US STOCKS: Late Equities Roundup: Regional Bank Pressure?

- Stocks retreated from early session highs, looking to finish near late session lows Thursday after an abrupt risk-off move repeated twice in the second half. No specific headline or Block related trade to cite for the move, though some desks pointed to overreaction of a story on two regional banks getting hit: Zions and Western Alliance Bancorp.

- Currently, the DJIA trades down 354.94 points (-0.77%) at 45,897.05, S&P E-Minis Future down 61.5 points (-0.92%) at 6,652.25, Nasdaq down 176.7 points (-0.8%) at 22,490.57.

- The Financials sector is leading the decline at the moment, but primarily due to insurers: Marsh & McLennan -8.07%, Arthur J Gallagher & Co -6.47%, Brown & Brown Inc -6.36%.

- On the positive side, chip makers continued to support the tech sector as AI demand gained momentum. Bloomberg reported earlier that Taiwan Semiconductor Manufacturing Co "hiked its projection for 2025 revenue growth to the mid-30% range, sending a strong signal of confidence in demand for components like Nvidia Corp chips that power AI."

- Leading chip makers included: Micron Technology +5.05%, ON Semiconductor +5.02%, KLA +1.17% and Monolithic Power Systems +1.13%

- Pharmaceuticals followed close behind with: Mettler-Toledo International +4.10%, Charles River Labs +3.95%, Bio-Techne Corp +3.45% and Revvity +2.15%

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OUTLOOK: (Z5) Bullish Trend Sequence Intact

- RES 4: 114-10 High Apr 7 (cont.)

- RES 3: 114-10 1.0% 10-dma envelope / High Apr 7 (cont.)

- RES 2: 114-00 Round number resistance

- RES 1: 113-29 High Sep 5

- PRICE: 113-17+ @ 20:03 BST Sep 16

- SUP 1: 112-25+ 20-day EMA

- SUP 2: 112-04 50-day EMA

- SUP 3: 111-13+ Low Aug 18 and a key support

- SUP 4: 110-25 Low Aug 1

Treasury futures remain in a bull-mode condition. Note that the recent impulsive rally signalled an acceleration of the uptrend. Also, moving average studies are in a bull-mode position, highlighting a dominant uptrend. This suggests scope for an extension through 114-00 next and a test of 114-10, the Apr 7 high (cont). Initial firm support to watch is 112-25+, the 20-day EMA.

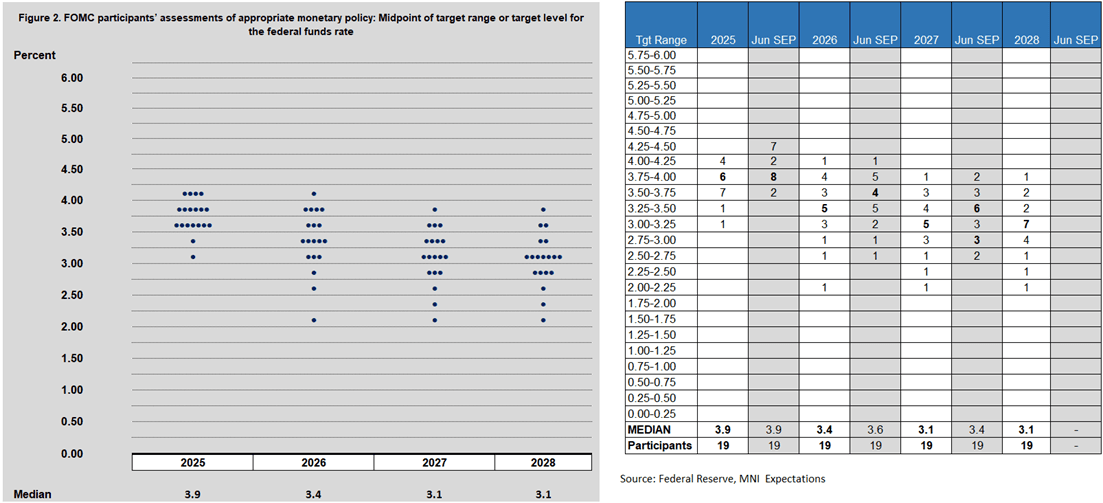

FED: September Dot Plot: Division Remains…At A Lower Level (1/2)

As always there will be interest in the updated Dot Plot at the September meeting. The MNI Markets Team anticipates a Dot Plot with a basically even split between two and three cut expectations for this year, similar to the June projections which showed a Committee essentially split between zero cuts and two cuts the rest of the year.

- This would signal that the FOMC’s median member is still looking for 2 total cuts this year, unchanged from June, with many amenable to 3 cuts, implying further easings in October and December, depending on how the data develops. A more awkward Dot Plot would have a wide dispersion of projections that show several members seeing no further cuts, with a growing vocal minority pushing for a more aggressive front-loaded easing.

- Going through the main considerations for the new Dot Plot:

2025: The end-year median is expected to either remain at June’s level of 3.9%, representing one further cut (assuming a 25bp cut in September), or fall to 3.6%. MNI’s Markets Team expects 3.9% in a very split decision between the two that tilts toward the more conservative side, with 10 dots at zero/one further cuts, and 9 seeing two or more further cuts.

- Put another way, in June, 9 participants saw rates ending the year above 4%; we expect that to be whittled down to 4, implying they see no further cuts the rest of the year. A plurality of 7 – probably including Fed Chair Powell and Board allies – will see 2 further cuts, while two dots below that could round it out, with one being Miran.

- Our Instant Answers will be watching the distribution of the 2025 dots.

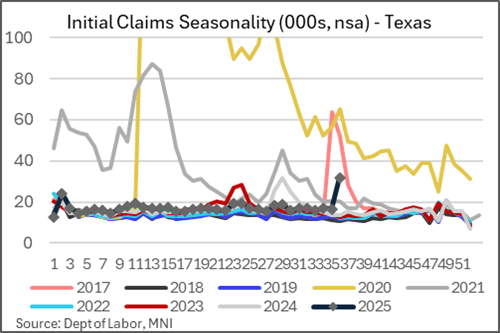

US LABOR MARKET: Texas Initial Jobless Claims Inflated By ... Fraud?

Last week's upside surprise to initial claims may be down to fraud.

- Recall initial jobless claims surprisingly jumped to 263k (sa, cons 235k) in the week to Sep 6. In the NSA jobless claims details, national claims increased 7.9k on the week but 15.3k of that came from Texas. It stood out significantly compared to recent years (see chart), with some (including MNI) initially concluding it may have been due to summer floods (for which unemployment claims had to be filed by Sep 4, though that's been extended).

- But there was a major twist yesterday, with the Texas Workforce Commission that reports the claims data saying (cited by Axios): "The increase in initial claims for unemployment insurance in the week ending September 6th is directly related to an increased volume of fraudulent claim attempts...Since Labor Day, we've observed an uptick in identity (ID) fraud claim attempts aimed at exploiting the unemployment insurance system."

- Axios writes: "The Labor Department did not respond to questions about whether Texas communicated that the fraud issue inflated its claims — and if so, why it was not flagged in the public release."

- This of course calls into question the national figure, which now will probably be disregarded as a nascent sign that the labor market continued to notably weaken in early September. The Texas numbers (and revisions) will be under special scrutiny in upcoming releases, of course.