calls, Rate Cuts Cool

Sep-09 2025 19:08

Option desks reported mixed SOFR and Treasury flow Tuesday, leaning toward calls even as underlying futures look to finish lower/near lows. Projected rate cuts recede slightly from pre-open (*) levels: Sep'25 at -27.2bp (-27bp), Oct'25 at -45.9bp (-47.3bp), Dec'25 at -67.9bp (-69.2bp), Jan'26 at -79.9bp (-82.3bp).

- SOFR Options:

- -4,000 SFRH7 96.00/98.00 risk rev w/ SFRM7 96.12/98.12 risk rev, both call over 1 total

- 3,000 96.25/96.37/96.50/96.62 call condors ref 96.36

- Block, 6,500 SFRZ5 96.62/96.75 call spds 1.75

- +2,500 SFRM6/SFRU6 97.50/98.25 call spd strip, 18.5

- 2,000 SFRZ5 96.37/96.43/96.50 call flys ref 96.355

- 2,000 SFRZ5 96.25/96.37 call spds ref 96.38

- 2,850 SFRU5 96.00/96.06/96.18/96.25 call condors, ref 95.985

- +5,000 SFRU5 96.00/96.12 call spds, 1.5

- +2,500 SFRZ5 95.81/95.93 put spds, 0.5 vs. 96.35/0.05%

- +5,000 SFRZ5 96.50/96.62/96.75/96.87 call condors, 1.5

- +10,000 SFRU5 95.93/96.00/96.06 call flys, 2.75

- 2,000 SFRU5 95.87/96.00/96.12 iron flys, 4.0 ref 95.99

- Block, +5,000 SFRU5 95.87/95.93/96.00 call flys, 2

- Block, +2,500 SFRU5 96.00/96.12 call spds, 1.25

- Block/screen, +4,000 SFRZ5 96.50/96.62/96.75/96.87 call condors, 1.5

- +6,000 SFRZ5 96.00/96.12 put spds, 1.75

- -2,000 0QU5 97.00/97.50 call spd vs. 2QU5 97.00/97.37 call spds, 2.0 net

- +5,000 SFRU5 96.00 calls, 1.75

- Treasury Options:

- 2,400 TUV5 104.75/105 1x2 call spds ref 104-14.25

- 2,400 FVZ5 110 calls ref 109-29.25

- 2,500 FVV5 109.75 puts, 17.5 ref 109-28.25

- 5,000 TUV5 104.25/104.5 call spds ref 104-14.88

- 5,000 TYV5 113.5/114 call spds ref 113-13

- +2,000 TYV5 111.75/112.75 put spds 13 vs. 113-08.5/0.08%

- +1,500 TYV 112/113 put spds, 15 vs. 113-16.5/0.23%

- +1,500 TUH6 104.62/105.25 call spds, 13.5 vs. 104-14.75/0.20%