US STOCKS: Late Equities Roundup: Late Sell Programs Extend Index Lows, Rebound

Dec-04 19:40

- US stocks retreated to moderately lower levels late Thursday, Nasdaq shares still inside the session range. Stocks had scaled back modest early gains as rates traded lower and projected rate cut pricing consolidates vs. late Wednesday levels.

- Currently, the DJIA trades down 42.86 points (-0.09%) at 47843.02, S&P E-Mini Futures down 2.25 points (-0.03%) at 6861, Nasdaq up 18.5 points (0.1%) at 23473.98.

- Consumer Staples and Discretionary sector shares led late session declines, big-box retailers and manufacturers weighing:

- Kroger Co -4.05%, Costco Wholesale -3.36%, Philip Morris Int -2.74% and Brown-Forman -1.73%;

- Travel related stocks also weighed on the Discretionary sector: Wynn Resorts -5.95%, Marriott International -4.19% and Hilton Worldwide -2.62%.

- Meanwhile, Health Care sector shares also underperformed: UnitedHealth Group -2.94%, Zoetis -2.02%, IQVIA Holdings -1.90%, Eli Lilly -1.86% and GE HealthCare Technologies -1.64%

- On the positive side, Industrials and Communications sector shares continued to outperform in late trade:

- GE Vernova +5.33%, EMCOR Group +3.78%, Generac Holdings +3.69%, Leidos Holdings +2.69%, Quanta Services +2.21% and Huntington Ingalls Industries +2.14%.

- Meta Platforms +3.90%, Live Nation Entertainment +2.12%, TKO Group Holdings +1.49% and Verizon Communications +1.34%.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US STOCKS: Late Equities Roundup: Weaker Into Late Cycle Earnings, Midweek Data

Nov-04 19:39

- Stocks remain in weaker territory late Tuesday, near session lows amid moderate risk-off support in rates. Focus is on late cycle corporate earnings as the US Government shutdown ties the longest in history at 35 days, while Wednesday sees non-government produced economic data: ADP employment, S&P Global US Services/Composite PMI and ISM Services.

- Currently, the DJIA down 308.53 points (-0.65%) at 47032.11, S&P E-Minis down 79.75 points (-1.16%) at 6804.25, Nasdaq down 437.7 points (-1.8%) at 23399.8.

- A mix of Pharmaceutical, Energy, Materials and Information Technology sector shares continued to decline in late trade: Zoetis -12.66%, CDW Corp -10.12%, Albemarle Corp -8.08%, Palantir Technologies -7.93%, Gartner -6.88%, Synopsys -5.97%, Skyworks Solutions -5.96%, Marathon Petroleum -5.92% and Micron Technology -5.76%

- Weighing on the Consumer Discretionary sector - notable declines also reported in cruise lines: Norwegian Cruise Line -15.37%, Carnival Corp -9.35% and Royal Caribbean Cruises -7.09%.

- Conversely, the Financials sector, particularly insurance providers continued to outperform in late trade: Apollo Global Management +5.69%, Willis Towers Watson +3.01%, Global Payments +2.93% and Travelers Cos Inc +2.75%. Health Care sector shares followed: Henry Schein +9.39%, Waters Corp +6.46%, Centene Corp +3.80% and Molina Healthcare 3.30%.

- Stocks expected to announce earnings after the close include: Arista Networks Inc, Live Nation Entertainment, Corteva, Rivian Automotive, Advanced Micro Devices, American International Grp, Mosaic Co, Pinterest, Match Group, AES Corp, Super Micro Computer, Amgen Inc.

US TSYS/SUPPLY: Limited New Buyback Developments Seen (2/3)

Nov-04 19:33

Other aspects of note in Wednesday's Refunding:

- Buybacks: After being in some focus in August's Refunding, we don’t expect any changes to buyback program parameters this time, following the last round’s amendments that included higher-frequency operations/increasing the size of long-end buybacks.

- There are some risks that buyback sizes could be slightly increased, or that Treasury announces that the list of eligible counterparties will be expanded.

- Other Announcements: The discussion topics in the latest Primary Dealer survey ahead of the Refunding process usually provide some clues as to the don’t contain too many areas of market-moving interest: they include post-auction settlement periods for 20Y Bond, though does also ask about views regarding the Fed’s balance sheet policy (though some of these questions are already out of date, including: when QT is expected to end and whether the Fed is seen buying Treasuries with MBS proceeds).

- Upcoming Issuance: The Refunding itself will be $58B in new 3Ys, $42B in new 10Y, and $25B in new 30Y for next week. November’s issuance schedule is set to see $324B in nominal Treasury coupon sales (unch from the equivalent month in the previous quarter), in addition to $19B in 10Y TIPS (unch from prior) and $28B FRN (unch) for a total of $371B.

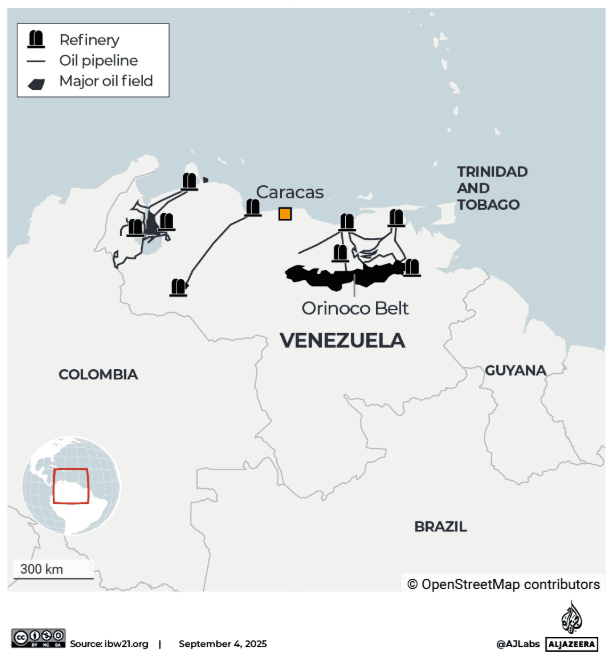

ENERGY SECURITY: Trump Weighing Venezuela Options: NYT

Nov-04 19:30

The NYT released an article citing US officials which states that the Trump administration has developed a range of military options against Venezuela, including seizing oil fields.

- Officials said Trump is in no rush to decide on action. He remains reluctant to approve operations that may fail and risk American troops. His public remarks on action have also been conflicting.

- The NYT said that a decision will be delayed at least until the Gerald R Ford aircraft carrier arrives in the Caribbean in mid-Nov.

- The three options for action cited by the NYT include:

- Airstrikes on military facilities to hit military support for Maduro, forcing him to flee.

- Sending US special forces to try and capture Maduro, arguing he is the head of a narco-terrorist organisation (cartel de los soles whose very existence is disputed)

- A more complicated plan to send US counter terrorism forces to seize control of airfields and at least some oil fields and infrastructure. Given the location of key oil fields compared to export terminals, this could require a significant occupation.

- There are also those who see the military build-up as a psychological campaign to force Maduro to flee.

- Maduro has offered the US a dominant role in Venezuela’s oil industry to avert conflict, but this was said to have been rejected.

- If Maduro was to fall and be replaced by stable leadership, Chevron would be well placed for the boon in oil investment. However, the army remains very pro-Maduro; US military involvement risks sparking an armed insurgency and further destabilising the nation.