MNI ASIA MARKETS ANALYSIS: Projected Rate Cuts Consolidate

HIGHLIGHTS

- Treasuries look to finish back near early morning lows following a knee-jerk reaction to a drop in weekly and continuing jobless claims data Thursday.

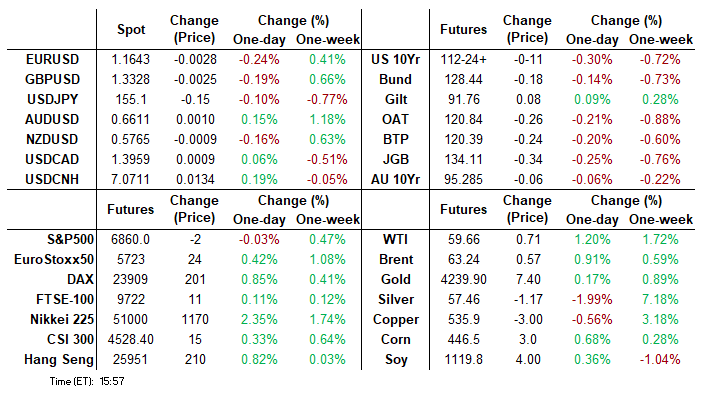

- The grinding retreat in rates correlated with projected rate cut pricing consolidating vs. late Wednesday levels (*): Dec'25 at -22.9bp (-23.6bp), Jan'26 at -30.6bp (-31.4bp), Mar'26 at -38.6bp (-40.4bp), Apr'26 at -45.1bp (-47.9bp).

- The USD index traded down to a pullback low of 98.77, however, looks set to post a small winning day as we approach the APAC crossover.

- Wall Street executives and bond investors expressed concern to the US Treasury over NEC Director Kevin Hassett's potential nomination as Federal Reserve chair.

US TSYS

MNI US TSYS: Revisiting Early Session Lows, Surprise Weekly Claims Decline

- Treasuries look to finish near early Thursday session lows - grinding lower all day after rebounding from this morning's knee-jerk sell-off following lower than expected weekly and continuing jobless claims data.

- Currently, TYH6 trades -11.5 at 112-24 vs. 112-22 low, key support and Nov 5 low below at 112-07.

- Initial jobless claims were far lower than expected at 191k (sa, cons 220k) in the week to Nov 29 after a marginally upward revised 218k (initial 216k). It’s the lowest seasonally adjusted figure since Sep 2022 although we’re always cautious about reading too much into a single week around the Thanksgiving holiday.

- Continuing claims were also better than expected but less surprisingly so, at 1939k (sa, cons 1963k) in the week to Nov 22 after another downward revision to 1943k (initial 1960k).

- The Atlanta Fed’s GDPNow has been revised down marginally from 3.85% to 3.81% for annualized real GDP growth in Q3. Ahead of next week’s FOMC meeting, it currently paints a very similar picture to the 3.84% in Q2. What’s more, the drivers behind this quarterly growth are indicative of underlying strength, with private domestic final purchases estimated at ~2.9% annualized after 2.86% in Q2.

- Look ahead to Friday: Personal Income/Outlays, UofM Consumer Survey. Non-Farm payrolls are not released tomorrow but are rescheduled for December 16.

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.95% (-0.06), volume: $3.360T

- Broad General Collateral Rate (BGCR): 3.90% (-0.06), volume: $1.331T

- Tri-Party General Collateral Rate (TCR): 3.90% (-0.06), volume: $1.302T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.89% (+0.00), volume: $85B

- Daily Overnight Bank Funding Rate: 3.89% (+0.00), volume: $153B

FED Reverse Repo Operation

RRP usage slips to $2.233B while counterparties retreat by 1 to 39 this afternoon from $2.514B Wednesday. Compares to last Tuesday November 18: $0.905B - lowest level since mid-March 2021; this years highest excess liquidity measure: $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury options turned mixed by midday Thursday, some larger rate cut call plays adding to second half volumes. Pick-up in calls fading the continued decline in underlying futures while projected rate cut pricing consolidated vs. late Wednesday levels (*): Dec'25 at -22.9bp (-23.6bp), Jan'26 at -30.6bp (-31.4bp), Mar'26 at -38.6bp (-40.4bp), Apr'26 at -45.1bp (-47.9bp).

SOFR Options:

Block/screen, 41,750 SFRU6/0QU6 97.00/97.50 call spd spd, 3.0 net 0QU6 over

+2,500 SFRG6/SFRH6 96.43/96.56/96.68 call fly strip, 3.5 total

+10,000 SFRZ5 96.06/96.12 2x1 put spds, .25

+20,000 SFRZ5 96.18 puts, 0.75

+2,500 SFRG6/SFRH6 96.43/96.56/96.68 call fly strip, 3.5 total

+10,000 SFRU6/0QU6 98.00 call spds 0.0

+2,000 SFRF6 96.56/96.68/96.81 call flys, 1.5 ref 96.45

+5,000 SFRZ5 96.31 calls, 0.5 ref 96.2725

+5,000 SFRZ6 98.00 calls, 7.0 ref 96.92

Block, 6,000 SFRH6 96.37 calls, 13.25

+15,500 SFRH6 96.37 puts vs. 96.62/96.75 call spds ref 96.46 to -.455/0.46%

+5,000 SFRH6 96.25 puts, 1.0

1,000 SFRH6/SFRF6 96.43 straddle spd, 7.25

4,000 SFRH6 96.43 puts vs. 96.43/96.56 call spds ref 96.46

2,000 SFRZ5 96.18/96.25/96.31 put flys, 2.25 ref 96.2725

2,000 SFRF6 96.25/96.31/96.37/97.43 put condors ref 96.46

5,000 SFRF6 96.25/96.31/96.37/97.43 call condors, 3.0 ref 96.46

4,000 0QZ5 97.00/97.18 call spds ref 96.93

Treasury Options:

-5,000 TYG6 112.5/113.5 strangles, 107

Block, +10,000 TYF6 113/113.5 strangles, 56 vs. 112-22/0.05%

Block, 8,000 TYF6 112 puts, 13 vs. 112-23.5/0.18%

+20,000 TYH6 115 calls 20 vs. 112-26.5/0.20% appr 5.07 vol (expires Feb 20. '26)

-17,000 TYF6 112.5/113.25 strangle, 43

3,500 FVF6 110 calls, 9.5 ref 109-15.25

+7,200 TYH6 111 puts, 22

7,500 FVF6 109.5/110 1x2 call spds ref 109-15

1,000 TYF6 110.5/112.5 2x1 put spds ref 112-27.5

-2,000 TYF6 111 puts, 2

-2,500 TYF6 114 calls,10

-1,000 FVF6 109.75 straddles, 45.5

-2,000 wk1 TY 112.75 calls, 17

EGBS

• 2y/10y bunds are closing +1bp/+2bp at 2.07%/2.77%. UST 10yr +3.7bps as initial claims came in low.

• €IG closes -1.2bp on average.

• Supply - EUR Fins: DB (Long 5NC4 SP). GBP Corps: ARNDTN (7yr SUN).

• SX5E/SPX futures are +0.5%/-0.1% at 5730pts/6857pts. €IG movers included Hyundai Motor Co (+6%), 3i Group (+6%), Daimler Truck Holding (+5%), Renault (+5%), PVH (-11%), Koninklijke Philips (-6%), Tauron Polska Energia (-4%), LyondellBasell Industries (-4%).

• Main/XO finish +0.3bp/+1bp at 52.8bp/256bp

MNI FOREX: USD Index Plumbs Fresh Pullback Lows Before Stabilising

- The USD traded with more mixed sentiment on Friday, as initial momentum selling may have stalled in respect of the well below-forecast initial jobless claims data – providing a moderately more optimistic short-term view of the US labour market. The USD index traded down to a pullback low of 98.77, however, looks set to post a small winning day as we approach the APAC crossover.

- USDJPY was a focus through European trade, as headlines surrounding the December BOJ meeting helped bolster expectations for an imminent hike. The yen received a decent boost, prompting USDJPY to reach a new weekly low of 154.51, before the post-data stabilisation has seen spot edge closer to 155 at typing. Most recent price action has strengthened the chances for a deeper correction, targeting the 50-day EMA at 153.34.

- In similar vein, GBPUSD briefly extended its impressive surge on Wednesday, rallying as high as 1.3385. Sterling strength was driven by both the key break of 0.8746-51 in EUR/GBP as well as the continued unwind of pre-Budget vol. 3m GBPUSD implied vol is now at the second-lowest level for this time of year of this century, after 2012.

- AUDUSD also traded through the late October highs of 0.6618 and has now posted 9 consecutive sessions of higher highs. While negative carry for long AUDUSD remains, acute pressure in the front-end of the curve means the 3m carry / vol ratio is at the highest level since April.

- In emerging markets, USDMXN slipped to an 11-week low and hovers just above the cycle lows and key support level at 18.20. Importantly, President Sheinbaum is expected to meet President Trump tomorrow, providing some more tepid optimism over upcoming trade discussions. We have emphasised the dominant downtrend in place, signalling the potential for a larger move towards 17.4491.

- Canadian employment data headlines tomorrow’s economic calendar. US monthly PCE data and Michigan sentiment figures will also be released.

MNI FX OPTIONS: Expiries for Dec05 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600(E1.2bln), $1.1715(E959mln)

- USD/JPY: Y155.00($1.4bln)

- GBP/USD: $1.3210(Gbp745mln), $1.3250(Gbp653mln)

- AUD/USD: $0.6500(A$1.1bln)

- USD/CAD: C$1.3990-15($1.3bln)

MNI US STOCKS: Late Equities Roundup: Late Sell Programs Extend Index Lows, Rebound

- US stocks retreated to moderately lower levels late Thursday, Nasdaq shares still inside the session range. Stocks had scaled back modest early gains as rates traded lower and projected rate cut pricing consolidates vs. late Wednesday levels.

- Currently, the DJIA trades down 42.86 points (-0.09%) at 47843.02, S&P E-Mini Futures down 2.25 points (-0.03%) at 6861, Nasdaq up 18.5 points (0.1%) at 23473.98.

- Consumer Staples and Discretionary sector shares led late session declines, big-box retailers and manufacturers weighing:

- Kroger Co -4.05%, Costco Wholesale -3.36%, Philip Morris Int -2.74% and Brown-Forman -1.73%;

- Travel related stocks also weighed on the Discretionary sector: Wynn Resorts -5.95%, Marriott International -4.19% and Hilton Worldwide -2.62%.

- Meanwhile, Health Care sector shares also underperformed: UnitedHealth Group -2.94%, Zoetis -2.02%, IQVIA Holdings -1.90%, Eli Lilly -1.86% and GE HealthCare Technologies -1.64%

- On the positive side, Industrials and Communications sector shares continued to outperform in late trade:

- GE Vernova +5.33%, EMCOR Group +3.78%, Generac Holdings +3.69%, Leidos Holdings +2.69%, Quanta Services +2.21% and Huntington Ingalls Industries +2.14%.

- Meta Platforms +3.90%, Live Nation Entertainment +2.12%, TKO Group Holdings +1.49% and Verizon Communications +1.34%.

MNI EQUITY TECHS: E-MINI S&P: (Z5) Trading At Its Latest Highs

- RES 4: 7000.00 Psychological round number

- RES 3: 6953.75 High Oct 30 and bull trigger

- RES 2: 6900.50 High Nov 12

- RES 1: 6880.75 Intraday high

- PRICE: 6873.25 @ 14:31 GMT Dec 4

- SUP 1: 6780.31 20-day EMA

- SUP 2: 6674.50/6525.00 Low Nov 25 / 21

- SUP 3: 6500.00 Round number support

- SUP 4: 6476.62 23.6% retracement of the Apr 7 - Oct 30 uptrend

A bullish theme in S&P E-Minis is intact and the contract is trading at its latest highs. Price also remains above the 20- and 50- day EMAs. Note that recent gains signal the likely end of the corrective cycle between Oct 30 and Nov 21. A continuation higher would highlight potential for a move towards the key resistance and bull trigger at 6953.75, the Oct 30 high. Key support lies at 6525.00, the Nov 21 low.

MNI COMMODITIES: Crude Rises Further, Silver Pulls Back From Record High

- WTI crude has risen further on Thursday, although it remains within the range seen since Nov 23. Geopolitical risks for Ukraine and Venezuela are supporting crude but projections for a record market surplus next year remain a concern.

- WTI Jan 26 is up by 1.2% at $59.6/bbl.

- From a technical perspective, short-term gains in WTI futures are considered corrective. Note that moving average studies are in a bear-mode position, highlighting a dominant downtrend.

- A resumption of the bear leg would open the key support and the bear trigger at $55.99, the Oct 20 low. Key short-term resistance to watch is $61.84, the Oct 24 high.

- Elsewhere, precious metals have had a mixed day, with spot gold trading in a relatively tight range, but silver notably underperforming.

- Gold is currently just 0.1% higher at $4,207/oz, while silver has fallen by 2.6% to $57.0/oz. As a result, the gold-silver ratio has bounced off yesterday’s four-year lows.

- Despite today’s profit taking, silver remains more than 20% higher over the last month, and ING expects prices to remain well supported amid resilient industrial demand and tight supply.

- For gold, the trend condition remains bullish, with sights on key resistance and the bull trigger at $4,381.5, the Oct 20 high.

- Trend signals in silver are also still bullish, with scope seen for a climb towards $59.563 next, a Fibonacci projection. Initial support lies at $53.53, the 20-day EMA.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 05/12/2025 | 0700/0800 | ** | Manufacturing Orders | |

| 05/12/2025 | 0730/0730 | DMO to publish issuance calendar for FQ4 | ||

| 05/12/2025 | 0745/0845 | * | Industrial Production | |

| 05/12/2025 | 0745/0845 | * | Foreign Trade | |

| 05/12/2025 | 0800/0900 | ** | Industrial Production | |

| 05/12/2025 | 0900/1000 | * | Retail Sales | |

| 05/12/2025 | 1000/1100 | *** | EZ GDP 3rd (Regular) | |

| 05/12/2025 | 1330/0830 | *** | Labour Force Survey | |

| 05/12/2025 | 1500/1000 | *** | U. Mich. Survey of Consumers | |

| 05/12/2025 | 1500/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 05/12/2025 | 1500/1000 | *** | Personal Income and Consumption | |

| 05/12/2025 | 1510/1610 | ECB Lane in Panel at CEPR Paris Symposium | ||

| 05/12/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 05/12/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 05/12/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 05/12/2025 | 2000/1500 | * | Consumer Credit |