MNI ASIA MARKETS ANALYSIS: Tsys Retreat Late, Gov Remains Shut

HIGHLIGHTS

- Treasuries look to finish near late session lows as another US Government funding bill fails to pass in the Senate - data generated by government remains suspended into next week.

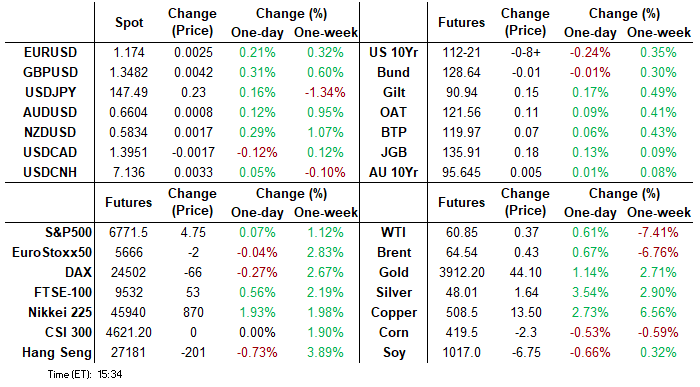

- Projected rate cut pricing has retreated slightly from early morning levels (*): Oct'25 at -24.2bp (-24.5bp), Dec'25 at -45.9bp (-47.1bp), Jan'26 at -57.2bp (-59bp), Mar'26 at -68.2bp (-71.1bp).

- Profit taking saw US stocks consolidate off new record highs tapped this morning, Consumer Discretionary, Information Technology and Communication Services led decliners in late trade.

US TSYS

US TSYS: Tsys Extend Late Session Lows, Gov Remains Closed, Data Suspended

- Treasuries extend lows after the bell - coinciding with reports that another vote to end the Govt shutdown has failed to pass in the Senate. Tsy Dec'25 10Y contract slips to 112-20.5 low -9 (yld 4.1172% +.0346); Curves mixed: 2s10s +.161 at 54.343, 5s30s -1.557 at 100.094.

- Treasuries retreated from modest session opener levels after it became aware the Sep employment data would NOT be released. Futures extended lows slightly after mixed ISM Services data (index and new orders lower than expected; prices paid & employment higher).

- The headline Services PMI index fell more than anticipated, to 50.0 (51.7 expected, 52.0 prior), with multiple key sub-indices showing signs of weakness. The Business Activity index (the equivalent of "Production" in the Manufacturing survey) making headlines with its 5.1 point fall to 49.9, the first contraction since May 2020 (it touched 50.0 in May).

- The USD Index traded inside the weekly range throughout Friday trade, leaving markets of the view that a prolonged US government shutdown that limits government data releases will do very little to deter the Fed from proceeding with a second rate cut at their October rate decision.

- Look ahead: No data scheduled or Fed speakers for Monday. Tuesday's Trade Balance & Import/Export data suspended due to the Gov shutdown. US Treasury supply kicks off Monday with $84B 13W & $75B 26W bill auctions (1130ET).

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.20% (+0.00), volume: $3.022T

- Broad General Collateral Rate (BGCR): 4.17% (+0.01), volume: $1.167T

- Tri-Party General Collateral Rate (TCR): 4.17% (+0.01), volume: $1.137T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.09% (+0.00), volume: $102B

- Daily Overnight Bank Funding Rate: 4.09% (+0.00), volume: $187B

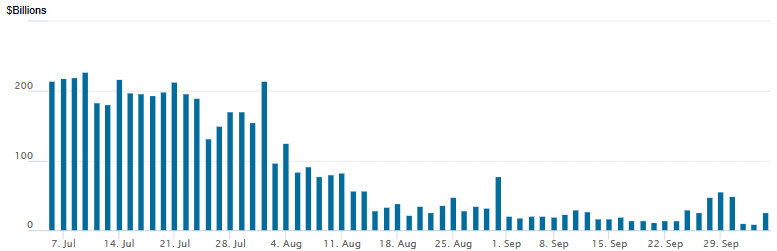

FED Reverse Repo Operation - New Multi Year Low

RRP usage rebounds to $25.392B with 14 counterparties this afternoon, after falling to the lowest level since early April 2021 yesterday with: $8.436B. Compares to the year's high usage of $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

Option desks reported better SOFR/Treasury call option trade on net, relatively light volumes as markets ruminate over the lack of September employment data due to the US Gov shutdown. Underlying Tsy futures holding narrow range on weaker levels since midmorning, projected rate cut pricing has retreated slightly from early morning levels (*): Oct'25 at -24.2bp (-24.5bp), Dec'25 at -45.9bp (-47.1bp), Jan'26 at -57.2bp (-59bp), Mar'26 at -68.2bp (-71.1bp).

SOFR Options:

over +15,000 SFRZ5 96.12/96.25/96.37 call flys, 1.75 ref 96.335

+5,000 SFRZ5 96.25/96.43 call spds, 9.5 ref 96.335

+2,500 SFRH6 96.43/96.56/96.68 call flys, 1.5 vs 96.555/0.10%

-5,000 SFRX5 96.50/97.00 call spds, 1.25 vs. 96.345/0.12%

+5,000 SFRZ5 96.50/96.362 call spds 0.75 over 96.06 put vs. 96.345/0.17%

+24,000 SFRZ5 96.18/96.25/96.31/96.37 call condors, 1.0 ref 96.34 to -.345

+7,000 SFRZ5 96.12/96.18/96.25 put trees, 0.75 ref 96.34

+4,000 SFRH6 96.75/96.87 call spds, 2.75

Block: 3,000 0QX5 96/93/97.06 call spds w/ 0QX5 96.81/96.37 put spds, iron fly 10.0 net cr

+2,000 SFRX5 96.25/96.31/96.43/96.50 call condors, 3.5 ref 96.34

+2,000 SFRX5 96.43/96.56 call spds, 1.5

Treasury Options:

2,500 TYZ5 113 calls, 42 ref 112-24

1,250 USX5 115 puts, 18 ref 117-00

4,000 TYX5 114.5 calls, 4 ref 112-24

1,500 FVX5 108.5 puts, 3 total volume over 11k

2,000 TYZ5 111.5 puts, 20 total volume over 14.4k

-8,000 TYZ5 111.5/114 strangles, 41

50,000 TYX5 120.25 calls ref 112-26.5, cab

5,000 FVX5 108.5/109.5 strangles, 20.5

6,000 TYX5 112/113.5 strangles vs. 10,000 TYZ5 112/113.5 strangles

+2,000 FVX5 108/108.25/108.75 broken put trees, 2.5 vs. 109-13.25/0.07%

2,650 TYZ5 114 calls, 25 ref 112-28.5

MNI BONDS: EGBs-GILTS CASH CLOSE: Core Curves Bull Flatten For The Week

Gilts outperformed Bunds Friday.

- With the US government shutdown postponing the September nonfarms payrolls report, core FI saw little clear direction and lighter-than-usual volumes.

- The session low in core yields (and wides in OAT/Bund) was made just after noon London time, on news that the French Socialist leader had pushed back on PM Lecornu's fiscal proposals. From there, yields drifted back toward the middle of the morning's range into the week's close.

- In data, Eurozone August PPI was a little weaker than expected, while Italian and Spanish Services PMIs were solid.

- The German curve twist flattened, with the UK curve down in parallel through the 10Y segment and outperforming Bunds throughout. For the week, curves bull flattened in both the UK (2Y yield -4.9bp, 10Y -5.6bp) and Germany (2Y -1.1.bp, 10Y -4.8bp).

- Periphery EGB spreads closed a little tighter.

- Ratings reviews after the close include Moody's on the EU. Next week's data schedule is relatively light, with German factory orders the Eurozone highlight. Multiple central bank speakers include ECB's Lagarde at EU Parliament, and BOE's Pill, Mann, and Bailey.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.9bps at 2.019%, 5-Yr is up 0.5bps at 2.302%, 10-Yr is down 0.1bps at 2.698%, and 30-Yr is down 0.7bps at 3.267%.

- UK: The 2-Yr yield is down 1.8bps at 3.966%, 5-Yr is down 1.9bps at 4.118%, 10-Yr is down 2bps at 4.69%, and 30-Yr is down 1.6bps at 5.501%.

- Italian BTP spread down 0.7bps at 81.3bps / French OAT spread down 0.9bps at 81.3bps

MNI EU OPTIONS: Slightly Slower Sonia / Euribor Activity To End Busy Week

Friday's Europe rates/bond options flow included:

- OEX5 117.50/118.25RR, bought the put for -0.25 in 4k

- ERZ5 98.12/98.25cs, bought for 0.75 in 5k

- ERH6 98.18/98.25cs vs 97.87p, bought the cs for flat in 4k

- SFIU5 95.95/95.50ps, 1x3, bought for 0.75 and 1 in 6k

- SFIH6 96.30/96.40/96.50/96.60c condor, bought for 1.75 in 1k

MNI FOREX: Shutdown Persists, But Market Taking in Stride

- Headed through the third session of US government shutdown and markets have been considerably more stable relative to the spells of volatility noted earlier in the week. The USD Index traded inside the weekly range throughout Friday trade, leaving markets of the view that a prolonged US government shutdown that limits government data releases will do very little to deter the Fed from proceeding with a second rate cut at their October rate decision.

- Outside of the US, JPY slipped against all others in G10. This keeps USD/JPY clear of the test of major support into the weekly lows of 146.59, a level that helped prop up price action earlier this week and contain any further USD weakness. Moves follow comments from BoJ's Ueda, who overnight steered clear of any renewed commitment to hiking rates in Japan. While this messaging was inline with prior BoJ communications, it contrasted with the better-than-expected Tankan manufacturing sentiment data out earlier in the week.

- Currency trade was generally more muted elsewhere, leaving major macro themes intact for now. GBP traded mixed, leaving the Autumn Budget as the next major macro risk for the UK. The front-end of the GBP vol curve provides a further signal for market concern over the Autumn Budget. The flatter front-end of the curve and the building premium for 2m implied vols shows markets building a risk premium into the event. 2m vols have posted the sharpest gains over the past week as they begin to capture the event on November 26th.

- US data again will not be released in the coming week, with the government shutdown likely to extend well over the weekend. There remains very little pressure on either side to concede and strike a near-term deal. Outside of the US, focus rests on the Canadian jobs market release, prelim US UMich sentiment data as well as rate decisions from the New Zealand, Poland, Thailand and Philippine central banks.

MNI FX OPTIONS: Expiries for Oct06 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1675-80(E1.4bln), $1.1700(E1.2bln), $1.1750(E926mln), $1.1800(E943mln)

- USD/JPY: Y146.00($1.3bln), Y147.00($2.6bln), Y147.70-80($877mln), Y147.95-00($756mln)

- AUD/USD: $0.6568-70(A$1.3bln), $0.6700(A$1.1bln)

MNI US STOCKS: Late Equities Roundup: Scaling Off Record Highs, DJIA Outperforming

- Stock indexes are retreating from record highs set early in Friday's session, the DJIA still outperforming: up 264.77 points (0.57%) at 46,783.38 vs. record high of 47,049.64, S&P E-Minis down 8.25 points (-0.12%) at 6,759 vs. 6,800.00 record high, Nasdaq down 129.5 points (-0.6%) at 22,717.73 vs. 22,925.43 record high.

- Consumer Discretionary, Information Technology and Communication Services led decliners in late trade, autos and travel related stocks weaker for the second day running: Las Vegas Sands -6.85%, Wynn Resorts -4.84%, Tesla -3.32% and MGM Resorts Int -1.17%.

- Weaker Tech-sector shares included: Palantir Technologies -7.15%, Jabil -4.49%, Dell Technologies -3.07% and Advanced Micro Devices -2.69%. Meanwhile, online media and entertainment shares weighed on the communication sector: Meta Platforms -1.69%, Warner Bros Discovery -1.38%, Live Nation Entertainment -0.92% and Match Group -0.82%.

- On the positive side, Health Care and Utility sector shares continued to lead gainers in the second half, carry over support for pharmaceutical stocks after Pres Trump announced a direct-to-consumer website for discounted drug purchases. Leading gainers included Humana +9.80%, Cigna Group +5.40%, Centene Corp +4.64%, Elevance Health and Align Technology both +3.75%.

- The Utility sector buoyed by NextEra Energy +2.83%, Pinnacle West Capital +2.53%, Sempra+2.46%, Entergy +2.34% and Eversource Energy +2.01%.

MNI EQUITY TECHS: E-MINI S&P: (Z5) Northbound

- RES 4: 6831.38 2.500 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 3: 6812.29 2.382 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 2: 6800.00 Round number resistance

- RES 1: 6787.63 1.382 proj of the Aug 1 - 15 - 20 price swing

- PRICE: 6777.50 @ 14 26 ET Oct 3

- SUP 1: 6675.82 20-day EMA

- SUP 2: 6611.00 Low Sep 17

- SUP 3: 6558.72 50-day EMA

- SUP 4: 6506.50 Low Sep 5

A bull cycle in S&P E-Minis remains intact. The contract has traded to a fresh cycle high this week to confirm a resumption of the uptrend and maintain the positive price sequence of higher highs and higher lows. Sights are on 6787.63, a Fibonacci projection. Initial support to watch is at the 20-day EMA, at 6675.82. It has recently been pierced, a clear break of it would signal scope for a deeper pullback, potentially towards the 50-day EMA, at 6558.72.

COMMODITIES

MNI AMERICAS OIL: Americas End of Day Oil Summary: Crude Higher

WTI crude prices regained some ground amid rising tensions in the Middle East, although are still on track for a net decline on the week, with OPEC expected to raise output at its Sunday meeting. Initial firm resistance has been defined at $66.42, the Sep 29 high. A break of this level would highlight a reversal.

- An explosion and fire occurred at Chevron’s El Segundo refinery near LA late Oct. 2, affecting the isomax unit, which produces jet fuel from heavy gasoil. This is temporarily bullish for jet fuel on the West Coast.

- Baker Hughes US rigs: Oil: 422 (-2) - down 57 rigs, or 11.9% on the year.

- President Trump has said in a Truth Social post that if an agreement is not reached with Hamas by 6pm ET on Sunday, all hell will break out against Hamas.

- OPEC, which meets on Sunday, increased the October target by 137kb/d and at least that amount is likely in November although with conflicting reports on the size of a potential hike of up to 500kb/d. OPEC crude output rose by 400k b/d in September as the group formally completed the unwinding of 2.2m b/d of cuts, Bloomberg reports.

- WTI Nov futures were up 0.6% at $60.88

- WTI Dec futures were up 0.6% at $60.50

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 06/10/2025 | 0700/0900 | ** | Industrial Production | |

| 06/10/2025 | 0700/0900 | ** | Unemployment | |

| 06/10/2025 | 0730/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 06/10/2025 | 0730/0930 | *** | HCOB France Construction PMI | |

| 06/10/2025 | 0730/0930 | ECB de Guindos Speech at Diario Expansion | ||

| 06/10/2025 | 0800/1000 | ECB Lane Keynote at ECB MonPol Conference | ||

| 06/10/2025 | 0830/0930 | ** | S&P Global/CIPS Construction PMI | |

| 06/10/2025 | 0900/1100 | ** | EZ Retail Sales | |

| 06/10/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 06/10/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 06/10/2025 | 1700/1900 | ECB Lagarde at ECON Hearing, European Parliament | ||

| 06/10/2025 | 1730/1830 | BOE Bailey Keynote at Scotland Global Investment Summit | ||

| 07/10/2025 | 2330/0830 | ** | Household spending |