OPTIONS: Expiries for May02 NY cut 1000ET (Source DTCC)

May-01 13:59

- EUR/USD: $1.1150(E897mln), $1.1290-00(E1.0bln), $1.1370-85(E1.2bln)

- USD/JPY: Y144.63-65($629mln), Y145.00($609mln), Y146.00($778mln)

- AUD/USD: $0.6450(A$729mln), $0.6550(A$803mln)

- NZD/USD: $0.5970-80(N$665mln)

- USD/CAD: C$1.3825($598mln), C$1.3895-00($1.1bln)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

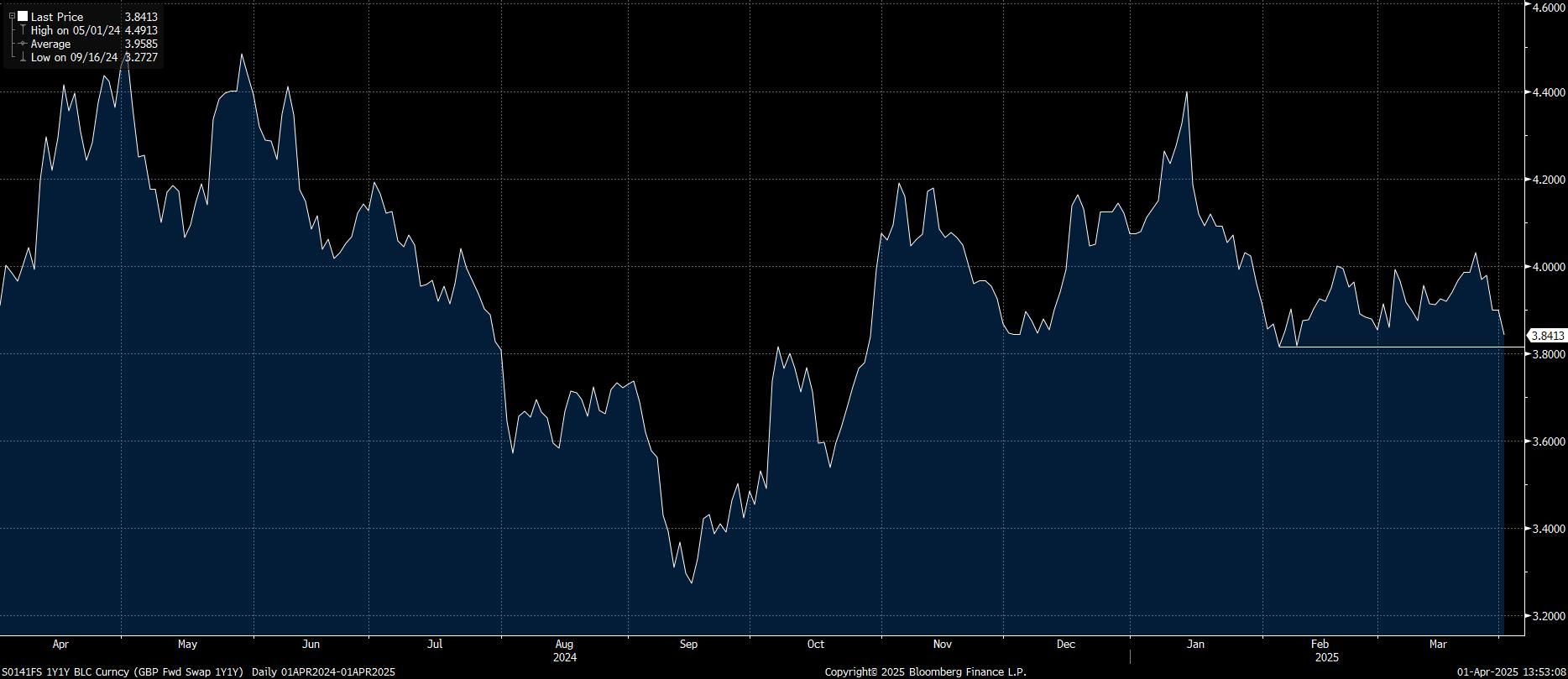

STIR: GBP 1y1y Eyes Feb Lows

Apr-01 13:57

Spillover from the move lower in core global yields ahead of “Liberation Day” leaves GBP 1y1y on track to register the first close below 3.85% since February.

- The February closing low/double bottom support area (3.8145%) presents the next notable downside level of interest.

Fig. 1: GBP 1y1y Swap

Source: MNI - Market News/Bloomberg

US TSYS: Post-S&P Global US Manufacturing PMI React

Apr-01 13:56

- Treasuries paring gains slightly, still holding higher range after mildly higher than expected S&P Mfg PMI data, stocks pare losses (SPX eminis -5.00 at 5648.25).

- Tsy Jun'25 10Y contract trades 111-18.5 (+11.5), off earlier high of 111-27.5, next technical resistance at 112-01 (High Mar 4 and a bull trigger).

- Curves continue to bull flatten off early week highs: 2s10s -2.694 at 29.105, 5s30s -1.852 at 60.088.

- Cross asset update, Bbg US$ index +.95 at 1275.20, Gold making new highs around 3135.0, crude adding to Monday's rally (WTI +.34 at 71.82.).

- Next up: JOLTS, Construction Spending and ISM mfg data at 1000ET.

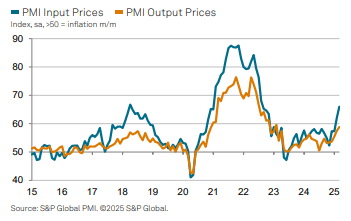

US DATA: PMI Mfg Orders Slow, Input Cost Inflation Highest In 2.5 Years

Apr-01 13:55

- The manufacturing PMI was revised up slightly in the March final release to 50.2 (cons 49.9, flash 49.8), although still sees a sizeable decline from 52.7 in February (highest since Jun 2022).

- The press releases summarizes the report as: “Production declines in March as order book growth slows on tariff uncertainty”

- It also confirms strong input cost inflation indicated in the flash release, at its highest in “over two-and-a-half years”. The flash release, for both manufacturing and services, had noted that “Input price inflation accelerated sharply, especially in manufacturing, to a near two-year high, often attributed to the impact of tariff policies. However, competition limited the pass-through of higher costs to selling prices.” Here, specifically for manufacturing, output price inflation increased to a 25-month high.

Some highlights from the full press release (here):

- “US manufacturing sector growth stalled in March. Having grown strongly in February, production declined as order books expanded only modestly despite evidence of a stabilization of exports.

- Confidence in the outlook for business activity softened, amid some uncertainty over the impact of federal government policies.

- Employment numbers were unchanged after four months of job gains. Softer trends in output and new orders, plus uncertainty in the outlook, weighed on hiring decisions.

- Cost pressures intensified, largely due to the impact of tariffs, with input price inflation rising to its highest level in over two-and-a-half years.”

- Further on prices: “The steep increase in input prices fed through to a greater rise in manufacturing selling prices during March. Latest data showed that output price inflation picked up for a fourth successive month to a 25-month high.”