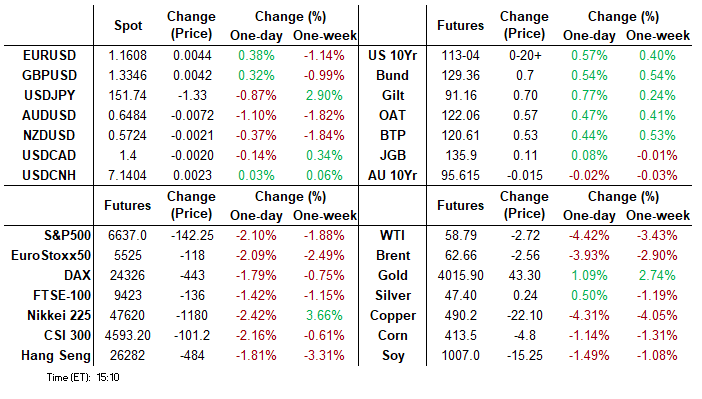

MNI ASIA MARKETS ANALYSIS: Rates Surge as Tariff Risk Returns

HIGHLIGHTS

- Treasuries gapped higher late morning Friday after Pres Trump threatened to raise tariffs on China and withdraw from a high-profile upcoming meeting with Chinese President Xi Jinping.

- Pres Trump wrote that China is “becoming very hostile” regarding export controls on rare earths and “virtually anything else they can think of, even if it’s not manufactured in China.”

- Earlier FI support after dovish Fed Gov Waller comments: open to quarter point cuts, but need to be cautious, sees one-off effect from tariffs.

US TSYS

MNI US TSYS: Extending Late Session Highs

- Treasury futures continue to extend session highs in late trade - Initially gained this morning on the back of dovish comments from Fed Gov Waller.

- Treasuries gapped higher late morning Friday after Pres Trump threatened to raise tariffs on China and withdraw from a high-profile upcoming meeting with Chinese President Xi Jinping. Pres Trump wrote that China is “becoming very hostile” regarding export controls on rare earths and “virtually anything else they can think of, even if it’s not manufactured in China.”

- Currently, Tsy Dec'25 10Y contract trades 113-05.5 (+22), yld 4.0494% -.0889; curves mixed: 2s10s -1.441 at 52.923, 5s30s +1.222 at 99.573. Approaching resistance at 113-12/29 (High Sep 18 / High Sep 11 and the bull trigger).

- Projected rate cut pricing continues to gain vs. late Thursday levels (*): Oct'25 at -24.2bp (-23.7bp), Dec'25 at -47.3bp (-44.8bp), Jan'26 at -59.7bp (-54.7bp), Mar'26 at -71.2bp (-65.2bp).

- Look ahead, cash Tsys closed for Columbus day holiday Monday - futures open along with stocks. Should be a quiet session with NFIB Small Business Optimism data at 0600ET. Philly Fed Paulson economic outlook at 1255ET, (text, Q&A).

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.13% (+0.01), volume: $2.923T

- Broad General Collateral Rate (BGCR): 4.10% (+0.01), volume: $1.148T

- Tri-Party General Collateral Rate (TCR): 4.10% (+0.01), volume: $1.120T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.10% (+0.00), volume: $84B

- Daily Overnight Bank Funding Rate: 4.10% (+0.00), volume: $174B

FED Reverse Repo Operation

RRP usage extends to new low of $4.124B (lowest level since early April 2021) with 10 counterparties this afternoon vs. $4.496B low yesterday. Compares to this year's high usage of $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR and Treasury option flow remained mixed late Friday, SOFR leaning towards low delta puts. Treasuries toward calls. Underlying futures continue to extend highs (TYZ5 113-04, +20.5) after Pres Trump threatened China with "massive increase" of tariffs. Projected rate cut pricing gains vs. late Thursday levels (*): Oct'25 at -24.2bp (-23.7bp), Dec'25 at -47.9bp (-44.8bp), Jan'26 at -60.2bp (-54.7bp), Mar'26 at -72.3bp (-65.2bp).

SOFR Options:

+10,000 SFRZ5 96.18/96.31/96.50/96.62 call condors, 7.5 ref 96.36

Block, 11,830 SFRZ5 96.50 calls, 4.0

+10,000 3QV5 96.75 puts, 5.5 vs. 96.70/0.

6,000 0QM6 97.25/98.00 call spds vs. 3QM6 96.87/97.62 call spds, cab net/steepener

+10,000 SFRZ5 96.50/96.56 call spds, 0.75 vs. 96.315/0.05

-20,000 SFRX5 96.50/96.56 call spds, 0.25 vs. 96.315/0.05%

over 14,100 SFRH6 96.25 puts, 4.0 ref 96.52

1,250 SFRH6 96.50/SFRM6 96.75 straddle spds

2,400 SFRZ5 96.12/96.18/96.25/96.31 put condors, 1 ref 96.325

+5,000 SFRZ5 96.00/96.12 put spds, 1.0 ref 96.325

+1,250 0QX5 96.75 straddles, 25.5 vs. 96.93/0.52%

+1,500 SFRH6 96.75/97.25 call spds 2.75 over 96.00/96.12 put spds

Treasury Options:

Block/screen, +69,000 wk34 FV 109.25 puts, 4.5 ref 109-17.5

Block, +12,000 wk3 TY 114 calls, 5 ref 113-03.5

8,500 TYX5 113.75 calls 13 ref 113-04

3,900 TYZ5 113 puts, 49 ref 113-02.5

over 46,300 wk5 10Y 109.5 puts, 1 ref 112-26 to -25.5

appr 10,000 TYZ5 112/113 1x2 call spds

6,000 TYZ5 114/114.5 call spds, 3 ref 112-27

5,000 USZ5 125 calls, 8 ref 117-17

over 32,100 wk3 US 112 puts, 1 ref 117-17

5,500 TYF6 111/114 strangles, ref 112-20

-1,250 TYX5 111.5/112.5 2x1 put spds, 11 ref 112-24.5/0.19%

over +10,500 wk2 TY 112.75 calls, 3-4 ref 112-22.5 to -23 (exp today)

-5,000 TYX5/TYZ5 112.5 call spds, 23 ref 112-15/0.02%

+4,700 TYZ5 112.5 calls, 53 ref 112-19.5/0.52%

+1,500 FVX 109.25 calls, 17 ref 109-08.5/0.45%

MNI BONDS: EGBs-GILTS CASH CLOSE: Late Risk-Off Rally Seals Gilt, Bund Weekly Gains

European core instruments rallied late Friday to seal a weekly drop in yields.

- Just ahead of the European cash close and the weekend, US President Trump announced on Truth Social that he was considering imposing "massive increase" of tariffs on Chinese goods after China "made a sinister move with rare earth controls".

- That triggered a significant global risk-on move, turning what had been a steadily constructive session into an outright rally for Bunds and Gilts, with bull flattening in both the German and UK curves.

- Conversely, periphery/semi-core spreads which looked to close flat/tighter to Bunds widened, and closed as such.

- OATs underperformed ahead of French President Macron's expected naming of a new Prime Minister late Friday (given the day's developments it appears likely he will opt for a candidate from the centrist/centre-right bloc or a technocrat).

- For the week, the UK curve bull flattened (2Y -0.8bp, 10Y -1.5bp) with Germany's bull steepening (2Y -6.0bp, 10Y --5.4bp).

- After hours we await Macron's announcement as well as ratings reviews of Belgium and Italy. Next week's scheduled highlight is UK August / September Labour Market Data on Tuesday.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 3.8bps at 1.959%, 5-Yr is down 5.9bps at 2.236%, 10-Yr is down 5.9bps at 2.644%, and 30-Yr is down 5.4bps at 3.225%.

- UK: The 2-Yr yield is down 4.6bps at 3.958%, 5-Yr is down 5.8bps at 4.118%, 10-Yr is down 7bps at 4.675%, and 30-Yr is down 7.4bps at 5.472%.

- Italian BTP spread up 1.3bps at 81.8bps / French OAT up 1.3bp at 83.4bps

MNI FOREX: Steady Session Gives Way to Sharp Vol

- A steady Friday session gave way to volatility just ahead of the London close, as President Trump raised a threat of further trade measures and tariffs against China as a result of Beijing's recent actions on rare earths. Risk proxies were sold hard in response, with the same names that were exposed to the tariff disputes earlier this year again being hit the hardest: AUD, NOK, ZAR and NZD are the softest currencies on the day.

- Follow-through USD sales on the Trump post have changed the intraday picture for GBP/USD, which has surged to briefly trade back above 1.3350, and help cool this week's USD rally somewhat. Focus in the coming week shifts to a busy week for the BoE, with several MPC members set to speak, while UK jobs numbers are also due. Commentary across this week flagged the sensitivity of the MPC to inflation expectations, suggesting the bar to another BoE rate cut in 2025 as a result of a weak labour market is rather high.

- With JPY rallying and AUD falling sharply on Trump's renewed tariff threat, AUD/JPY is very close to erasing the Takaichi gap. A further ~90 pip slip puts the price back to 97.35, last week's close, and would help form a long wick candlestick pattern on the weekly chart. Price action in the cross shows the real sensitivity of these two currencies to renewed tension in a trade war scenario.

- Trump's potential withdrawal from a face-to-face meeting with Xi is significant; but with two weeks to go until the APEC conference in South Korea - there still appears to be room for diplomacy - which would work against Friday's price action.

- US earnings season is set to kick off in the coming week, although the data schedule is thinner. September US CPI was originally due for release, however the US government shutdown has delayed this print until October 24th.

MNI OPTIONS: Expiries for Oct13 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1450(E804mln), $1.1570-75(E931mln), $1.1650(E772mln), $1.1700-15(E1.4bln), $1.1750-60(E3.6bln)

- USD/JPY: Y151.00($757mln)

- EUR/JPY: Y174.95-00(E560mln)

- AUD/USD: $0.6550-55(A$930mln)

MNI US STOCKS: Late Equities Roundup: Extending Lows, IT & Energy Sectors Lagging

- Stocks remain weaker late Friday, the late morning sell-off triggered by Pres Trump social media post threatening China with "massive increase" of tariffs on Chinese goods after China "made a sinister move with rare earth controls" as well as the installation on vessel fees for China-bound US ships and a probe into Qualcomm's China operations.

- Currently, the DJIA trades down 613.98 points (-1.32%) at 45,739.43, S&P E-Minis down 131.5 points (-1.94%) at 6,647, Nasdaq down 588.1 points (-2.6%) at 22,433.38 after climbing to new record high of 23,043.52 on the open.

- Information Technology and Energy sector shares continued to lead the decline:

- Synopsys -7.81%, Teradyne -6.99%, Microchip Technology -6.74%, Super Micro Computer -6.40% and ON Semiconductor -6.22%.

- APA -6.09%, Baker Hughes -4.76%, Halliburton -4.57% and Occidental Petroleum -3.96%.

- Resisting the sell-off Consumer Staples and Utility sector shares outperformed: PepsiCo +3.42%, Philip Morris International +2.92%, Campbell's Company +1.64% and Altria Group +1.54% buoyed the former, while Southern Co +1.93%, Duke Energy +1.67%, American Water Works +1.57% and Atmos Energy +1.57% buoyed Utilities.

MNI EQUITY TECHS: E-MINI S&P: (Z5) Fresh Cycle High

- RES 4: 6850.87 1.618 proj of the Aug 1 - 15 - 20 price swing

- RES 3: 6831.38 2.500 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 2: 6819.25 1.500 proj of the Aug 1 - 15 - 20 price swing

- RES 1: 6812.29 2.382 proj of the Aug 20 - 28 - Sep 2 price swing

- PRICE: 6785.00 @ 14:19 BST Oct 10

- SUP 1: 6716.75 20-day EMA

- SUP 2: 6680.00 Low Oct 1

- SUP 3: 6624.25 Low Sep 25

- SUP 4: 6598.72 50-day EMA

The trend condition in S&P E-Minis is unchanged and the direction remains up. Fresh cycle highs this week confirm a continuation of the uptrend and maintain the positive price sequence of higher highs and higher lows. The contract is holding on to its latest gains and sights are on 6812.29 and 6819.25, Fibonacci projection points. Initial support to watch is at the 20-day EMA, at 6716.75. A clear break of it would signal scope for a pullback.

COMMODITIES

MNI AMERICAS OIL: Americas End of Day Oil Summary: Crude Collapses

WTI crude collapsed below $60 under renewed pressure after Trump posts threatening more extensive tariffs against China, as well as possibly withdrawing from his face-to-face meeting with Xi, adding to pressure from an easing geopolitical risk premium and oversupply concerns. Declining consumer sentiment was also a bearish indicator. Big volumes of WTI puts at 60 and Brent puts at 65 could lead to gamma hedging (changing delta hedge positions).

- The Baker Hughes oil rig count was down 4 to 418 w/w, down 63 y/y

- The Gaza agreement reduces geopolitical risk in the key oil-exporting Middle East after prices had risen earlier in the week following a more cautious OPEC November output increase.

- Venezuela is said to have offered the US various concessions including stakes in its oil resources in an effort to avoid US conflict, before diplomatic efforts broke down earlier this week, according to the NYT.

- Saudi Aramco is set to sell ~39-40mbbl of contractual supplies of November loading crude to China, compared to 50-51mbbl a month ago, Bloomberg said. Lower than expected OSPs announced earlier this month weren’t enough to rise buying interest, Bloomberg sources said.

- WTI Nov futures were down 4.2% at $58.90

- WTI Dec futures were down 4.1% at $58.49

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 13/10/2025 | 1105/1205 | BOE Greene at Society of Professional Economists Conference | ||

| 13/10/2025 | - | *** | Trade | |

| 13/10/2025 | - | *** | Money Supply | |

| 13/10/2025 | - | *** | New Loans | |

| 13/10/2025 | - | *** | Social Financing | |

| 13/10/2025 | - | ECB Lagarde and Cipollone at IMF/World Bank Meetings | ||

| 13/10/2025 | 1655/1255 | Philly Fed's Anna Paulson | ||

| 13/10/2025 | 1910/2010 | BOE Mann in MonPol Panel, National Association of Business Economists | ||

| 14/10/2025 | 2301/0001 | * | BRC-KPMG Shop Sales Monitor |