MNI ASIA MARKETS ANALYSIS: Strong Risk-Off Move Lacks Driver

HIGHLIGHTS

- Treasuries surged higher later Thursday, TYZ5 revisited Sep 17 highs (113-25.5) apparently a risk-off move/stocks reversed early gains tied to a couple regional banks selling off.

- With no official US data (PPI, retail sales and weekly jobless claims were due today) due to the US government shutdown, market focus remains on alternative measures of economic activity and today's releases were poor.

- Friday's Housing Starts/Permits, Import/Export Prices suspended due to the Gov shutdown. Meanwhile, the Federal Reserve has temporarily suspended the release of its Industrial Production data due to the shutdown as well.

US TSYS

MNI US TSYS: Risk-Off Round Two: Insurers Weigh on Financials

- Treasuries poised to extend session highs, TYZ5 113-25.5 - highest since September 17/pst FOMC knee jerk high - as equities extend lows again after rebounding off midday lows.

- Again, no specific headline or Block related trade to cite for the move, though some desks pointing to overreaction of story on two regional banks getting hit (Zions and Western Alliance Bancorp) that was mentioned earlier.

- Currently, the DJIA is down 409.64 points (-0.89%) at 45,843.87, S&P E-Minis down 72.25 points (-1.08%) at 6,644, Nasdaq down 222.9 points (-1%) at 22,448.95.

- The Financials sector is leading the decline at the moment, but primarily due to insurers: Marsh & McLennan -8.07%, Arthur J Gallagher & Co -6.47%, Brown & Brown Inc -6.36%.

- Tsy Dec'25 10Y futures trade 113-25.5 (+17.5), 10Y yield 3.9726% (-.0556). Rally narrows the gap with the 113-29 bull trigger in the process. This strengthens the underlying bullish theme, signaling scope for a stronger rally. Clearance of 113-29 would confirm a resumption of the M/T uptrend.

- Look ahead: Friday's Housing Starts/Permits, Import/Export Prices suspended due to the Gov shutdown. Meanwhile, the Federal Reserve has temporarily suspended the release of its Industrial Production data due to the shutdown as well.

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.29% (+0.10), volume: $3.059T

- Broad General Collateral Rate (BGCR): 4.25% (+0.09), volume: $1.183T

- Tri-Party General Collateral Rate (TCR): 4.25% (+0.09), volume: $1.141T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.10% (+0.00), volume: $81B

- Daily Overnight Bank Funding Rate: 4.10% (+0.00), volume: $165B

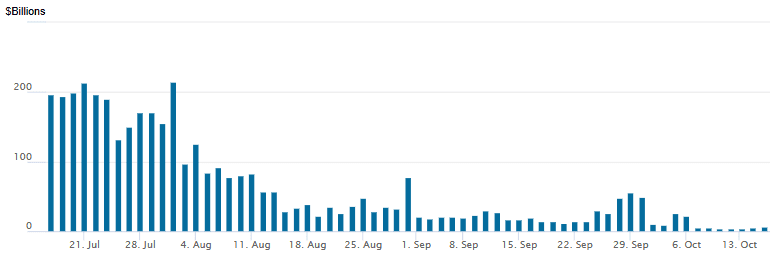

FED Reverse Repo Operation

RRP usage inches up to $6.960B with 11 counterparties from $5,484B Wednesday. Compares to $3,516B on Tuesday, Oct 13 (lowest level since early April 2021) & this year's high usage of $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR calls & Treasury options shifted to upside calls & call spreads Thursday as underlying rates rallied/extended highs on an apparent risk-on move with stocks ratcheting lower/off early session highs. Projected rate cut pricing gained traction vs. late Wednesday levels (*): Oct'25 at -25.8bp (-24.2bp), Dec'25 at -52.4bp (-48.4bp), Jan'26 at -67.3bp (-61.5bp), Mar'26 at -81.6bp (-74.4bp).

SOFR Options:

+15,000 SFRX5 96.87 calls, .75-1.0 ref 96.405

+10,000 SFRX5 96.87/96.87 call spds, 0.5 ref 96.425/0.05%

-2,000 SFRZ5 96.37 straddles, 14.75 ref 96.40

+5,000 SFRX5 96.75/96.87 call spds vs. 96.445/0.05%

-10,000 SFRZ5 96.62/96.75 call spds 1.0

+4,000 SFRH6 96.75/97.37 call spds, 10.0

+20,000 SFRZ5 96.62/96.75 call spds, 0.75 vs. 96.375 to -.365/0.05%

-5,000 SFRZ5 96.25/96.43/96.62 call flys, 7.75 ref 96.355

+5,000 0QX5 96.75 puts, 1.5 vs. 97.005/0.10%

Block, 5,000 SFRZ5 96.25/96.31/96.43/96.50 call condors, 4.0

-5,000 SFRX5 96.31/96.37 call spds, 3.5

-5,000 SFRZ5 96.37/96.50/96.56/96.68 call condors, 1.75

+5,000 0QX5 96.87/96.93/97.06/97.18 broken call condors, 1.0 ref 97.095/0.05%

+1,000 SFRF6 96.68/96.81/96.87/97.00 call condors, 1.75 ref 96.60

Treasury Options:

5,000 FVX5 111.75 calls ref 109-31.25

over -43,000 TYZ5 114/115.5 call spds, 24 vs. 113-21/0.26% -- rolling up strikes: recal paper +200k TYZ5 114 calls since from 31-33 in late September to early October. Heavy buyers in TYZ5 113 and 113.5 calls as well

3,300 TUZ5 104.25 puts ref 104-12.38

5,000 TYZ5 111.5/112.5/113.5 put flys, 13 ref 113-08

3,000 FVZ5 109.75/110 strangles

1,500 TYX5 112/112.75/113 broken put trees, 7

-4,500 TYX5 112/114 call over risk reversals, 3

over 27,000 TYG5 114/115/115.5/117 broken call condors ref 113-06

-6,100 FVZ5 108.5/108.75/109.25 broken put trees, 3.5 ref 109-26.5 to -25.75/0.05%

-1,000 TYF6 111/116 strangles, 33

2,000 FVX5 109.75 calls

1,200 USX5 117.5/119 strangles

+/-2,500 wk3 TY 113.25 puts, 6-7 ref 113-10.5

+1,500 TYX5 113 puts, 10 ref 113-12/0.30%

+1,500 FVX5 109.5 puts, 6.5

MNI BONDS: EGBs-GILTS CASH CLOSE: Gilts Outperform Amid Broader Rally

European yields dropped across the board Thursday, with Gilts outperforming.

- While Spanish/French supply helped contain intraday rallies in Bund, ultimately core FI gained through the session as the US Trade Representative made comments seen as ratcheting up Sino-American tensions.

- UK Chancellor Reeves' comments on investigations surrounding regulated prices (which would lessen inflation) appeared to provide some support for Gilts, which outperformed on t he day.

- French PM Lecornu survived no-confidence motions as expected, but fiscal/political risks remain with budget negotiations beginning next week.

- After the cash close, bond futures rose sharply alongside a drop in equities, implying that the cash rally would have continued.

- In data, monthly UK GDP data broadly met expectations, although the details were a little more mixed.

- The German curve twist steepened, with the UK's bull steepening. Periphery/semi-core EGB spreads tightened, led by BTPs.

- Friday's agenda includes final Eurozone September inflation data, and multiple central bank speakers: BOE's Pill, Greene and Breeden, as well as ECB's Rehn and Nagel.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 1.3bps at 1.909%, 5-Yr is down 0.7bps at 2.159%, 10-Yr is down 0.1bps at 2.57%, and 30-Yr is up 1.3bps at 3.159%.

- UK: The 2-Yr yield is down 5bps at 3.852%, 5-Yr is down 4.7bps at 3.954%, 10-Yr is down 4.2bps at 4.501%, and 30-Yr is down 4.2bps at 5.301%.

- Italian BTP spread down 2bps at 78.9bps / French OAT down 1.3bps at 76.2bps

MNI EGB OPTIONS: Thursday's Rate Plays: Upside, Upside, And More Upside

Thursday's Europe rates/bond options flow included:

- RXX5 130/130.50cs, sold at 18 in ~9.7k

- RXZ5 128.00/127.50ps, bought for 5 and 6 in 4k

- ERH6 98.25/98.50cs vs 0RH6 98.25/98.50cs, bought the mid for 2.5 in 9k

- ERH6 98.4375/98.625cs, bought for half in 4.5k

- ERM6 98.43/98.50/98.56c fly, bought for 0.25 in 3k

- ERM6 98.50/98.62/98.75c fly, bought for 0.25 in 35k

- ERM6 98.62/98.75/98.87c fly, bought for 0.25 in 20k

- ERM6 98.25/43/50 call ladder vs 97.87 puts paper pad 0 for the call ladder on 10K

- ERM6 98.50/98.625/98.75/98.875c condor, bought for half in over 15k

- 2RZ5 98.00/98.0625cs, unconfirmed sell at 1.5 in 10k (traded Paper to Paper)

- SFIH6 96.40/96.50/96.55/96.60c condor 1x2x1x2, bought for 0.75 in 4k

MNI FOREX: USD Resolves Lower as Data Deteriorates

- Other than a brief phase of strength into the European open, Thursday trade has generally proved negative for the USD, which resolved lower across both the European and US sessions. The USD Index made light work of any support into yesterday's lows, however more material levels should come into play through 97.891 (50% retracement of bounce off cycle lows) and 97.462.

- With no official US data (PPI, retail sales and weekly jobless claims were due today) due to the US government shutdown, market focus remains on alternative measures of economic activity and today's releases were poor. The Philly Fed Business Outlook came in sharply below expectations, with NY Fed Services Business Activity also deteriorating.

- This, twinned with Treasury estimates that the shutdown is costing $15bln per day, is keeping US yields under pressure, although 4.00% support in 10y yields has held for now.

- Quietly, GBP strength continues to build. Only SEK & NOK have outperformed GBP in spot returns this week and while GBPUSD is close to erasing the early October move lower, it's EURGBP that seems to be more at risk of moving lower. The cross off daily lows, but is still trading either side of the 50-dma (a level that has helped anchor prices over the past fortnight). Price has found very little support from the survival of France's cabinet across two confidence votes today, despite the tightening of the French-German yield spread this week.

- That said, we see the market having more room to reprice a dovish BoE outlook than a dovish ECB outlook, which points to the risk of further downside in the SFIZ6/ERZ6 spread. EURGBP's correlation to 12m forward rates rather than near-term CB expectations is clear - and with more scope for BoE repricing across the course of 2026 relative to the ECB, this could contain protracted downside in spot.

- Friday focus shifts to the final Eurozone CPI print. Housing starts/building permits data and the import/export price indices for September were due, but will likely be rescheduled due to the US government shutdown. Central bank speakers include BoJ's Uchida, BoE's Pill, Breeden & Greene and Fed's Musalem looks to be the final FOMC member speaking before the pre-meeting media blackout.

MNI OPTIONS: Expiries for Oct17 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1510-15(E1.9bln), $1.1650-60(E1.2bln), $1.1670-80(E1.4bln), $1.1690-00(E1.0bln)

- USD/JPY: Y150.25-46($2.5bln), Y152.00($784mln)

- AUD/USD: $0.6540(A$529mln)

MNI US STOCKS: Late Equities Roundup: Regional Bank Pressure?

- Stocks retreated from early session highs, looking to finish near late session lows Thursday after an abrupt risk-off move repeated twice in the second half. No specific headline or Block related trade to cite for the move, though some desks pointed to overreaction of a story on two regional banks getting hit: Zions and Western Alliance Bancorp.

- Currently, the DJIA trades down 354.94 points (-0.77%) at 45,897.05, S&P E-Minis Future down 61.5 points (-0.92%) at 6,652.25, Nasdaq down 176.7 points (-0.8%) at 22,490.57.

- The Financials sector is leading the decline at the moment, but primarily due to insurers: Marsh & McLennan -8.07%, Arthur J Gallagher & Co -6.47%, Brown & Brown Inc -6.36%.

- On the positive side, chip makers continued to support the tech sector as AI demand gained momentum. Bloomberg reported earlier that Taiwan Semiconductor Manufacturing Co "hiked its projection for 2025 revenue growth to the mid-30% range, sending a strong signal of confidence in demand for components like Nvidia Corp chips that power AI."

- Leading chip makers included: Micron Technology +5.05%, ON Semiconductor +5.02%, KLA +1.17% and Monolithic Power Systems +1.13%

- Pharmaceuticals followed close behind with: Mettler-Toledo International +4.10%, Charles River Labs +3.95%, Bio-Techne Corp +3.45% and Revvity +2.15%

MNI EQUITY TECHS: E-MINI S&P: (Z5) Trend Signals Remain Bullish

- RES 4: 6850.87 1.618 proj of the Aug 1 - 15 - 20 price swing

- RES 3: 6831.38 2.500 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 2: 6819.25 1.500 proj of the Aug 1 - 15 - 20 price swing

- RES 1: 6766.75/6812.25 High Oct 15 / High Sep 9 and bull trigger

- PRICE: 6653.75 @ 1524 ET Oct 16

- SUP 1: 6609.91 50-day EMA

- SUP 2: 6540.25 Low Oct 10 and a key short-term support

- SUP 3: 6506.50 Low Sep 5

- SUP 4: 6427.00 Low Sep 2

A sharp sell-off in S&P E-Minis on Oct 10 appears corrective - for now. Price has found support below the 50-day EMA, currently at 6609.91, and the Oct 10 low of 6540.25 has been defined as a key short-term support. Moving average studies remain in a bull-mode position, highlighting a dominant uptrend and positive market sentiment. The bull trigger is 6812.25, the Oct 9 high. A breach of this hurdle would confirm a resumption of the uptrend.

MNI COMMODITIES: Gold, Silver Hit Fresh Record Highs, Crude Still Under Pressure

- Spot gold registered another all-time high of $4,298.7/oz on Thursday, with pullbacks remaining limited and short-lived at this stage.

- Currently, spot is up by 2.0% at $4,292, taking total gains since the start of September to 24%.

- Familiar arguments continue to drive gold demand, namely buying from both official accounts and ETFs, questions surrounding Fed independence, ongoing global trade frictions, broader geopolitical risk, bearish views surrounding the USD and expectations for further Fed easing.

- A further extension higher would target round number resistance at $4,300, followed by $4,317.7, a Fibonacci projection.

- As noted previously, however, gold is in overbought territory. A move down would be considered corrective and would allow the overbought set-up to unwind. Support to watch lies at $3,955.0, the 20-day EMA.

- Meanwhile, silver remains supported by a lack of liquidity in London, which has seen price rise by another 1.8% to $53.99/oz today.

- A bullish trend remains in place, with sights on $54.0 round number resistance, which was pierced earlier. A break would open $54.567, a Fibonacci projection point.

- Elsewhere, oil markets remain under pressure from demand concerns due to the US-China trade tensions and as the IEA raised its forecast of a record surplus.

- WTI Nov 25 is down by 1.3% at $57.5/bbl, testing support around the May 30 low. A break below here would open $54.89, the May 5 low.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 17/10/2025 | 0600/0800 | ** | Unemployment | |

| 17/10/2025 | 0900/1100 | *** | EZ HICP Final | |

| 17/10/2025 | 0935/1035 | BOE Pill Speech at Institute of Chartered Accountants Conference | ||

| 17/10/2025 | 1100/1200 | BOE Greene Roundtable at Atlantic Council | ||

| 17/10/2025 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 17/10/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 17/10/2025 | 1230/0830 | *** | Housing Starts | |

| 17/10/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 17/10/2025 | 1230/0830 | *** | Housing Starts | |

| 17/10/2025 | 1315/0915 | *** | Industrial Production | |

| 17/10/2025 | 1615/1215 | St. Louis Fed's Alberto Musalem | ||

| 17/10/2025 | 1630/1730 | BOE Breeden in Panel at IMF/World Bank Meetings | ||

| 17/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 17/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 17/10/2025 | 2000/1600 | ** | TICS |