MNI ASIA MARKETS ANALYSIS: US$ Bounce as Fed Chair List Grows

HIGHLIGHTS

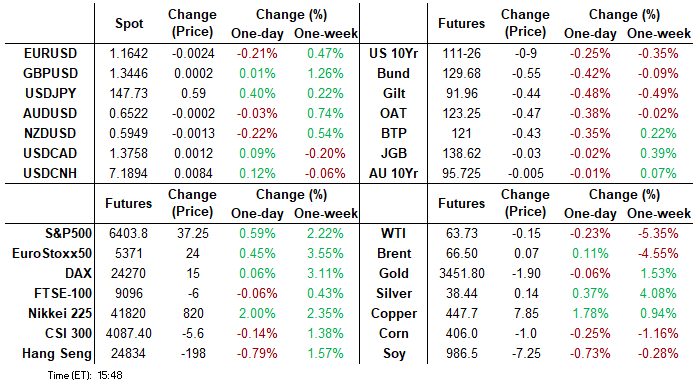

- Treasuries look to finish weaker Friday - near late week lows while yields climb past Wednesday's knee jerk high of 4.2789% to 4.2868%. Futures appeared to follow German Bunds lead lower in the first half.

- No data, but St Louis Fed Pres Musalem (2025 FOMC voter, hawk) said in a Q&A that he supported the July decision to hold rates as the FOMC is missing on its inflation target but not its employment target.

- The greenback rose against all others on Friday - gaining late after WSJ reported ex-St Louis Fed Pres Bullard and ex-Bush adviser Marc Sumerlin have been added to the list.

- Slow start to next week's calendar, focus on Tuesday's CPI inflation data for July. Core CPI meanwhile is seen at 0.32% M/M (cons 0.3)

US TSYS

MNI US TSYS: Extending Late Lows, Yields Surpass Midweek Kneejerk High

- Treasuries look to finish weaker Friday - near late week lows while yields climb past Wednesday's knee jerk high of 4.2789% to 4.2868%. Futures appeared to follow German Bunds lead lower in the first half.

- Tsy Sep'25 10Y futures trade -9.5 at 111-25.5 after the bell - first technical support lies at 110-19+, the Jul 24 low, key support is 110-08+, the Jul 14 and 16 low.

- Curves mixed, short end steeper (2s10s +1.046 at 52.652 while projected rate cuts consolidated slightly from morning levels(*): Dec'25 at -58.3bp (-59.4bp).

- No data, but St Louis Fed Pres Musalem (2025 FOMC voter, hawk) said in a Q&A that he supported the July decision to hold rates as the FOMC is missing on its inflation target but not its employment target.

- The greenback rose against all others on Friday - gaining late (BBDXY +1.16 at 1204.82) after The Wall Street Journal reported that ex-St Louis Fed President James Bullard and ex-George W Bush adviser Marc Sumerlin have been added to the list of possible Fed Chair nominees (previously named Waller, Hassett, and Warsh also on the list).

- Slow start to next week's calendar, focus on Tuesday's CPI inflation data for July. Core CPI meanwhile is seen at 0.32% M/M (cons 0.3).

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.35% (+0.01), volume: $2.855T

- Broad General Collateral Rate (BGCR): 4.33% (+0.01), volume: $1.154T

- Tri-Party General Collateral Rate (TCR): 4.33% (+0.01), volume: $1.130T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $108B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $254B

FED Reverse Repo Operation

RRP usage inches up to $80.303B this afternoon from $77.961B yesterday (lowest level since mid-April when usage fell to the mid-50s), total number of counterparties at 21. Lowest usage of the year at $54.772B on Wednesday, April 16 -- in turn the lowest level since April 2021 - compares to July 1: $460.731B highest usage since December 31.

US SOFR/TREASURY OPTION SUMMARY

With few exceptions, upside calls continued to drive SOFR & Treasury options volumes Friday. Underlying futures moderately weaker - at/near late session lows, curves mixed (2s10s -.204 at 51.402, 5s30s +.243 at 103.537). Projected rate cut pricing has eased slightly vs. morning (*) levels: Sep'25 at -22.6bp (-22.8bp), Oct'25 at -38.4bp (-38.9bp), Dec'25 at -58.3bp (-59.4bp), Jan'26 at -68.9bp (-70.9bp).

SOFR Options:

+10,000 SFRV5 96.00/96.18 2x1 put spds, 3.0 net ref 96.245

+4,000 SFRM6 96.12/96.50 put spd 8.0 over 97.25/97.62 call spd vs. 96.665/0.20%

-6,000 SFRQ5 95.87/96.00 put spds, 6.5

+10,000 SFRX5 95.68/95.75 put spds, 0.5

+5,000 SFRZ5 96.25/96.37/96.50 call flys, 1.5 ref 96.25

-2,500 SFRH6 95.62 puts, 1.0 ref 96.465

+8,000 0QU5 97.25/97.50 call spds 1.75

-3,000 SFRU5 95.68/95.81 put spds, 2.75

1,600 0QZ5 96.75/97.00/97.50/97.75 call condors ref 96.91

+15,000 SFRU5 96.12/96.25 call spds, 1.5 ref 95.93 (ongoing buyer)

over +7,300 SFRZ5 99.00 calls, .25

-3,000 SFRZ5 96.25/96.37/96.50/96.25 call condors, 3 ref 96.25

3,000 SFRQ5 95.87/95.93 call spds ref 95.93

Block, -6,000 SFRQ5 95.81/95.93 call spds, 8.5

Block, -5,000 SFRQ5 95.68/95.81/95.93 put flys, 3.25

Treasury Options:

35,000 TYU5/TYZ5 115 call spds, 24 net, Dec over

-1,500 TYV5 112 straddles, 146

-3,000 TYU5 112 calls, 28

8,500 wk2 TY 112 put (exp today) vs. wk3 TY 112.5 calls (exp 8/15), 8 net/call over

over 7,500 TYU5 113.5 calls, 5 last

-1,000 FVX5 109 straddles, 129 ref 109-01.75

2,700 TYU5 113.5/TYV5 115.5 call spds, covered 3 net

1,200 TUU5 103.62 puts, 1.5 ref 103-28.25

+1,000 wk3 TY 112.5/113/113.25 broken call flys, 3.5

-1,000 TYX5 108.5/110/113.5/115 iron condor, 32

MNI BONDS: EGBs-GILTS CASH CLOSE: Afternoon Weakness Cements Weekly Bear Steepening

European curves bear steepened to close the week.

- Bonds leaned a little weaker in early trade, in part due to spill-over from a weak long-end US Treasury auction after the European cash close Thursday.

- Then EGBs/Gilts turned lower in early afternoon trade with no clear catalyst, though the move was amid fairly thin volumes and weekly lows were not pierced.

- Comments from BoE chief economist Pill were hawkish, but had little reaction as it's known he dissented against Thursday's rate cut.

- There was a modest bounce in Bunds alongside a Bloomberg headline reporting that the US and Russia are "planning Ukraine deal cementing Russian gains", but this did little to mitigate the earlier sell-off.

- Bunds underperformed Gilts across most of the curve. Periphery/semi-core EGB spreads tightened modestly as equities rallied going into the weekend.

- Curves bear flattened for the week: Germany (2Y +2.7bp, 10Y +1.1bp) outperformed the UK (2Y +10.6bp, 10Y +7.3bp) largely on account of the hawkish-leaning BOE decision.

- The early highlight next week is the UK labour market data for June/July.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 3.7bps at 1.956%, 5-Yr is up 5.7bps at 2.283%, 10-Yr is up 6bps at 2.69%, and 30-Yr is up 6.8bps at 3.206%.

- UK: The 2-Yr yield is up 2.2bps at 3.899%, 5-Yr is up 3.3bps at 4.037%, 10-Yr is up 5.4bps at 4.601%, and 30-Yr is up 7.7bps at 5.428%.

- Italian BTP spread down 0.4bps at 78.9bps / Spanish down 0.4bps at 56.7bps

MNI EGB OPTIONS: Little More Lean Toward Put Structures Than Earlier In The Week

Friday's Europe rates/bond options flow included:

- DUV5 107.20/107.10/106.90 broken put ladder, bought for 1 and 1.5 in 7.6k

- RXU5 (15th Aug) 130.00/129.50ps vs 130.5/131.00cs, bought the ps for 5 in 2k

- ERV5 98.1875/98.3125/98.375/98.5625c condor, sold at 1.25 in 4k

- ERZ5 98.25/98.1875 put spread 5K given at 4.5

- SFIZ5 96.1096.25/96.40/96.55c condor, sold at 6.75 in 7k

- SFIZ5 96.20/96.15/96.10/96.00broken put condor, bought for 0.75 in 3k

- SFIH6 96.50/97.00cs 1x1.5, bought for 7 in 2k

- SFIM6 96.75/97.25/97.75c fly, bought for 5.5 in 5k

MNI FOREX: USD/JPY Rallies, But Consolidation Phase Still in Play

- The greenback rose against all others on Friday - gaining late (BBDXY +1.16 at 1204.82) after The Wall Street Journal reported that ex-St Louis Fed President James Bullard and ex-George W Bush adviser Marc Sumerlin have been added to the list of possible Fed Chair nominees (previously named Waller, Hassett, and Warsh also on the list).

- JPY traded poorly on a phase of selling pressure through the European morning. Speculation continues to mount over the future of the LDP leadership. Speaking today, Ishiba noted he is not intending to change the cabinet lineup for now, but has vowed to stay on in his role despite party pressure to accelerate succession. Conviction in the weaker is low, however, with volumes holding below the average.

- While JPY traded weaker, USD/JPY has held inside a consolidation pattern for much of the week, holding the bulk of the NFP losses. This has allowed a previously overbought condition to unwind, and keeps the downside argument in focus. The recent break and close below 147.57, the 20-day EMA, is a concern. A clear break of this support zone would undermine the recent bull theme. A break of last week’s 150.92 high would resume the uptrend.

- Canadian jobs data came in noticeably weaker than forecast, with the country shedding over 40k jobs in July and over 50k full-time positions. The unemployment rate also ticked higher on a non-rounded basis, helping USD/CAD keep well off the mid-week lows. The 100-dma comes in as first resistance here, crossing at 1.3829.

- Headlines just ahead of the UK close showed US and Russian negotiators reportedly working on mutually-agreeable ceasefire conditions. The terms included a freezing of current battlelines and a withdrawal of troops from regions occupied by opposition forces - if realised, such an agreement would be a major boon to Putin, whose forces have proved unable to wrest control of the regions by force over the course of the past three and a half years of war.

- Risk rallied, with European equities putting in a firm bounce on the report. Rallies were limited however, as there remain significant impediments to such a deal. It is unclear whether Ukraine will be invited to participate in direct talks with Putin, and the Zelenskyy administration could immediately reject such an offer (albeit risking a backlash from a White House impatient for any form of peace to be agreed).

- The coming week's highlights include UK jobs data (seen confirming the slowdown in the UK labour market over the past few quarters), the RBA rate decision (expected to undergo a 25bps cut to 3.60%) and a potential face-to-face meeting held between the US and Russian Presidents.

MNI OPTIONS: Expiries for Aug11 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1550(E1.2bln), $1.1600-05(E1.1bln), $1.1650-60(E940mln), $1.1690-00(E1.5bln), $1.1750(E1.0bln)

- USD/JPY: Y147.00($571mln)

- GBP/USD: $1.3331-45(Gbp552mln)

- NZD/USD: $0.5920-30(N$1.2bln)

- USD/CAD: C$1.3605($591mln)

MNI US STOCKS: Late Equities Roundup: Nasdaq Marks New Record High

- Stocks continue to extend gains late Friday, the tech-heavy Nasdaq marking new record high of 21,464.53 - surpassing prior record high of 21,457.48 from July 31. Currently, the DJIA trades up 220.3 points (0.5%) at 44189.98, S&P E-Minis up 46.75 points (0.73%) at 6413.5, Nasdaq up 203 points (1%) at 21446.57.

- A mix of Information Technology, Pharmaceuticals, Communication Services and Financial sector shares continued to lead the late week rally: Gen Digital +9.39%, Micron Technology +5.80%, Apple +4.21%, Skyworks Solutions +3.72%; Gilead Sciences +8.41%, Elevance Health +3.93%, Expedia Group +3.90%, MetLife +3.73% and Humana +3.04%; Prudential Financial +2.84%, Bank of America +2.83%.

- Leading decliners: Despite reporting more-or-less in-line earnings Trade Desk Inc fell -37.06% (trading desks suggested the departure of CFO Schenkein for the sell-off), GoDaddy -11.09%, Paramount Skydance -9.50%, Akamai Technologies -5.93%, Warner Bros Discovery -5.69%, DoorDash -4.11%, Edison International -3.31% and Uber Technologies -3.27%.

- Note, nearly 80% of companies have reported earnings in the latest cycle, while some Cisco and Applied Materials announce next week, focus will be on Nvidia's earnings expected August 28.

MNI EQUITY TECHS: E-MINI S&P: (U5) Corrective Pullback Extends

- RES 4: 6523.63 1.764 proj of the May 23 - Jun 11 - 23 price swing

- RES 3: 6500.00 Round number resistance

- RES 2: 6477.31 1.618 proj of the May 23 - Jun 11 - 23 price swing

- RES 1: 6468.50 High Jul 31 and the bull trigger

- PRICE: 6415.00 @ 1515 ET Aug 8

- SUP 1: 6244.36 2.0% 10-dma Envelope

- SUP 2: 6239.50 Low Aug 1

- SUP 3: 6213.75 50% retracement of Jun - Aug Upleg

- SUP 4: 6203.65 50-day EMA

Equities sold off sharply Friday on the back of the soft NFP print - pushing prices through mid-July lows in the process. Since that spell of weakness, price has traded either side of support at the 20-day EMA, at 6325.25, signaling scope for a deeper retracement toward the 50-day EMA at 6203.65. Clearance of this average is required to signal a stronger reversal. The primary trend remains up, leaving key short-term resistance and the bull trigger at 6468.50, the Jul 31 high.

COMMODITIES

MNI AMERICAS OIL: WTI crude prices ended near unchanged today

WTI crude prices ended near unchanged today amid late short covering after having traded lower on some signs of progress towards a peace agreement in Ukraine and are nonetheless on track for a net weekly decline with the market focused on the risk of oversupply amid rising OPEC+ output and higher US tariffs on India.

- Washington and Moscow are aiming to reach a deal that would lock in Russia’s territorial gains in Ukraine, according to Bloomberg, with the report slightly easing supply risks amid US threats of further Russian sanctions. A Trump-Putin meeting is tentatively being planned for the end of next week, according to Fox News reporter Jacqui Heinrich.

- This week Trump announced a doubling of tariffs on Indian imports to 50% as a penalty for the ongoing purchase of Russian oil, prompting local state-owned oil refiners to pull back from purchases and look elsewhere.

- WTI Sep futures were down 0% at $63.88

- WTI Oct futures were down 0.1% at $62.97

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 11/08/2025 | 0600/0800 | *** | CPI Norway | |

| 11/08/2025 | 0800/1000 | *** | HICP (f) | |

| 11/08/2025 | - | *** | Money Supply | |

| 11/08/2025 | - | *** | New Loans | |

| 11/08/2025 | - | *** | Social Financing | |

| 11/08/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 11/08/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 12/08/2025 | 2301/0001 | * | BRC-KPMG Shop Sales Monitor | |

| 12/08/2025 | 0430/1430 | *** | RBA Rate Decision |