MNI ASIA MARKETS ANALYSIS: Tsys Retreat, Reevaluating Soft CPI

HIGHLIGHTS

- Treasuries look to finish lower, curves mildly mixed Friday, intermediate rates below Thursday's pre-CPI inflation data levels as markets continued to question the delayed/abbreviated Oct/Nov report.

- Consumer sentiment ended the year on a down note, with the final UMichigan survey for December confirming the weakest current conditions reading in series history.

- A Japanese bond selloff overnight after the BOJ's rate hike set a negative tone that was picked up by long-end EGBs in early trade, with the broader German bear steepening move resuming following Thursday's ECB decision.

US TSYS

MNI US TSYS: Tsys Fully Reject Thursday's CPI-Tied Rally, Bund Decline Adds to Move

- Treasuries look to finish weaker Friday, early impetus: Japanese bond selloff overnight after the BOJ's rate hike set a negative tone that was picked up by long-end EGBs in early trade, with the broader German bear steepening move following Thursday's ECB decision.

- Treasuries followed Bunds lead in early trade, extending lows as rates fall back towards yesterday's pre-data levels as markets continued to question the delayed/abbreviated Oct/Nov report.

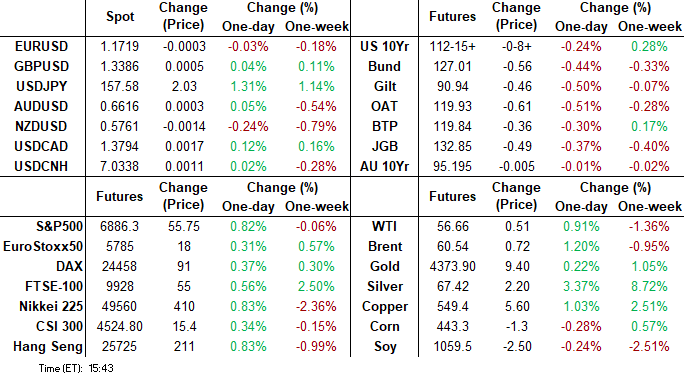

- Currently, TYH6 trades -8 at 112-16 vs. 112-14.5 low, 10Y yield +.0274 at 4.1490%, a deeper pullback would cancel a bull theme and instead refocus on attention on 111-29, the Dec 10 low and a key short-term support.

- NY Fed President Williams tells CNBC in an interview Friday that the this week's soft CPI print as well as the tickup in the unemployment rate were distorted by technical factors. As such he says that the latest data doesn't change his view of the outlook: “I don’t personally have a sense of urgency to need to act further on monetary policy right now because I think the cuts we’ve made have positioned us really well."

- Consumer sentiment ended the year on a down note, with the final U-Michigan survey for December confirming the weakest current conditions reading in series history. Overall Consumer Sentiment was revised down slightly to 52.9 from 53.3 (51.0 Nov), with Expectations also revised down 0.4 points to 54.6 (51.0 Nov), while Current Conditions at the record low 50.4 (50.7 prelim, 51.1 Nov).

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.66% (-0.03), volume: $3.273T

- Broad General Collateral Rate (BGCR): 3.63% (-0.03), volume: $1.325T

- Tri-Party General Collateral Rate (TCR): 3.63% (-0.03), volume: $1.300T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.64% (+0.00), volume: $88B

- Daily Overnight Bank Funding Rate: 3.64% (+0.00), volume: $171B

FED Reverse Repo Operation:

RRP usage retreats to $3.047B with 12 counterparties this afternoon vs. Thursday's $11.708B. Compares to last Thursday's $0.838B (lowest level since mid-March 2021); this years highest excess liquidity measure: $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

Mixed and largely two-way SOFR/Treasury option flow Friday. Highlight trade was continued interest in buying large clips of Mar'26 10Y low delta Treasury calls. Underlying futures weaker - back to yesterday's pre-data lows as markets question the CPI inflation data. Projected rate cut pricing continues to retreat vs. late Thursday levels (*): Jan'26 at -5.5bp (-6.6bp), Mar'26 at -14.9bp (-16.8bp), Apr'26 at -22bp (-23.6bp), Jun'26 at -35.6bp (-37.6bp).

SOFR Options:

+5,000 SFRH6 96.00 puts, cab ref 96.49

+2,000 0QF6 96.87/96.93 strangles, 12.5 ref 96.905

+2,000 2QF6 96.50 puts, 1.5 vs. 96.695/0.10%

-20,000 SFRH6 96.62/96.75 call spds, 1.25

+15,000 SFRH6 96.18/96.31 put spds, 0.25 ref 96.49

Block/screen, 10,000 SFRM6 97.87/SFRU6 98.62 call strip, 4.0

-5,000 0QU6 96.75/97.25/97.50/98.00 call condors, 13.25

+2,500 0QH6 96.62/96.87 2x1 put spds, 5.0 vs. 96.83/0.05%

+2,000 SFRF6/SFRG6 96.56/96.62/96.68 call fly strip, 1.0

+2,000 SFRF6 96.25/96.31/96.37/96.43 call condors

+1,000 SFRH6 96.62/96.75/96.87/97.00 call condors ref 96.50/0.10%

+2,000 SFRH6 96.18/96.31 put spds

Treasury Options:

12,500 TYH6 111 puts, 17 ref 112-16.5

over 6,000 TYF6 114.5 calls ref 112-17.5

10,000 TUF6 104.37/104.5 strangles ref 104-12.12

2,000 USH6 120 calls, ref 115-09

3,000 USF6 110/113 put spds ref 115-08

3,000 USF6 117/122 call spds ref 115-08

over +53,600 TYH6 113.5 calls, 30 vs. 112-18.5/0.30%

1,000 TYH6 113/113.5/114/114.5 call condors ref 112-16.5

+2,000 TYG6 112.5 straddles, 106

+4,000 Mon wkly 10Y 112/112.25 put spds, 4 vs. 112-15/0.14%

+2,250 TYF6 111.75/114 call over risk reversals, 0.0

+3,250 TYF6 112.5 puts, 10 vs. 112-18 to -18.5/0.35%

over 12,700 TYF6 113 calls, 3 last - part tied to 112/113 call over risk reversal

MNI BONDS: EGBs-GILTS CASH CLOSE: Curves Seal Bear Steepening For The Week

European curves bear steepened Friday to cap modest losses for the week, with Bunds underperforming Gilts.

- A Japanese bond selloff overnight after the BOJ's rate hike set a negative tone that was picked up by long-end EGBs in early trade, with the broader German bear steepening move resuming following Thursday's ECB decision.

- Eurosystem sources told MNI's Policy Team that ECB policymakers think the deposit rate is likely to remain on hold for an extended period.

- Yields were also underpinned in afternoon trade as NY Federal Reserve President Williams downplayed any dovish policy implications of the week's major US data.

- 10Y Bund yield held just below the 2.90% level but posted its highest daily close since March.

- In data, the ECB's forward looking wage tracker continues to point to downside pay pressures next year. UK retail sales were on the soft side while UK public finance data was slightly worse than expected (a negative for Gilts).

- The day's move ensured a bear steepening move for the week as a whole: UK 2Y yield +0.6bp/10Y + 0.7bp; Germany 2Y flat/10Y+3.8bp.

- Periphery/semi-core EGB spreads closed a little wider, with OATs underperforming on a failure by the Government to pass its full budget before year-end.

- Next week's holiday-shortened schedule includes final GDP data for the UK and Spain, while we get a few ECB speakers on Monday (Simkus, Vujcic, Kazimir).

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.7bps at 2.154%, 5-Yr is up 3.8bps at 2.488%, 10-Yr is up 4.5bps at 2.895%, and 30-Yr is up 5.1bps at 3.536%.

- UK: The 2-Yr yield is up 0.8bps at 3.753%, 5-Yr is up 3.4bps at 3.971%, 10-Yr is up 4.3bps at 4.524%, and 30-Yr is up 4.7bps at 5.255%.

- Italian BTP spread up 0.1bps at 69bps / French OAT up 1bps at 71.6bps

MNI OPTIONS: Subdued Trade Post-ECB/BOE Highlighted By Rates Call Structure Buying

Friday's Europe rates/bond options flow included:

- RXG6 119p, bought for 1 in 1k / RXG6 118.5p, bought for 1 in 2.25k / RXG6 118p, bought for 1 in 5k

- ERU6 98.00/98.12cs vs 97.75/97.62ps, bought the cs for half in 10k

- ERZ6 98.25/98.37cs, bought for 1.5 in 14k

- SFIJ6 96.65/96.70/96.75/96.80c condor, bought for 1 in 15k

MNI FOREX: Friday Focus on Post-BOJ Yen Weakness, DXY Touch Higher on Week

- All the focus in FX markets Friday was on the weaker Yen following the Bank of Japan’s expected rate hike. BOJ Governor Kazuo Ueda laid the groundwork for further interest rate increases after the BOJ’s board decided on a unanimous 25-basis-point hike to the highest level in three decades on Friday, but provided little clue as to timing and stressed that policymakers must examine the impact of higher rates on the economy, inflation and financial conditions.

- USDJPY extended its post US employment squeeze, which was likely exacerbated by short-term positioning dynamics as we approach the holiday period. The path of least resistance remains lower for the Yen, and the limited conviction across the FX space has bolstered the underlying bearish JPY theme.

- As such, USDJPY rose 1.26% on the session and trade around 157.50 as we approach the weekend close. Price action has significantly narrowed the gap to the recent cycle highs at 157.89, the Nov 20 high and a bull trigger. A break of this hurdle would confirm a resumption of the uptrend.

- Late comments from Katayama continued to sound the alarm on excessive one-sided moves in the JPY but has done little to impact intra-day sentiment overall.

- The only other notable mover on Friday was the New Zealand dollar, with NZDUSD extending its moderate reversal lower following dovish leaning remarks from Governor Breman and soft revisions within the latest GPD data. This has helped NZDUSD fall further back below the medium-term pivot of 0.5800, and boosted AUDNZD back towards 1.1500.

- Overall this week, the long-awaited return of tier-one US data did little to move the needle for both fed expectations and the USD. The DXY put in a 0.9787 low post-NFP on Tuesday and has subsequently risen around 0.75%, looking set to post moderate gains on the week.

- In emerging markets, renewed weakness for HUF following the NBH meeting and ongoing struggles for BRL amid mounting political uncertainty in Brazil are notable. MXN maintains its resilient profile in the face of a still dovish-leaning Banxico.

MNI US STOCKS: Late Equities Roundup: Tech-Stocks Maintain Support on Narrow Ranges

- Stocks remain firm late Friday, trading sideways on narrow ranges for much of the session. Currently, the DJIA trades up 272.43 points (0.57%) at 48225.46, S&P E-Mini Futures up 57.75 points (0.85%) at 6888.75, Nasdaq up 268.5 points (1.2%) at 23275.47.

- Despite ongoing concerns over valuations, Information Technology sector shares led advances for the second consecutive session, followed by select Consumer Discretionary sector shares - mostly travel related.

- Memory-chip stocks continued to power higher Friday with Sandisk gaining 8.15% - carry over support after Micron beat expectations yesterday with MU up another 7% today after surging 12.5% higher yesterday.

- Next up was Oracle +7.32% following reports of a joint venture with TikTok expected to boost revenues. Additional tech sector gains included: Advanced Micro Devices +6.25%, Lam Research +4.20%, Arista Networks +5.35%, Super Micro Computer +4.43% and Western Digital +4.03%.

- Consumer Discretionary sector gainers included: Carnival +8.63%, Norwegian Cruise Line +5.48%, Royal Caribbean Cruises +2.65% and DoorDash +2.72%.

- Conversely, the list of leading laggers included: Lamb Weston Holdings down a whopping -24.46% on increased price pressures, NIKE -10.86%, Lululemon Athletica -2.86%, DR Horton -2.77%, Darden Restaurants -2.15%, PulteGroup -2.47% and Conagra Brands -2.11%.

MNI EQUITY TECHS: E-MINI S&P: (H6) Corrective Cycle

- RES 4: 7037.85 2.0% Upper Bollinger Band

- RES 3: 7014.00 High Oct 30 and the bull trigger

- RES 2: 6932.25/6988.00 High Dec 15 / 12

- RES 1: 6866.91 20-day EMA

- PRICE: 6843.50 @ 14:17 GMT Dec 19

- SUP 1: 6771.50 Low Dec 18

- SUP 2: 6737.71 61.8% retracement of the Nov 21 - Dec 11 rally

- SUP 3: 6678.58 76.4% retracement of the Nov 21 - Dec 11 rally

- SUP 4: 6583.00 Low Nov 21

A pullback in S&P E-Minis has resulted in a breach of both the 20- and 50-day EMAs. This strengthens a short-term bear threat and signals scope for a deeper retracement of the recent bull phase between Nov 21 - Dec 11. Sights are on 6737.71, a Fibonacci retracement. Note that the key support and reversal trigger lies at 6583.00, the Nov 21 low. For bulls a resumption of gains would refocus attention on key resistance at 7014.00, the Oct 30 high.

COMMODITIES

MNI AMERICAS OIL: Americas End of Day Oil Summary: WTI Down 1.4% on Week

Oil prices are ticking up further today after a recovery earlier this week amid concern that the US could introduce further Russia sanctions. The overall trend remains lower, down around 1.4% on the week, with ongoing concerns of a 2026 supply glut while the impact of geopolitical events for now appear short lived.

- WTI JAN 26 up 0.9% at 56.66$/bbl

- Bajer Hughes US rig count: Oil: 406 (-8) - down 77 rigs, or 15.9% on the year. This is the lowest since Sep. 2021

- US Secretary of State Marco Rubio said Dec. 19 that nothing will impede US enforcement of sanctions in the Caribbean.

- Hyperion, a tanker sanctioned by the US for transporting Russian oil, is on track to test President Trump’s blockade: Bloomberg

- US President Donald Trump said he believes Ukraine peace talks in are "getting close to something" ahead of a US-Russian meeting this weekend.

- Putin told his annual press conference on Friday that Russia does not believe Ukraine is ready for peace talks.

- WTI is expected to average $52/bbl next year, Goldman Sachs said.

- North Dakota’s oil produced 1.168m b/d of oil in October, the state said.

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 22/12/2025 | 0700/0700 | * | Quarterly current account balance | |

| 22/12/2025 | 0700/0700 | *** | GDP Second Estimate | |

| 22/12/2025 | 0900/1000 | ** | PPI | |

| 22/12/2025 | 1330/0830 | * | Industrial Product and Raw Material Price Index | |

| 22/12/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 22/12/2025 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 22/12/2025 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 22/12/2025 | 1800/1300 | * | US Treasury Auction Result for 2 Year Note |