MNI ASIA MARKETS ANALYSIS: Stocks Surge to New Record Highs

HIGHLIGHTS

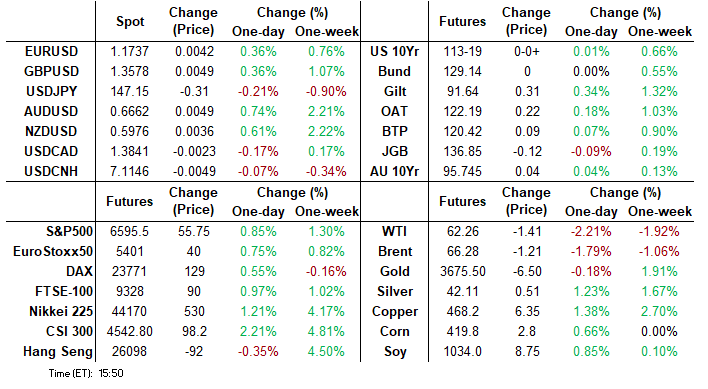

- Treasuries gapped higher early Thursday after CPI inflation data came out largely in-line with expectations while weekly claims surprised to the upside.

- Dovish reaction in rates saw projected rate cut pricing into year end rise to near cycle highs with nearly -75bp in cuts priced in by year end.

- The USD Index traded weaker into the Thursday close. While August CPI data came in alongside expectations, it was the particularly poor weekly jobless claims numbers that drove the price lower.

- US Equity indexes all climbed to new record highs Thursday, partially driven by the aforementioned rise in projected rate cut pricing in rates, Health Care, Financials and Consumer Discretionary sector shares led gainers.

US TSYS

MNI US TSYS: Strong Dovish Data React Lifts Projected Rate Cut Pricing

- Treasuries look to finish higher Thursday, off early post-data highs on heavier two-way flow. Treasury futures extended lows briefly (TYZ5 113-09) before rebounding / gapping higher post data: slightly higher than expected August CPI MoM inflation, while weekly claims come out much higher than expected.

- Core goods prices accelerated to 0.28% M/M from 0.21% prior, a little shy of expectations of a rise to the low 0.30s. This slight "miss" appears down to used car prices on the soft side of expectations at 1.0% M/M, still a 7-month high but vs expectations of a little above that figure.

- Initial jobless claims surprisingly jumped to 263k (sa, cons 235k) in the week to Sep 6 after a slightly downward revised 236k (initial 237k). Note that in the NSA jobless claims details, national claims increased 7.9k on the week but 15.3k of that came from Texas. Continuing claims on the other hand surprised lower at 1939k (sa, cons 1950k).

- Currently, the Dec'25 10Y trades +4 at 113-22.5 (yld 4.00547% -.0401) vs. 113-29 high - through initial technical resistance at 113-21.5 (High Sep 5) and 113-26.5 (2.764 proj of the Jul 15 - 22 - 28 price swing). Next level round number resistance at 114-00.

- Projected rate cut pricing gained traction vs. morning/pre-data levels (*): Sep'25 at -27.2bp (-27.1bp), Oct'25 at -50.1bp (-46.4bp), Dec'25 at -73.2bp (-68bp), Jan'26 at -86.1bp (-80.4bp).

- Focus Friday shifts to the UK activity data, in which markets expect both industrial and manufacturing production to slow on a monthly and yearly basis - underscoring a slower level of monthly GDP growth into Q3. French and German inflation numbers are also due, but it's the prelim University of Michigan sentiment numbers that should prove more decisive.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.39% (-0.01), volume: $2.800T

- Broad General Collateral Rate (BGCR): 4.37% (-0.01), volume: $1.145T

- Tri-Party General Collateral Rate (TCR): 4.37% (-0.01), volume: $1.118T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $111B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $209B

FED Reverse Repo Operation

RRP usage slips to $26.897B with 15 counterparties this afternoon from $29.400B Wednesday. Compares to $17.923B on Wednesday, Sep 3 - the lowest levels since early April 2021. This year's high usage of $460.731B occurred on June 30.

US SOFR/TREASURY OPTION SUMMARY

Pick-up in SOFR & Treasury option volume on two-way flow, better upside call structures gave way to puts as underlying futures retreated from post-CPI/weekly claims highs. Projected rate cut pricing gained traction vs. morning/pre-data levels (*): Sep'25 at -27.2bp (-27.1bp), Oct'25 at -50.1bp (-46.4bp), Dec'25 at -73.2bp (-68bp), Jan'26 at -86.1bp (-80.4bp).

SOFR Options:

+16,000 SFRV5/SFRX5/SFRZ5 96.25/96.43/96.62 call fly strip, paying 20-22 for package

+5,000 SFRZ5 95.81/95.93/96.06 put flys, 0.75

+10,000 SFRZ5 96.50/96.62 call spds, 2.5

+7,500 3QH6 96.25/97.25 call over risk reversals, 2.0

+4,000 SFRV5 96.31/96.43/96.50 put tree, 1.0 ref 96.39

+4,000 0QZ5 96.25/96.75 put spds 4.0

+2,000 SFRM6 97.25/98.00 call spd w/ SFRU6 97.50/98.12 call spd strip, 20.5

-5,000 SFRU5 95.75/95.87/96.00 call flys, 1.75 ref 95.9875

12,500 SFRU5 95.87 calls

-5,000 SFRU5 96.00/96.12/96.25 call flys, 1.75 - ongoing sale/unwind

-6,000 SFRU 95.93/96.00/96.06/96.12 call condors 4.0 ref 95.985

-5,000 SFRM6 96.00/96.25 put spds, 8.0 ref 96.385

+10,000 SFRZ5 96.50 calls, 8.0 ref 96.405

4,000 SFRZ5 95.87/96.00/96.12 put flys ref 96.33

Block: 9,000 SFRH6 96.12/96.37 put spd vs. 96.75/97.00 call spd, 1.0 net/put spd over

12,800 SFRU5 95.75/95.87/96.00 put flys, ref 95.9675

8,290 SFRU5 95.75/95.87/96.00 put flys ref 95.9675

3,300 SFRM5 96.00/96.50 put spds ref 96.825

3,750 SFRV5 96.18/96.25/96.31 put trees vs. 0QU5 96.87/97.12 strangles

11,000 SFRZ5 96.00/96.12/96.25/96.37 call condors ref 96.335

5,000 SFRU5 96.12 calls, 0.75 last ref 95.9675 to -.97

+2,500 SFRZ5 96.18/96.37/96.50 broken put trees. 3.5 ref 96.34

-5,000 SFRZ5 96.25/96.37 put spds, 5.5 ref 96.335

+5,000 0QU5 97.12 calls, 1.0

+4,000 0QU5 96.93 puts, 2.0 ref 96.995

-10,000 SFRU5 96.00/96.12/96.25 call flys, .5 ref 95.97

-2,000 SFRH6 96.37 puts, 11..0 vs. 96.555/0.34%

Treasury Options:

+50,000 USV5 111.5 puts, 1

-24,000 TYZ5 112.5/115 strangles, 105

11,790 USX5 106 put vs. USZ5 110 put, 14 net/Dec over

4,850 TYV5 108/110.75 2x1 put spds ref 113-21.5

2,800 USV5 112/118/121 broken call flys ref 117-26

4,000 TYX5 116/116.5 call spds ref 113-23.5

3,000 FVZ5 108.5 puts, ref 109-25.5

8,300 TYX5 115 calls vs. 111.5/112.5 put spds ref 113-12.5

+3,500 Thu wkly TY 113/113.25 put spds, 5 ref 113-10/0.05%

9,000 TYX5 115 calls vs. 111.5/112.5 put spds, 3 net

1,200 wk3 TY 112.5/113.5 put spds vs. 114.5 calls (exp 09/19)

3,000 FVV5 109.5 puts, 11-9 vs. 109-26/0.09%

+3,000 TYV5 113.5 straddles, 63 vs. 113-11.5 to -10/0.08%

1,000 USV5 118.5/119/119.5 call flys ref 117-05

10,000 TYV5 116 calls ref 113-14.5, 2 last

over 5,200 TYV5 115 calls 5 last

MNI BONDS: EGBs-GILTS CASH CLOSE: Bunds Underperform With ECB Seen Slightly Hawkish

European curves flattened Thursday.

- US CPI data came in on the slightly high side of expectations, but with relatively benign PCE inflation details combined with above-expected jobless claims released simultaneously, global core FI gained ground.

- The main event of the European session was the ECB meeting - MNI's review is here (PDF).

- In short, the bar to cuts was seen to have been raised a little: Lagarde's press conference sparked a hawkish reaction with growth risks deemed more balanced and the disinflationary process over.

- Later in the session, ECB sources from Bloomberg suggested further shocks are needed to see rate cuts. Reuters sources said the debate on a rate cut was not over just yet with October too soon but December eyed.

- On net, the German curve closed with twist flattening on the day as the short-end was notably weaker; Gilts easily outperformed, with bull flattening in the UK curve.

- Periphery/semi-core EGBs tightened amid the weakness in Bunds, with BTPs and OATs outperforming.

- UK activity data features first thing Friday, while multiple ECB speakers make appaearances (Rehn, Nagel, Kocher).

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 3.4bps at 1.986%, 5-Yr is up 3.2bps at 2.257%, 10-Yr is up 0.5bps at 2.657%, and 30-Yr is down 1.8bps at 3.255%.

- UK: The 2-Yr yield is down 0.9bps at 3.931%, 5-Yr is down 1.2bps at 4.043%, 10-Yr is down 2.7bps at 4.606%, and 30-Yr is down 4.4bps at 5.438%.

- Italian BTP spread down 2bps at 79.5bps / French OAT down 2.1bps at 78.8bps

MNI FOREX: EUR/USD Surges on Soft US Jobs, Hesitant Lagarde

- The USD Index traded weaker into the Thursday close. While August CPI data came in alongside expectations, it was the particularly poor weekly jobless claims numbers that drove the price lower. The USD Index sales came across several phases through Thursday trade, with price action getting a further boost on the core equity rally.

- The e-mini S&P rallied alongside spot gold prices - both gaining as markets cemented expectations for outsized easing at the September FOMC meeting. OIS markets retain full pricing for a 25bps rate cut next week, with partial pricing still pointing to a decent chance of a 50bps move.

- EURUSD gained ground throughout the ECB press conference, breaking the Thursday highs at 1.1738 amid a hawkish-leaning Lagarde as well as the soft jobs data. Lagarde's key press conference signals include her statement that the risks to Eurozone economic growth have become "more balanced" (she previously had noted downside risks), as well as the phrase that "the disinflationary process in Europe is over". These underpinned a hawkish adjustment in EUR STIR.

- Focus Friday shifts to the UK activity data, in which markets expect both industrial and manufacturing production to slow on a monthly and yearly basis - underscoring a slower level of monthly GDP growth into Q3.

- French and German inflation numbers are also due, but it's the prelim University of Michigan sentiment numbers that should prove more decisive. Markets expect the one- and 5-10 year inflation expectation metrics to slow by 0.1 ppts apiece ahead of next week's FOMC decision.

MNI OPTIONS: Expiries for Sep12 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1550(E1.7bln), $1.1600(E1.1bln), $1.1650(E1.6bln), $1.1670-75(E1.8bln), $1.1700(E2.8bln), $1.1724-35(E1.9bln) $1.1800(E1.5bln), $1.1850(E1.4bln)

- USD/JPY: Y146.00($1.1bln), Y147.25($616mln), Y147.40-50($2.9bln), Y150.00($698mln), Y151.00($1.1bln)

- EUR/GBP: Gbp0.8725(E604mln)

- AUD/USD: $0.6570-90(A$1.6bln)

MNI US STOCKS: Late Equities Roundup: Up, Up & Away - Extending New Record Highs

- Major equity indexes extended their climb to new record highs late Thursday, supported in large part by a dovish reaction to this morning's data - more or less in-line CPI inflation and higher than expected weekly claims - that buoyed projected rate cut pricing into year end.

- Currently, the DJIA trades up 610.71 points (1.34%) at 46106.55 vs. 46129.84 record high, S&P E-Minis up 51.25 points (0.78%) at 6591 vs. 6595.0 record high, Nasdaq up 156.7 points (0.7%) at 22041.16 vs. 22048.65 record high.

- A combination of Health Care, Financials and Consumer Discretionary sector shares led gainers in late trade.

- Managed care provider Centene Corp led gains in the Health Care sector - rising +11.64%, followed by Molina Healthcare +6.29%, Moderna +5.31% and AbbVie +4.02%.

- The Financials sector was buoyed by KKR & Co +4.24%, Blackstone +3.39%, Blackrock +3.09% and Apollo Global Management +2.91%.Meanwhile, cruise lines rebounded from early week selling: Norwegian Cruise Line +5.82%, Tesla +5.29%, Carnival +4.32% and Royal Caribbean +3.66%.

- On the flipside, IT, Communication Services and Energy sector shares led decliners in late trade: Oracle Corp -5.84%, Netflix -4.30%, Broadcom -2.42%, Vistra -2.38% and Teradyne -2.32%.

- Energy stocks retreated as oil prices halted four consecutive session gains (WTI -1.29 at 62.38): APA Corp -1.37%, Expand Energy -0.86%, Diamondback Energy -0.84%, Devon Energy -0.73% and ConocoPhillips -0.61%.

MNI EQUITY TECHS: E-MINI S&P: (U5) Bulls Remain In the Driver’s Seat

- RES 4: 6673.37 2.236 proj of the May 23 - Jun 11 - 23 price swing

- RES 3: 6623.57 2.0% 10-dma envelope

- RES 2: 6600.00 Round number resistance

- RES 1: 6595.00 High Sep 11

- PRICE: 6590.25 @ 1424 ET Sep 11

- SUP 1: 6469.93 20-day EMA

- SUP 2: 6372.16 50-day EMA

- SUP 3: 6313.25 Low Aug 6

- SUP 4: 6239.50 Low Aug 1 and a key support

A bull cycle in S&P E-Minis remains intact and the latest pullback has once again proved to be a shallow correction. The contract traded to a fresh cycle high on Wednesday, breaching the Sep 5 high of 6541.75. This confirms a resumption of the uptrend and maintains the price sequence of higher highs and higher lows. Sights are on the 6600.00 handle next. Initial support to watch is 6469.93, the 20-day EMA.

MNI COMMODITIES: Crude Pulls Back, Gold Edges Lower

- WTI has pulled back today as the market weighs expectations of increased October supply and future surpluses against geopolitical developments.

- WTI Oct 25 is down by 2.1% at $62.3/bbl.

- Saudi Arabia’s oil exports are set to jump this month as the twin impact of higher production and easing local demand from peak summer levels frees up supply, Bloomberg reports.

- The global oil market is caught in a “tug-of-war between increasingly bearish fundamentals and heightened geopolitical risks,” according to Citigroup.

- From a technical perspective, a bear cycle in WTI futures remains intact, with initial support at $61.29, the Aug 13 low and the bear trigger. A clearance of this level would pave the way for a move towards $57.71, the May 30 low.

- Initial resistance to watch is $66.03, the Sep 2 high.

- Meanwhile, spot gold has edged down by 0.2% to $3,632/oz, as the yellow metal consolidates recent gains which saw it trade at an all-time high of $3,674.27 earlier this week.

- Bloomberg reports that this week’s gains also took bullion to a record high on an inflation adjusted basis, taking it above the previous January 1980 peak.

- Gold remains in a clear bull cycle, with the next objective seen at $3,674.8, a Fibonacci projection, followed by $3,700 round number resistance.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 12/09/2025 | 0600/0700 | *** | UK Monthly GDP | |

| 12/09/2025 | 0600/0700 | ** | Trade Balance | |

| 12/09/2025 | 0600/0700 | ** | Index of Services | |

| 12/09/2025 | 0600/0700 | ** | Index of Production | |

| 12/09/2025 | 0600/0800 | *** | Germany CPI (f) | |

| 12/09/2025 | 0600/0700 | ** | Output in the Construction Industry | |

| 12/09/2025 | 0600/0800 | *** | Germany CPI (f) | |

| 12/09/2025 | 0645/0845 | *** | HICP (f) | |

| 12/09/2025 | 0700/0900 | *** | HICP (f) | |

| 12/09/2025 | 0830/0930 | ** | Bank of England/Ipsos Inflation Attitudes Survey | |

| 12/09/2025 | 0900/1100 | Labour Market Quarterly Statistics | ||

| 12/09/2025 | - | *** | Money Supply | |

| 12/09/2025 | - | *** | New Loans | |

| 12/09/2025 | - | *** | Social Financing | |

| 12/09/2025 | 1230/0830 | * | Building Permits | |

| 12/09/2025 | 1400/1000 | * | Services Revenues | |

| 12/09/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 12/09/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 12/09/2025 | 1600/1200 | *** | USDA Crop Estimates - WASDE | |

| 12/09/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 12/09/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |