COMMODITIES: Gold, Silver Hit Fresh Record Highs, Crude Still Under Pressure

- Spot gold registered another all-time high of $4,298.7/oz on Thursday, with pullbacks remaining limited and short-lived at this stage.

- Currently, spot is up by 2.0% at $4,292, taking total gains since the start of September to 24%.

- Familiar arguments continue to drive gold demand, namely buying from both official accounts and ETFs, questions surrounding Fed independence, ongoing global trade frictions, broader geopolitical risk, bearish views surrounding the USD and expectations for further Fed easing.

- A further extension higher would target round number resistance at $4,300, followed by $4,317.7, a Fibonacci projection.

- As noted previously, however, gold is in overbought territory. A move down would be considered corrective and would allow the overbought set-up to unwind. Support to watch lies at $3,955.0, the 20-day EMA.

- Meanwhile, silver remains supported by a lack of liquidity in London, which has seen price rise by another 1.8% to $53.99/oz today.

- A bullish trend remains in place, with sights on $54.0 round number resistance, which was pierced earlier. A break would open $54.567, a Fibonacci projection point.

- Elsewhere, oil markets remain under pressure from demand concerns due to the US-China trade tensions and as the IEA raised its forecast of a record surplus.

- WTI Nov 25 is down by 1.3% at $57.5/bbl, testing support around the May 30 low. A break below here would open $54.89, the May 5 low.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: Statement: Labor Market Downgrade (1/2)

Going paragraph by paragraph through the previous (July) statement in italics, with areas of interest for the September statement highlighted ( Link to July FOMC statement )

- The resumption of rate cuts at this meeting will necessitate some pretext for the decision, both in the projections and in the Statement. That starts with the opening paragraph which is likely to change the description of labor market conditions, removing the reference to them remaining “solid” and referring to the recent slowdown in payroll growth and rise in the unemployment rate.

- “Inflation remains somewhat elevated” doesn’t require changing.

- The description of economic activity – that in July referred to activity – needs some cleaning up now that we are two months into the third quarter, potentially noting that growth has settled into a solid pace after a volatile first half.

- The language regarding the balance of risks is in danger of shifting to reflect weakening in labor market conditions, but given still-solid incoming inflation prints and risks on the tariff front, the Committee will be content to keep this paragraph unchanged.

- The Statement will of course announce the rate cut decision, but we don’t expect any change in the forward guidance “in considering the extent and timing…”, as it gives the Committee optionality to ease further in future meetings or return to a holding stance, depending on how the data unfolds.

BOC: MNI Instant Answers Eye Nods To Further Easing Potential (2/2)

Statement / Press Conference: With no Monetary Policy Report released at this meeting and thus no new economic projections, there will be initial attention on the decision statement which is expected to remain non-committal on future cuts but retain the overall easing bias. That’s a tone likely to be echoed at the press conference.

- While Governing Council’s message will probably reiterate they are proceeding “carefully” with a meeting-by-meeting approach, the overall meeting communications will leave the door open to another rate cut in October if data continue to develop in a similar direction over the interim period.

MNI's Instant Answers for the BOC decision focus on any signals on future rate moves sent from the 0945ET release Wednesday. They are:

- Target for overnight rate:

- Does the Bank say the case for further rate reductions is strong?

- Does the Bank reiterate it could LOWER rates if the economy weakens and inflation is contained?

- Does the Bank mention core inflation has been elevated?

- Does the Bank say growth or job market prospects have weakened?

- Does the Bank say it may be less forward looking with policy?

BOC: Macro Developments Since July Support Resumption Of Easing Wednesday (1/2)

Summarizing our Bank of Canada preview out earlier today - link here: the BOC is widely expected to cut its benchmark overnight rate by 25bp to 2.50% on Wednesday September 17. This comes after three consecutive holds, amid a period in which activity and labour market data proved more resilient than expected in the face of the US-Canada trade conflict.

- We’ve heard almost nothing from BOC leadership since the July meeting, save for a speech on central bank independence and flexible inflation targeting delivered by Gov Macklem at a Banco de Mexico conference in August. That leaves us with the data to determine the Bank’s likely course of action – and it’s been almost unambiguous in arguing for the resumption of cuts. In our meeting preview we go through the major data releases since the July BOC meeting.

- July’s rate decision noted that “With still high uncertainty, the Canadian economy showing some resilience, and ongoing pressures on underlying inflation, Governing Council decided to hold the policy interest rate unchanged. We will continue to assess the timing and strength of both the downward pressures on inflation from a weaker economy and the upward pressures on inflation from higher costs related to tariffs and the reconfiguration of trade. If a weakening economy puts further downward pressure on inflation and the upward price pressures from the trade disruptions are contained, there may be a need for a reduction in the policy interest rate.”

- Since then, those criteria for a cut appear to have played out in the data:

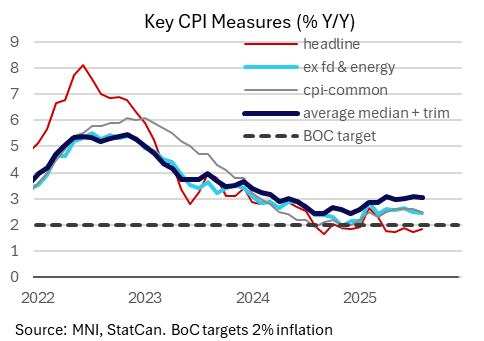

- Inflation Pressures Moderating: August's Canadian CPI data out Tuesday continued July’s theme of steady-to-moderating core inflation after an uncomfortably hot period, and will not present an obstacle to the BOC cutting its benchmark rate Wednesday. This was an important development as the resilience of core inflation was a key component to the BOC’s decision to hold rates through the summer’s trade-related uncertainty. Another factor since that will have helped ease concerns was Canada’s decision to end counter-tariffs on the US at the start of September, taking some of the upside pressure off import prices.

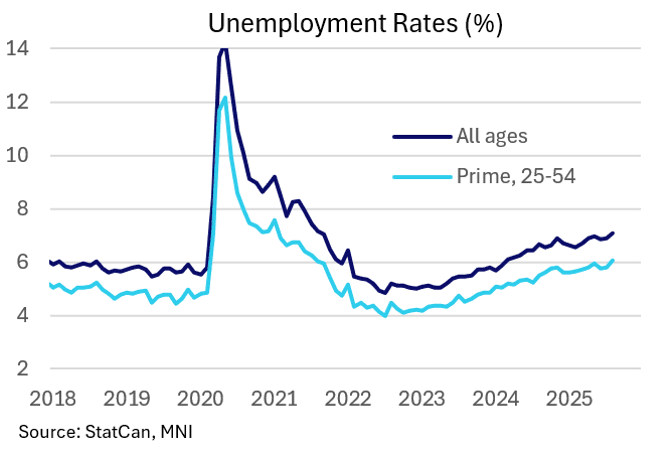

- Jobs Market Softening: The BoC's July meeting deliberations noted "some members expressed concern about the risks of further increases in the unemployment rate and the implications for households if the trade conflict were to escalate or the effects were to spread through the economy more broadly." Data since then will only have increased those concerns. August's Labour Force Survey was unambiguously weak, and in several aspects marked a deterioration from the poor July report, from the fall in employment to the rise in the unemployment rate. Weakness appeared broad-based, including by industry, with continued signs that US-Canada trade tensions are weighing on the labor market. It saw the first back-to-back fall in employment ex-pandemic since 2019, with the unemployment rate rising above 7% (unrounded) since September 2021.

- Growth Recovery Is Limited: The first half of the year concluded on a sour note for growth as Q2 GDP printed -1.6% Q/Q annualized, worst in 5 years, albeit close to the Bank of Canada's "current tariff scenario" of -1.5% and lower than -0.8% consensus expected. That said, the BOC noted in July that in its "current tariff" scenario, "GDP growth picks up to about 1% in the second half of this year as exports stabilize and household spending increases gradually." That's still a plausible outcome, but Bloomberg consensus is now at only 0.2% with a major slowdown in household consumption (0.5% after 4.5%), so at best the recovery looks to be in line with the BOC's previous outlook.