MNI ASIA MARKETS ANALYSIS: Trade Optimism Eases Slightly

HIGHLIGHTS

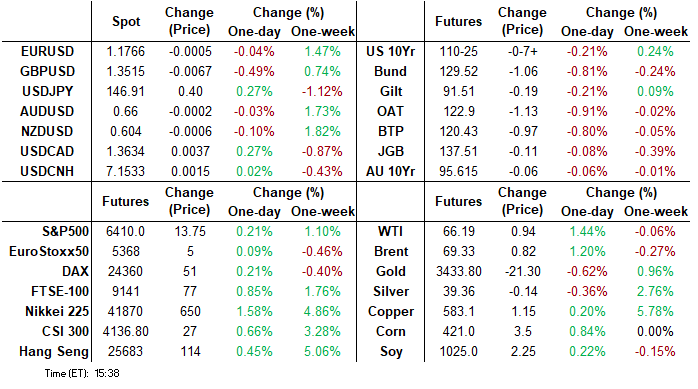

- Treasuries added to the midweek decline Thursday, retreating after lower-than-expected initial claims reading, the dataset continuing to ease back from the multi-month high registered in June.

- New Home Sale missed estimates & mixed S&P PMIs: Manufacturing lower than expected while Services and Composite are higher than expected spurred midmorning short covering that evaporated in the second half.

- The ECB held its benchmark rate steady at 2% for the first time after seventh consecutive cuts, Pres Lagarde indicating that the ECB will keep its meeting-by-meeting approach as geopol & trade uncertainty remains.

- The US dollar index trades on a slightly firmer footing Thursday, and was supported at the margin by the lower-than-expected jobless claims data and a firm July services PMI.

US TSYS

MNI US TSYS: Yields Gain After Mixed Data, New Home Sales Dip

- Treasuries added to the midweek decline Thursday, retreating after lower-than-expected initial claims reading (to a 14-week low 217k vs. 226k expected, 221k prior unrevised), the dataset continuing to ease back from the multi-month high registered in June.

- New Home Sale missed estimates (627k SAAR vs. 650k expected, 623k prior) & mixed S&P PMIs: Manufacturing lower than expected while Services and Composite are higher than expected spurred midmorning short covering that evaporated in the second half.

- After the bell, Sep 10Y Tsy futures trade -7 at 110-25.5 vs. 110-19.5 low. Key support remains intact at 110-08+, the Jul 14 and 16 low. A move through this support would reinstate a bearish theme.

- The ECB held its benchmark rate steady at 2% for the first time after seventh consecutive cuts, Pres Lagarde indicating that the ECB will keep its meeting-by-meeting approach as geopol & trade uncertainty remains.

- The US dollar index trades on a slightly firmer footing Thursday, and was supported at the margin by the lower-than-expected jobless claims data and a firm July services PMI, BBDXY +1.66 at 1194.75.

- Looking to Friday's data, Durable Goods Orders and Cap Goods Orders Nondef Ex Air expected at 0830ET, Kansas City Fed Services Activity at 1100ET.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.28% (+0.00), volume: $2.659T

- Broad General Collateral Rate (BGCR): 4.27% (+0.00), volume: $1.110T

- Tri-Party General Collateral Rate (TCR): 4.27% (+0.00), volume: $1.088T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $115B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $283B

FED Reverse Repo Operation

RRP usage retreats to $132.186B this afternoon from $196.374B yesterday, total number of counterparties at 28. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021 - compares to July 1: $460.731B highest usage since December 31.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury option flow remained mixed on modest volumes Thursday, underlying futures adding to yesterday's sell-off, TYU5 back at early Monday levels (110-26, -6.5). Projected rate cut pricing cools slightly vs. late Wednesday (*) levels: Jul'25 at -0.06bp (-1.2bp), Sep'25 at -16.4bp (-16.6p), Oct'25 at -27.1bp (-28.1bp), Dec'25 at -43.1bp (-44.3bp). Year end projection well off early July level of appr -65.0bp.

SOFR Options:

+5,000 SFRU5 95.87/96.00/96.12 call fly w/ 95.62/95.75 1x2 call spd strip, 5.5

+8,000 SFRU5 95.62 puts, cab

+5,000 SFRV5 96.25/96.50 call spds 3.87

+4,000 SFRZ5 95.75/95.87/96.25/96.37 put condors, 6.0

+2,500 SFRU5 96.18/96.25 call spds, 0.25 ref 95.83

+2,000 SFRV5 96.12/96.25/96.37 call flys, 1.75 vs. 96.095/0.05%

+5,000 SFRU5 95.81/96.00/96.06/96.18 broken put condors, 1.25 ref 95.825

10,000 SFRU5 95.75/95.81/95.93/96.00 call condors ref 95.83

4,000 SFRU5 95.81 puts

3,900 SFRZ5 95.87 puts

-1,000 SFRU5 95.87/96.00/96.06/96.18 call flys, 2.5

Treasury Options:

+23,000 TYU5 105 puts, 1

over 7,500 FVQ5 108 puts, 1-3

6,000 TYU5 110 puts, 27 ref 110-21.5

2,000 wk1 TY 111 calls, 26 ref 110-28 (exp 8/1)

over 10,400 TYU5 113 calls, 9 ref 110-29.5 to -30

+2,000 TYQ5 111/111.25 call spds, 5 ref 110-28.5

+4,000 TYQ5 110 puts, 1 ref 110-30.5

1,000 USU5 111/112 put spds, 18 ref 113-13

MNI BONDS: EGBs-GILTS CASH CLOSE: "On Hold" ECB Drives German Bear Flattening

EGBs underperformed global counterparts Thursday after a more hawkish-than-expected communication from the ECB meeting.

- Along with the fully expected rate hold, President Lagarde didn't do much to encourage expectations of further rate cuts. She said "you could argue that we are on hold" and that the ECB is "in a good place now to hold" pending incoming data and developments.

- The usual Bloomberg/Reuters ECB sources reports after the meeting pointed to a high bar for a September cut.

- Solid US jobless claims data also weighed, with Treasury weakness spilling over.

- In European data, flash Eurozone PMI data was a little better than expected, with manufacturing in line and services above-consensus, while UK PMI data was mixed (manufacturing beat slightly, but services missed).

- The hawkish repricing of near-term ECB policy resulted in the German curve bear flattening sharply, with UK yields lower across the curve but the short- and long-end outperforming.

- Periphery EGBs underperformed, with10Y Italian and Greek spreads to Bunds rising 2-3bp.

- Friday's schedule includes UK retail sales and the German IFO survey.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 8.8bps at 1.932%, 5-Yr is up 8.7bps at 2.281%, 10-Yr is up 6.3bps at 2.702%, and 30-Yr is up 1.9bps at 3.192%.

- UK: The 2-Yr yield is down 1.9bps at 3.862%, 5-Yr is down 1.2bps at 4.032%, 10-Yr is down 1.3bps at 4.622%, and 30-Yr is down 2.2bps at 5.46%.

- Italian BTP spread up 2.5bps at 84.8bps / French OAT up 0.3bps at 67bps

MNI EGB OPTIONS: Multiple UK/Euro Rate Trades Pre-ECB

Thursday's Europe rates/bond options flow included:

- DUU5 107.20 puts vs. 107.235 (47% delta) 5K given at 10.5

- RXU5 128.50/127.50 put spread paper paid 17 on 5K

- ERQ5 98.12/98.18/98.25 call fly paper paid 1 on 6.5K

- SFIV5 96.50/96.60 call spread vs. 96.305 (8% delta) paper paid 1.25 on 4K

- SFIX5 96.20/15/05 put ladder paper paid 0.25 on 5K

MNI FOREX: EURGBP Rises Above 0.8700, Approaches 2025 Highs

- Currency markets have had a lacklustre tone on Thursday, with a lack of meaningful macro developments potentially underpinning a subdued summer tone. With that said, the ECB holding interest rates and sounding notably constructive on euro area growth combined with poorer-than-expected UK PMI data have elevated EURGBP to a fresh 3-month high above the 0.8700 handle.

- EURGBP price action built momentum after breaking above a cluster of daily highs across July, just below the 0.8700 mark, placing the focus on key resistance at 0.8738, the Apr 11 high. Above here, 0.8781 would be the next chart point of note, the 2.236 projection of the Mar 3 - 11 - 28 price swing. Sterling has been the standout underperformer in G10, prompting GBPUSD to trade back below 1.3550, currently down 0.2% on the session at 1.3510 as we approach the APAC crossover.

- The US dollar index trades on a slightly firmer footing Thursday, and was supported at the margin by the lower-than-expected jobless claims data and a firm July services PMI. This has particularly helped USDJPY to extend its intra-day bounce to over 100 pips. It is worth noting that overnight, USDJPY’s low at 145.85 broadly matched the pair’s 50-day EMA, which will have likely been influential in the subsequent bounce. Overall, a technical bull cycle in USDJPY does remain in place, with the recent phase of weakness appearing to be a corrective retracement from recent highs. A sustained break of the 50-day is needed to highlight a stronger bearish reversal.

- This more stable backdrop for the dollar has prompted AUDUSD to edge lower from the cycle highs printed earlier in the session at 0.6625. Constructive domestic data and comments from RBA Governor Bullock helped propel AUDUSD above key resistance and the 0.66 handle to register fresh 8-month highs. Above here, resistance is scant until 0.6688, the Nov 07 high, printed shortly after the US election last year.

- Tokyo CPI kicks off Friday’s economic calendar, before UK retail sales, German IFO and US durable goods.

FX OPTIONS: Expiries for Jul25 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1700(E679mln), $1.1740-50(E1.7bln), $1.1800(E2.1bln)

- USD/JPY: Y145.00($1.2bln), Y146.00($841mln), Y147.75-85($600mln)

- EUR/GBP: Gbp0.8725-50(E892mln)

- AUD/USD: $0.6450($552mln)

- USD/CAD: C$1. C$1.3700-20($1.2bln)

MNI US STOCKS: Late Equities Roundup: Dow Continues to Lag SPX & Nasdaq

- Stocks remain mixed Thursday, while SPX emini and Nasdaq indexes continue to mark new record highs (6416.75 & 21107.83 respectively), the DJIA trades weaker in late trade (appr 235.0 pts off December 4 record high). Currently, the DJIA trades down 187.71 points (-0.42%) at 44822.82, S&P E-Minis up 17.5 points (0.27%) at 6413.75, Nasdaq up 84 points (0.4%) at 21103.65.

- While strong earnings continue to support a broad swath of Communication Services, IT, Financials and Health Care sector shares, foreign trade policy optimism that buoyed stocks in the first half of the week has started to wane.

- Health Care sector shares were supported by pharmaceutical, leaders included: West Pharmaceutical Services +20.30%, Labcorp Holdings +6.75%, Charles River Laboratories +6.73% and Bio-Techne +5.57%. Other leaders included United Rentals +8.38%, Nasdaq +7.31%, Albemarle +6.55%, T-Mobile US +6.06% and Allegion +5.20%.

- On the flipside, leading decliners late Thursday included: LKQ -20.62%, Dow -18.19%, Chipotle Mexican Grill -13.98%, Southwest Airlines -10.84%, LyondellBasell Industries -10.19%, Tesla -8.85%, IBM -7.53% and ON Semiconductor Corp -6.32%.

- Earnings announcements expected after today's close: Boyd Gaming Corp, Weyerhaeuser, Digital Realty Trust, Newmont, Hexcel, Intel Corp, Deckers Outdoor, Edwards Lifesciences and Comfort Systems USA.

- Expected tomorrow: Phillips 66, Saia Inc, HCA Healthcare, Centene, Xerox Holdings, Skechers USA, Charter Communications and Booz Allen Hamilton.

MNI EQUITY TECHS: E-MINI S&P: (U5) Fresh Cycle High

- RES 4: 6500.00 Round number resistance

- RES 3: 6477.31 1.618 proj of the May 23 - Jun 11 - 23 price swing

- RES 2: 6439.88 1.500 proj of the May 23 - Jun 11 - 23 price swing

- RES 1: 6418.25 High Jul 24

- PRICE: 6406.00 @ 1310 ET Jul 24

- SUP 1: 6318.75 Low Jul 22

- SUP 2: 6277.23/6131.47 20- and 50-day EMA values

- SUP 3: 6075.25 Low Jun 24

- SUP 4: 5959.00 Low Jun 23

S&P E-Minis have once again traded to a fresh cycle high this week. The climb confirms a resumption of the uptrend and maintains the price sequence of higher highs and higher lows. Note that moving average studies are in a bull-mode position highlighting a clear dominant uptrend. With the 6400.00 handle cleared, sights are on 6439.88, a Fibonacci projection. Key support is at the 50-day EMA, at 6131.47. Support at the 20-day EMA is at 6277.23.

MNI COMMODITIES: Crude Edges Higher, Gold Continues To Falter

- Crude has pared gains later in the session as the WSJ reported that Chevron can resume operations in Venezuela. Earlier in the session, oil prices were gaining ground amid trade optimism as the EU said a trade deal with the US was in reach following a US-Japan trade deal on Wednesday.

- WTI Sep 25 is up by 0.8% at $65.8/bbl.

- The WSJ report’s details are unclear, but it follows recent discussions involving President Trump and Secretary of State Marco Rubio after last week’s prisoner swap where all 10 remaining Americans who were detained by Venezuela were released.

- A bearish theme in WTI futures remains intact and the recovery since June 24 still appears corrective. Support to watch is the 50-day EMA, at $64.74, a clear break of which would expose $58.17, the May 30 low.

- On the upside, initial resistance to monitor is $69.41, the 50.0% retracement of the June 23 - 24 high-low range.

- Meanwhile, spot gold has continued to falter, with a potential softening in US-EU tariff rates helping to push spot down by a further 0.5% today to $3,372/oz.

- Outflows from Chinese ETF’s tied to gold also weighed on the market, according to analysts at TD securities.

- The move lower in gold still appears corrective at this stage, with the 20-day EMA at $3,355.7 providing first support.

- On the upside, first resistance is at $3,439.0, the July 23 high, followed by $3,451.3, the June 16 high.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 25/07/2025 | 0600/0800 | ** | PPI | |

| 25/07/2025 | 0600/0800 | ** | Unemployment | |

| 25/07/2025 | 0600/0700 | *** | Retail Sales | |

| 25/07/2025 | 0645/0845 | ** | Consumer Sentiment | |

| 25/07/2025 | 0800/1000 | ** | M3 | |

| 25/07/2025 | 0800/1000 | ** | ISTAT Consumer Confidence | |

| 25/07/2025 | 0800/1000 | ** | ISTAT Business Confidence | |

| 25/07/2025 | 0800/1000 | *** | IFO Business Climate Index | |

| 25/07/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 25/07/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 25/07/2025 | 1300/1500 | ** | BNB Business Confidence | |

| 25/07/2025 | 1500/1100 | Finance Dept monthly Fiscal Monitor (expected) | ||

| 25/07/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 25/07/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |