MNI ASIA MARKETS ANALYSIS: Stocks Retreat on Late Earnings

HIGHLIGHTS

- Treasuries reversed reversed early Thursday morning gains, extended lows into late trade after mostly higher than expected ISMs: Mfg, New Orders & Employment, while Prices Paid comes out less than expected.

- ISMs was a very weak report that is consistent with recessionary conditions in the manufacturing sector amid policy uncertainty and a giveback of tariff-front loading production in Q1.

- Curves bear flattened off this morning's steeper levels, moves partially tied to unwinds of month end extensions. Focus turns to Friday morning's April employment data.

- Late stock retreat to only mildly higher after Amazon, Eli Lilly & Becton Dickinson sell off.

US TSYS

MNI US TSYS: Late Stock Retreat, Join Treasuries, Focus on Earnings, Jobs

- US Treasuries are broadly weaker after the bell (late stock retreat to only mildly higher after Amazon, Eli Lilly & Becton Dickinson sell off), near late session lows as focus turns to Friday morning's April employment report. Volatile early trade as markets reacted more to economic data than trade related headlines.

- Treasuries extended early highs after higher than expected weekly and continuing claims, prior for continuing down-revised. Initial jobless claims increased to 241k (sa, cons 223k) in the week to Apr 26 after a marginally upward revised 223k (initial 222k).

- Rates reversed course, extended lows while stocks rallied - caveats to higher than expected ISM New Orders & Employment data as markets apparently overlooked (very weak report that is consistent with recessionary conditions in the manufacturing sector amid policy uncertainty and a giveback of tariff-front loading production in Q1.)

- Tsy Jun'25 10Y currently 9.5 at 111-29.5 vs. 111-24.5 low (10Y yld climbs to 4.2388% high), technical support well below at 111-07.5 (20-day EMA).

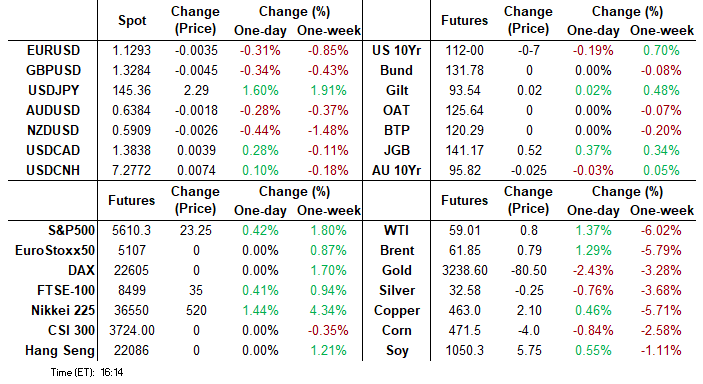

- US$ gained (BBDXY +6.09 at 1229.69) , while Gold sold off sharply (-60.63 at 3228.08). Note: Stocks pared gains into the close, finishing mildly higher: SPX eminis +22. at 5609.25.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.41% (+0.05), volume: $2.830T

- Broad General Collateral Rate (BGCR): 4.37% (+0.02), volume: $1.088T

- Tri-Party General Collateral Rate (TCR): 4.37% (+0.02), volume: $1.047T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $92B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $215B

FED Reverse Repo Operation

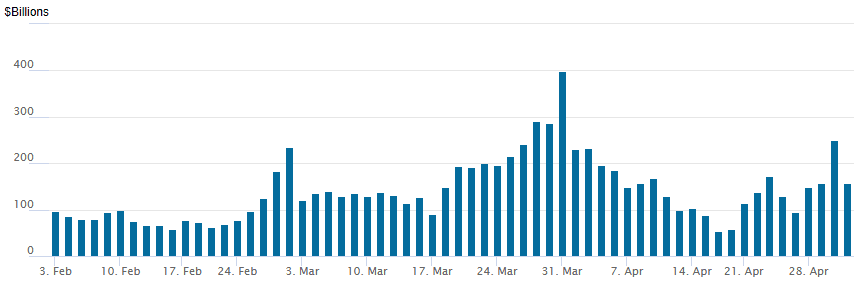

RRP usage retreats back to $157.353B this afternoon from $250.601B yesterday. Usage had fallen to $54.772B last Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B. The number of counterparties at 37.

US SOFR/TREASURY OPTION SUMMARY

Option desks reported better SOFR & Treasury put options on net Thursday. Underlying futures weaker, near recent lows (TYM5 -11.5 at 111-27.5 vs. -24.5 low) in the lead up to Friday's employment data. Curves reversed course, look flatter after the bell (2s10s -3.258 at 52.253, 5s30s -2.733 at 92.194). As such, projected rate cut pricing has cooled significantly vs. this morning's levels (*) as follows: May'25 at -1.8bp (-2.1bp), Jun'25 at -14.6bp (-17.7bp), Jul'25 at -35.8bp (-42.3bp), Sep'25 -56.8bp (-65.7bp).

SOFR Options:

+3,000 0QM5 96.50/96.75 2x1 put spds 2.5

+10,000 0QK5 96.62/96.75/96.93 put flys, 4.25

+10,000 SFRK5 95.87/95.93/96.00/96.12 broken call condor, 0.5 ref 95.935

-15,000 0QU5 97.12 calls, 33.0-32.5 ref 97.105

+20,000 0QK5 96.62 puts, 1.5 ref 97.05

2,000 SFRZ5 95.87 put vs. 96.75/97.00 call spds x2

Block, 5,000 SFRK5 95.75/95.81 put spds, 1.0 ref 95.925

15,000 SFRZ5 95.68/95.93 put spds ref 96.715

Block, 3,000 SFRM5 95.75/95.93 put spds 10.5 vs. 95.895/0.10%

2,000 SFRU5 95.87 puts ref 96.365

Block, 3,450 SFRN5 96.50/96.75 call spds vs. 96.37/0.13%

4,000 SFRU5 95.68/95.87/96.00 broken put flys ref 96.365

1,500 0QK5 96.81/96.87/97.00 broken put flys ref 97.035

1,500 0QM5 96.75/2QM5 96.75/3QM5 96.62 1x1x2 put trees vs. 2,500 0QH6 95.00 puts

2,000 0QK5 96.62/96.87 2x1 put spds ref 97.03

Treasury Options:

over +10,000 wk2 TY 110.5/111.5 3x2 put spds, 24 ref 112-02.5 (exp May 9)

2,000 FVM5 108/108.25/108.75 broken put trees

+10,000 Mon wkly FV 108.5 puts, 2.5

1,200 USN5 112/115 2x1 put spds, 15 net ref 115-25

+8,800 TYM5 111 puts, 16

1,300 FVM5 110.75 calls, ref 109-12.75

1,000 TYN5 114/116/117 broken call flys ref 112-21

MNI BONDS: EGBs-GILTS CASH CLOSE: Gilts Bear Steepen With EGBs On Holiday

Gilt yields rose sharply Thursday, with EGB trade closed for the May 1 European holiday.

- With much of Europe off, market focus was entirely on the UK.

- Gilts traded steadily through the morning session, with the short end outperforming as oil prices receded, and ticking higher on higher-than-expected US jobless claims data,

- But they turned sharply lower two hours before the cash close as the US ISM Manufacturing index was not as bad as feared.The selloff accelerated into the cash close, led by Treasuries.

- UK data included March lending data which showed a burst of mortgage loans (front-running the expiry of a stamp duty cut), while final April manufacturing PMI was slightly upgraded from the preliminary reading but remained contractionary.

- The UK curve bear steepened: The 2-Yr yield is up 1.8bps at 3.821%, 5-Yr is up 2.6bps at 3.943%, 10-Yr is up 4bps at 4.481%, and 30-Yr is up 5.3bps at 5.26%.

- Friday's calendar is highlighted by Eurozone flash April inflation (recall, national data so far suggests upside risks to consensus for core HICP coming into the week).

MNI EGB OPTIONS: Sonia Structures Predominant With Much Of Europe On Holiday

Thursday's Europe rates/bond options flow included:

- SFIZ5 96.45/96.55cs with 96.50/96.50cs strip, sold at 9 in 7.5k

- SFIZ5 96.00/95.90/95.75p fly, bought for 2.5 in 2k

MNI FOREX: USDJPY Extends Surge Amid Dovish BOJ and Equities Rally

- Despite the plethora of national holidays on Thursday, currency markets have seen significant swings, with the USD index (+0.78%) notably extending its recovery to trade back above the 100 mark ahead of Friday’s US employment report. The yen has significantly underperformed following a dovish tilt from the Bank of Japan and higher US yields/equities providing additional headwinds.

- As such, USDJPY stands 1.65% firmer on the session having extended a clean break of the recovery highs around the 144 handle. The move coincided with a breach of the 20-day EMA which may have also exacerbated the topside momentum. Highs approaching the APAC crossover are seen at 145.65, and represent a 280 pip rally from session lows. Firmer resistance is located at the 50-day EMA, intersecting at 146.72.

- Elsewhere, losses across the G10 space have been broad based against the dollar. The likes of EUR and GBP are roughly half a percent lower, back below 1.13 and 1.33 respectively.

- The recent pullback in EURUSD is considered corrective and the trend structure is unchanged, it remains bullish. Moving average studies are in a bull-mode position signalling a dominant uptrend, and the latest move down is allowing an overbought condition to unwind. Key support is at the 20-day EMA, at 1.1251.

- USDCHF has also strengthened 0.75% today, with the highs of the session once again coinciding with the 2023 breakdown point at 0.8333, and the 20-day EMA. This could increase the pair’s importance ahead of Friday’s release of the US employment report. Elsewhere, flash inflation data for the Eurozone is a calendar highlight on Friday.

MNI FX OPTIONS: Expiries for May02 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1150(E897mln), $1.1290-00(E1.0bln), $1.1370-85(E1.2bln)

- USD/JPY: Y144.63-65($629mln), Y145.00($609mln), Y146.00($778mln)

- AUD/USD: $0.6450(A$729mln), $0.6550(A$803mln)

- NZD/USD: $0.5970-80(N$665mln)

- USD/CAD: C$1.3825($598mln), C$1.3895-00($1.1bln)

MNI US STOCKS: Late Equities Roundup: Software & Services, Interactive Media Leading

- Stocks are see-sawing in decently higher territory late Thursday after trimming gains around midday, Information Technology and Communication Services sectors continue to outperform. Currently, the DJIA trades up 239.81 points (0.59%) at 40909.95, S&P E-Minis up 71.5 points (1.28%) at 5658.5, Nasdaq up 375.1 points (2.2%) at 17822.34.

- Information Technology and Communication Services sectors continued to lead in late trade, software and services outpaced chip makers: Microsoft +8.97%, Arista Networks +7.80%, Oracle +3.71%, NVIDIA +4.34%, Broadcom +4.27% while Super Micro Computer bounced 5.73% after Wednesday’s sharp sell-off.

- Interactive media & entertainment shares buoyed the Communications sector: Meta Platforms +5.29%, Match Group +2.53% and Alphabet +1.77%.

- Conversely, Health Care and Consumer Staples sectors underperformed in the first half: Becton Dickinson -15.79% after potential tariffs said to curtail profit outlook, Eli Lilly -9.37%, Moderna -3.21%, GE HealthCare Technologies -3.2%.

- Meanwhile, Church & Dwight -6.96%, Dollar General -4.34%, Estee Lauder Cos -2.55% and Clorox -2.47% weighed on the Consumer Staples sector.

MNI EQUITY TECHS: E-MINI S&P: (M5) Tops 50-Day EMA

- RES 4: 5837.25 High Mar 25 and a bull trigger

- RES 3: 5774.43 200-dma

- RES 2: 5773.25 High Apr 2

- RES 1: 5662.25 High Apr 28

- PRICE: 5655.00 @ 1510 ET May 1

- SUP 1: 5355.25/5127.25 Low Apr 24 / 21 and a key support

- SUP 2: 4996.43 76.4% retracement of the Apr 7 - 10 bounce

- SUP 3: 4832.00 Low Apr 7 and the bear trigger

- SUP 4: 4760.88 1.618 proj of the Feb 19 - Mar 13 - 25 price swing

The recovery in the e-mini S&P continues, with a ninth consecutive session of higher highs - the longest winning streak of the year so far, underpinning the short-term positive momentum for stocks. The bull cycle that started on Apr 7, remains in play and has breached a number of important short-term resistances. The index has topped 5618.25, the 50-day EMA, opening layered resistance at 5773.25-5774.43

MNI AMERICAS OIL: WTI crude has reversed earlier ~2% losses and moved higher

May 1 - Americas End-of-Day Oil Summary: WTI crude has reversed earlier ~2% losses and moved higher on the day, with signs of delayed US-Iran talks supportive. Rising expectations of a further sizeable OPEC+ production hike in June and global demand concerns continue have added pressure in recent days. Trump posted on Truth Social late in the session taking a tough stance on buyers of Iranian oil.

- The US-Iran meeting provisionally planned for Saturday May 3rd has been rescheduled according to Qatari officials.

- The US and Ukraine have signed a minerals deal today. US Treasury Secretary Bessent said that the deal will allow Trump to negotiate with Russia on a stronger basis.

- Saudi Arabia is not overly concerned about lower prices suggesting that it may focus on market share instead, Reuters said.

- WTI June futures were up 1.8% at $59.24

- WTI July futures were up 1.9% at $58.69

- RBOB Jun futures were up 1.7% at $2.05

- ULSD Jun futures were up 0.6% at $2.01

- US gasoline crack up 0.3$/bbl at 26.86$/bbl

- US ULSD crack down 0.8$/bbl at 25.29$/bbl

FRIDAY DATA OUTLOOK

| Date | GMT/Local | Impact | Country | Event |

| 02/05/2025 | 0630/0730 | DMO to announce details of long syndication for W/C 19 May | ||

| 02/05/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (f) | |

| 02/05/2025 | 0745/0945 | ** | S&P Global Manufacturing PMI (f) | |

| 02/05/2025 | 0750/0950 | ** | S&P Global Manufacturing PMI (f) | |

| 02/05/2025 | 0755/0955 | ** | S&P Global Manufacturing PMI (f) | |

| 02/05/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (f) | |

| 02/05/2025 | 0900/1100 | *** | HICP (p) | |

| 02/05/2025 | 0900/1100 | ** | Unemployment | |

| 02/05/2025 | 1130/2030 | * | Labor Force Survey | |

| 02/05/2025 | 1230/0830 | *** | Employment Report | |

| 02/05/2025 | 1400/1000 | ** | Factory New Orders | |

| 02/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 02/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |