MNI ASIA MARKETS ANALYSIS: Shifting Risks, Rate Cut Pricing Up

HIGHLIGHTS

- Treasury futures gap higher after Chairman Powell's Jackson Hole speech noted "shifting balance of risks may warrant adjusting policy" saw Sep-25 10Y trade up to 112-08 (+22.5).

- Powell: "while the labor market appears to be in balance, it is a curious kind of balance that results from a marked slowing in both the supply of and demand for workers.

- Projected rate cuts gained vs. early morning (*) levels: Sep'25 at -21.2bp (-16.9bp), Oct'25 at -34.1bp (-29.6bp), Dec'25 at -55.1bp (-47.7bp), Jan'26 at -68.6bp (-58.6bp).

- The USD sank sharply against all others on Friday, falling sharply following Powell's appearance at the Jackson Hole Policy Symposium, Bloomberg $ index, BBDXY fell to 1199.66 low, trades 1201.20 late (-9.72).

US TSYS

MNI US TSYS: Fed Chair Powell: Shifting Risks May Warrant Policy Adjustment

- Treasuries look to finish near session highs - after gapping higher following Fed Chairman Powell's dovish speech from the Jackson Hole, Wy symposium. Sep'25 10Y contract trades +19 at 112-04.5 after the bell vs. 112-08 high, 10Y yield -.0739 at 4.2537% vs. 4.2402% low.

- Technical resistance attention on 112-15+, the Aug 5 high and the bull trigger. Clearance of this hurdle would resume the uptrend and pave the way for a climb towards 112-23 initially, the May 1 high.

- The major near-term policy signal takeaway from Fed Chair Powell's Jackson Hole keynote (link) is that he only acknowledges that "with policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance", but also that the risks appear to have shifted since the July meeting ("The balance of risks appears to be shifting"), as "downside risks to employment are rising.

- Boston Fed President Collins: Sep cut not a done deal as "risks on the two sides have come into rough balance. So, that is a really complex context for monetary policy, when you could see the unemployment rate rising and you could see higher inflation. You know, my baseline is not one that is as concerned about inflation expectations rising at the moment. Earlier in the year I had more concerns about that.

- Focus in the coming week shifts to any further policy signaling from central bank officials at Jackson Hole. BoE's Bailey, ECB's Lagarde, BoJ's Ueda, Riksbank's Thedeen and several more FOMC members are in attendence - meaning it should be a busy weekend for central bank commentary.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.32% (+0.01), volume: $2.702T

- Broad General Collateral Rate (BGCR): 4.30% (+0.01), volume: $1.132T

- Tri-Party General Collateral Rate (TCR): 4.31% (+0.01), volume: $1.109T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $117B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $263B

FED Reverse Repo Operation

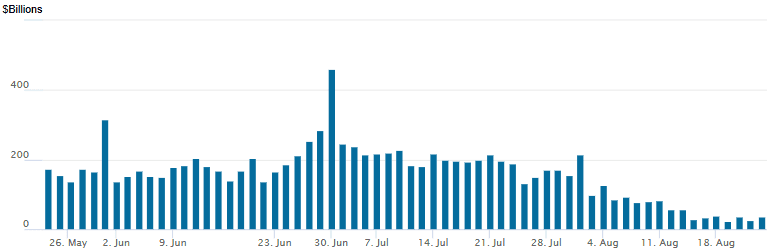

RRP usage rises to $36.275B this afternoon from $25.358B yesterday -- compares to $22.344B on Tuesday, Aug 19 - lowest since April 5, 2021. Total number of counterparties at 16. This week's retreat compares this year's high usage of $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury options continued to revolve around low delta/upside calls Friday, some profit taking/unwinds after the underlying surged higher following dovish comments from Fed Chair Powell at Jackson Hole symposium. Sep Tsy options expiring, pin risk evaporating as futures hold off strikes. Projected rate cuts gained vs. early morning (*) levels: Sep'25 at -21.2bp (-16.9bp), Oct'25 at -34.1bp (-29.6bp), Dec'25 at -55.1bp (-47.7bp), Jan'26 at -68.6bp (-58.6bp).

SOFR Options:

Block, 13,125 SFRU5 96.06/96.12 call spds 0.75 vs. 95.925/0.06%

+5,000 0QU5 97.00/97.50 call spds .5 over 2QU5 97.00/97.37 call spds

-17,000 SFRZ5 95.75 puts, 0.75 ref 96.235

+8,000 SFRH6 96.56/97.06 call spds .5 over 2QH6 97.00/97.50 call spds

-4,000 SFRH6 97.00 calls, 9.5 vs. 96.48/0.24%

-3,000 SFRVB5 96.00 puts, 2.0 ref 96.24

-3,000 SFRZ5 96.50 calls, 7.0 vs. 96.23/0.28%

Block, 5,000 SFRZ5 95.75 puts, 0.75

-4,000 SFRU5 95.87 calls, 7.0

-20,000 0QZ5 96.75/97.00/97.50/97.75 call condors 8.75-9.0 (adds to appr 10k yesterday)

over 15,000 SFRU5 95.81/95.87/96.00 call flys ref 95.855

over 10,000 SFRU5 95.68/95.75/95.81 put trees

2,000 SFRU5 96.00/96.12/96.25 call flys ref 95.855

7,800 SFRU5 96.12/96.25 call spds ref 95.8525

2,000 SFRZ5 95.93 puts ref 96.145

3,200 0QU5 96.62/97.00 strangles ref 96.78

3,200 SFRU5 96.06 calls

Treasury Options: Reminder Sep Tsy options expire today

+15,000 wk4 Mon TY 111.5 puts, cab-7 exp Mon

3,000 wk5 TY 112.5/113 2x1 put spds, 1 ref 112-05, exp 8/29

+67,000 TYV5 113.5 calls, 18 vs. 112-03/0.23%

over 3,400 TYU5 113 calls ref 111-17

1,000 FVU5 108.5/108.75 call spds ref 108-18.5

2,500 FVU5 108.5/109.25 call spds ref 108-19.5

MNI BONDS: EGBs-GILTS CASH CLOSE: Powell Ensures 10Y Yields Down On The Week

The highly-anticipated Jackson Hole speech by Federal Reserve Chair Powell brought a dovish message, spurring a rally across global FI Friday that included EGBs and Gilts.

- Bunds outperformed global peers in early trade, though moves were limited as markets awaited Powell's comments. German Q2 GDP was revised downward, with ECB Q2 negotiated wages broadly in line with tracking estimates.

- Yields dropped sharply in mid-afternoon trade as Powell signaled openness to a September Fed cut in more overt fashion than had been expected, noting a "shifting balance of risks may warrant adjusting our policy stance".

- Bund yields finished a little higher than the levels seen in the immediate aftermath of Powell's speech, but Gilt yields continued to fall, closing near session lows.

- A Bloomberg sources piece pointed to a September ECB hold, but markets took little impact with rate markets already pricing that in.

- The German and UK curves both bull flattened on the day, while periphery/semi-core EGB spreads tightened in a broader risk rally.

- For the week, the German curve bull flattened with the UK's twist flattening: UK 2Y +1.1bp, 10Y -0.3bp; German 2Y -2.5bp, 10Y -6.6bp.

- Saturday includes a panel at Jackson Hole with BOE's Bailey and ECB's Lagarde, with next week's calendar highlight being August flash Eurozone inflation data.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 2.4bps at 1.948%, 5-Yr is down 3.8bps at 2.277%, 10-Yr is down 3.5bps at 2.722%, and 30-Yr is down 1.8bps at 3.309%.

- UK: The 2-Yr yield is down 2.6bps at 3.944%, 5-Yr is down 2.3bps at 4.101%, 10-Yr is down 3.6bps at 4.693%, and 30-Yr is down 3bps at 5.548%.

- Italian BTP spread down 2bps at 80.4bps / French OAT down 1.2bps at 69.5bps

OPTIONS: Euribor Call Condors Closed, Sonia Call Fly Bought Pre-Jackson Hole

Friday's Europe rates/bond options flow included:

- OEV5 117.75/117.25ps 1x2, bought for 2.5 up to 3 in 3.5k

- RXV5 123p, bought for 2 in 7.2k

- ERU5 98.12/98.1875/98.25/98.3125c condor, sold at 0.25 in 20k (closing)

- SFIH6 96.20/96.30/96.40c fly vs 96.00/9590ps, bought the fly for half in 2k

MNI FOREX: USD Breaks To August Lows as Markets Resolve Around Sept Fed Cut

- The USD sank sharply against all others on Friday, falling sharply following Powell's appearance at the Jackson Hole Policy Symposium. In acknowledging that the balance of risks to the US economy has shifted, he signaling a much higher likelihood of a rate cut at the Fed's September meeting - helping OIS markets resolve pricing and send the dollar lower in the process. Immediate strength in EUR/USD put the pair through yesterday's highs to narrow the gap with 1.1693, the next upside level intraday. The move coincides with a firm rally for equities - putting the E-mini S&P within range of the weekly high at 6484.25.

- The price action was backed up by a follow-up claim from Trump that he will fire Fed's Cook should she not resign - adding to the evidence that Trump may look to build a corner of policymakers within the FOMC that favour his view of lower rates for the US economy. Rates markets built in expectations for not just a September rate cut, but additional easy policy into year-end - with over 50bps now well priced.

- Second to USD weakness, CAD also trade poorly as softer oil prices countered any bullish signal from slightly better-than-expected retail sales data as well as Carney's decision to unilaterally remove retaliatory tariffs against US imports. Gains this week in USDCAD and the breach of resistance at 1.3879, the Aug 1 high, marked a positive development, however the slippage into the Friday close undermines this sentiment - for now. Moving average studies have crossed and are in a bull-mode position, reinforcing current conditions. An extension higher would signal scope for a climb towards 1.4019, a Fibonacci retracement. On the downside, support to watch lies at 1.3769, the 50-day EMA - a level not yet challenged by the correction lower.

- Focus in the coming week shifts to any further policy signaling from central bank officials at Jackson Hole. BoE's Bailey, ECB's Lagarde, BoJ's Ueda, Riksbank's Thedeen and several more FOMC members are in attendence - meaning it should be a busy weekend for central bank commentary. A UK Bank Holiday should keep markets set for a quieter start to the week, but German IFO, US consumer confidence, Australian CPI and European inflation numbers are all due - as well as NVIDIA's earnings release.

MNI FX OPTIONS: Expiries for Aug25 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1550(E1.7bln), $1.1600(E806mln), $1.1640-55(E2.2bln), $1.1700(E961mln), $1.1780-85(E1.4bln)

- USD/JPY: Y147.00($878mln)

- AUD/USD: $0.6400(A$621mln), $0.6510-25(A$1.1bln)

- USD/CAD: C$1.3800($664mln)

MNI US STOCKS: Late Equities Roundup: Holding Record Highs in SPX & DJIA

- Stocks holding at/near new record highs late Friday -- surging higher after Fed Chair Powell intimated shifting risk profiles may warrant adjusting policy as he delivered a speech on the economy in Jackson Hole, Wy this morning.

- Risk appetites gathered momentum as the US$ fell back near last week's 3W lows (BBDXY -10.71 at 1200.21), 10Y Treasury yields -.0720 at 4.2557%, while projected rate cuts into year end approximately -56bp priced in by the December 10 meeting.

- The broad based rally saw the DJIA make new all-time high of 45,691.18 - well past prior high of 45,073.63 on December 4, '24, the SPX eminis neared last week's record high of 6,508.75 (Aug 15), while the Nasdaq neared last week's record high of 21,803.75 (Aug 13). Currently, the DJIA trades up 821.87 points (1.84%) at 45608.3, S&P E-Minis up 95.75 points (1.5%) at 6484, Nasdaq up 412.9 points (2%) at 21513.02.

- Consumer Discretionary, Communication Services and Energy sectors led gainers in the second half. Leading discretionary sector shares included: Mohawk Industries +7.17%, Norwegian Cruise Line +6.74%, Caesars Entertainment +6.30%, Carnival +6.25%, PulteGroup +5.78% and Tesla +5.71%.

- Communications leaders included Alphabet +4.06%, Charter Communications +3.50%, Warner Bros Discovery +3.50%, Walt Disney +2.35% and Meta Platforms +2.10%. Oil & gas stocks buoyed the Energy sector with: Schlumberger +4.41%, APA Corp +4.29%, Phillips 66 +4.15% and Halliburton +4.02%.

- Conversely, Consumer Staples, Utilities and Health Care sectors continued to underperform in late trade, decliners included: The Kroger Co -2.49%, Monster Beverage -2.28%, Costco Wholesale -1.51%; NRG Energy -0.62%, Constellation Energy -0.48% and CenterPoint Energy -0.45%; while McKesson Corp -2.94%, Cencora -2.74% and Cardinal Health -2.32%.

- Reminder, Nvidia is expected to announce their latest earnings next Wednesday after the close.

MNI EQUITY TECHS: E-MINI S&P: (U5) Corrective Pullback

- RES 4: 6600.00 Round number resistance

- RES 3: 6572.45 2.0% 10-dma envelope

- RES 2: 6523.63 1.764 proj of the May 23 - Jun 11 - 23 price swing

- RES 1: 6508.75 High Aug 15 and all-time High

- PRICE: 6487.00 @ 1505 ET Aug 22

- SUP 1: 6362.75 Low Aug 20

- SUP 2: 6313.25 Low Aug 6

- SUP 3: 6291.07 50-day EMA

- SUP 4: 6239.50 Low Aug 1

The dominant uptrend in S&P E-Minis remains intact and the latest retracement appears to be a correction - for now. Moving average studies are in a bull-mode position, highlighting a clear uptrend and positive market sentiment. A resumption of gains would pave the way for a climb towards 6523.63, a Fibonacci projection. On the downside, support to watch lies at 6291.07, the 50-day EMA.

COMMODITIES

MNI AMERICAS OIL: US Close Oil Summary: WTI Ticks Up

WTI has risen today as positive sentiment grows around US interest rate cuts following Powell speaking at Jackson Hole symposium. WTI ticked up further in US hours after comments from Trump that he will decide on Russia sanctions in the next two weeks if needed.

- WTI OCT 25 up 0.3% at 63.69$/bbl

- Baker Hughes oil rig count: 411 (-1) - down 72 rigs, or 14.9% on the year. This is the lowest level since mid-July, which itself was the smallest number of oil rigs since Oct. 2021

- Trump administration expects additional tariffs on India as planned next week as a result of the country's Russian crude purchases, White House trade advisor Navarro said.

- Trump said he may decide on sanctions on Russia in two weeks if needed.

- India pledged to keep buying Russian oil "depending on the financial benefit", according to Vinay Kumar, India's ambassador in Moscow.

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 25/08/2025 | 0700/0900 | ** | PPI | |

| 25/08/2025 | 0800/1000 | *** | IFO Business Climate Index | |

| 25/08/2025 | 1230/0830 | * | Quarterly financial statistics for enterprises | |

| 25/08/2025 | 1300/1500 | ** | BNB Business Confidence | |

| 25/08/2025 | 1400/1000 | *** | New Home Sales | |

| 25/08/2025 | 1400/1000 | *** | New Home Sales | |

| 25/08/2025 | 1430/1030 | ** | Dallas Fed manufacturing survey | |

| 25/08/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 25/08/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 25/08/2025 | 1915/1515 | Dallas Fed's Lorie Logan | ||

| 26/08/2025 | 2301/0001 | * | BRC Monthly Shop Price Index | |

| 25/08/2025 | 2315/1915 | New York Fed's John Williams |