MNI ASIA MARKETS ANALYSIS: Nascent Risk-On, Stocks New Highs

HIGHLIGHTS

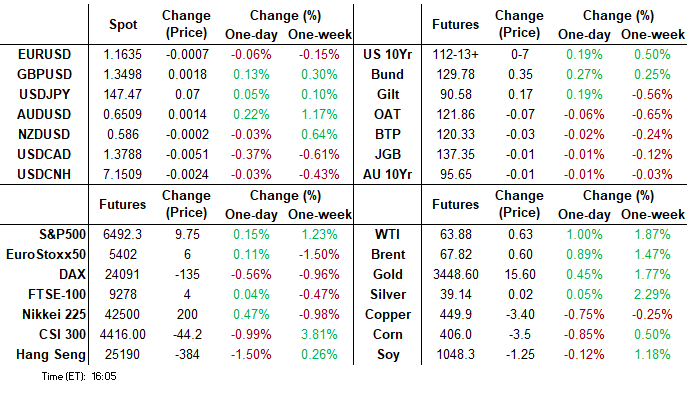

- Treasuries reversed early weakness, initially following German Bunds & French Oat rate futures Wednesday.

- Treasuries extended highs in late trade despite selling after a weak $70B 5Y Note auction 3.724% high yield vs. 3.716% WI.

- NY Fed President Williams (permanent FOMC voter) on CNBC didn't sound particularly concerned over state of the labor market, downplaying weak nonfarm payrolls growth implied by the July's downward revisions.

US TSYS

MNI US Tsys Tracked German Bund, French Oat Earlier, Extend Late Highs

- Tsys reversed early weakness - extended highs in 2s-10s - following German Bund and French Oat contracts. Sources posited real$ bought the early dip in OATS squeezing shorts with Bunds then Tsys reacting in short order on decent volumes.

- Dec'25 10Y contract tapped 112-15, just below technical resistance at 112-15+, the Aug 5 high and the bull trigger. Clearance of this hurdle would resume the uptrend and pave the way for a climb towards 112-19 initially, a Fibonacci projection.

- Tsy curves twist steeper: 2s10s +3.484 at 61.533 (nearing mid-April's 3Y highs), 5s30s +3.160 at 120.597.

- No reaction to MBA composite mortgage applications dip -0.5% (sa) last week after -1.4% the week prior as they still holds onto most of its refi-driven 11% increase before that. New purchase applications increased 2.2%, their largest increase in a month, whilst refi applications fell another -3.5% after -3.1% following the 23% jump before that.

- NY Fed President Williams (permanent FOMC voter) on CNBC doesn't sound particularly concerned about the state of the labor market, in particular downplaying the weak nonfarm payrolls growth implied by the July employment report's downward revisions.

- Uncertainty over an independent Federal Reserve aside (following Trump's "firing" of Fed Gov Cook late Monday) Trump seeking a majority of like minded Fed boardmen in the aftermath of Chairman Powell's dovish Jackson Hole speech appears to be emboldening risk takers as SPX emini and Nasdaq indexes made new highs (6502.50 and 21616.18 respectively)

- Look ahead to Thursday's session: Weekly Claims, GDP, PCE and US Tsy $44B 7Y Auction.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.38% (+0.01), volume: $2.820T

- Broad General Collateral Rate (BGCR): 4.37% (+0.02), volume: $1.164T

- Tri-Party General Collateral Rate (TCR): 4.37% (+0.02), volume: $1.125T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $113B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $226B

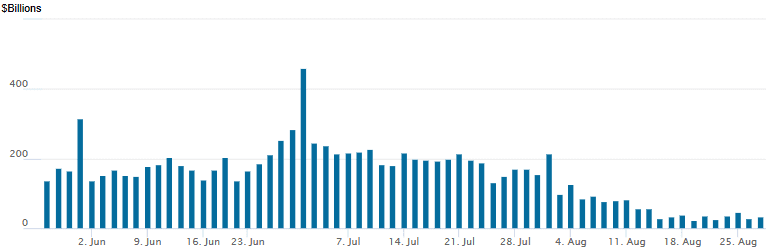

FED Reverse Repo Operation

RRP usage rebounds to $34.744B with 21 counterparties this afternoon, from $28.574B yesterday. Compares to $22.344B on Tuesday, Aug 19 - lowest since April 5, 2021 vs. this year's high usage of $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR/Treasury option volumes improved in the second half, flow mixed with large Oct 5Y put buyer in Tsys, SOFR options revolving around better calls. Underlying futures off early session lows with TYZ5 nearing initial resistance at 112-15.5 (High Aug 5 and the bull trigger), curves twist steeper with 2s10s +3.063 at 61.112 (near Mid-April levels last seen early 2022)., 5s30s +2.986 at 120.423. Projected rate cuts have gained slightly vs. early morning (*) levels: Sep'25 at -21.6bp (-21.4bp), Oct'25 at -34.6bp (-34.1bp), Dec'25 at -55.6bp (-54.4bp), Jan'26 at -69.1bp (-68.1bp).

SOFR Options:

+8,000 SFRZ5 96.50/97.00 call spds, 4.125 ref 96.235

5,000 0QZ5 97.50 calls ref 97.025

+20,000 SFRH6 96.75/97.25 call spds, 8.5

-5,000 SFRU6 95.50/98.25 call over risk reversals, 5.0 vs. 96.925

-4,000 SFRH6 96.50 calls, 22.5 vs. 96.495/0.50%

-5,000 SFRM6 97.00/97.50 call spds vs. 3QM6 96.87/97.37 call spds, 0.0 net

-5,000 SFRZ5 96.00 puts, 4.5

-2,500 SFRU6 97.75/98.00 call strip w/ 96.00 put vs. 96.87 straddle, 42.0 total (straddle sold over)

Block, 5,700 SFRU5 96.00/96.06/96.18/96.25 call condors 0.5 ref 95.89

+2,500 SFRU5 96.00/96.06/96.18/96.25 call condors, 0.5 vs 95.9175/0.05%

2,000 2QZ5 96.25/96.37/96.62 broken put flys, 4.5 ref 96.85/0.10%

+2,000 0QU5/2QU5 97.12 call spds, 1.0 net

2,600 SFRF6 96.50 calls ref 96.475

Treasury Options:

Block/screen +50,000 FVV5 108.5 puts, 6.5-7.0 vs. 109-13.75/0.18%

+12,000 wk5 TY 112.5 calls, 7 vs. 112-12/0.36%

-3,000 TYV5 111/113.5 strangles, 29

-2,500 TYV5 112.25 straddles, 120

+4,000 TYX5 109.5/113 strangles, 48

4,000 TYV5 112.5/113/113.5 call flys

+1,600 TUZ5 104.5/105.25 2x3 call spds, 13

1,900 USV5 111.5/112.5 put spds ref 113-30

-2,500 USV5 111 puts, 23 ref 114-00

+2,000 TYV5 109.5 puts, 4 vs. 112-00.5/0.08%

MNI BONDS: EGBs-GILTS CASH CLOSE: OATs Extend Underperformance

OATs underperformed for a 3rd consecutive session as French political concerns lingered.

- Core EGBs and Gilts gained in morning trade, the latter after registering fresh cycle lows at the open, amid a bit of risk-off with equities sagging.

- Impactful data was limited, but regional politics were a key focus, with France's Sep 8 no-confidence vote continuing to weigh on OATs (the Dutch government survived a no-confidence motion of its own today, though this was expected).

- Outright OAT yields hit recent highs with 30Y seeing yields hit a 14-year high, as spreads to Bunds continued to widen.

- Trade turned more constructive going into the close, with OATs seemingly finding a footing, boosting Bunds and Gilts (as well as Treasuries).

- The belly outperformed on the German curve (despite a soft 7Y auction), with yields down throughout, while the UK curve saw yields drop more or less in parallel.

- Thursday's data schedule includes consumer and business confidence for Italy and the Eurozone, along with an appearance by the ECB's Rehn and the account of the July ECB meeting.

- The week's regional focus - the Eurozone August flash inflation round - technically starts Thursday (Belgium is due) but most attention will be on Friday's releases for Spain, France, Italy, and Germany. MNI's preview is here.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 2.3bps at 1.915%, 5-Yr is down 3.1bps at 2.237%, 10-Yr is down 2.3bps at 2.7%, and 30-Yr is down 1.3bps at 3.307%.

- UK: The 2-Yr yield is down 0.4bps at 3.964%, 5-Yr is down 0.6bps at 4.133%, 10-Yr is down 0.4bps at 4.736%, and 30-Yr is down 0.8bps at 5.6%.

- Italian BTP spread up 4bps at 87.3bps / French OAT up 5.1bps at 82.4bps

MNI EGB OPTIONS: Large Euribor Upside, Closing Sonia Call Condor Position Wednesday

Wednesday's Europe rates/bond options flow included:

- RXV5 128/127ps 1x1.5, bought for 18.5 in 4k

- ERH6 98.18/98.00ps, sold at 10.5 in 3.75k

- ERZ6 99.00/99.50cs, bought for 2 in 28k

- SFIZ5 96.10/96.25/96.40/96.55c condor, sold at 4.5 in 11k total now (closing)

- SFIH6 96.40/96.50cs vs 96.00p, bought the cs for 0.25 in 3.5k total

MNI FOREX: Early Dollar Strength Dissipates, US GDP/PCE Awaited

- Initial weakness for European stocks on Wednesday worked in favour of the dollar, prompting some notable weakness for the rest of the G10 FX complex. French political uncertainty likely stoked these concerns, weighing on EURUSD in particular. However, firmer sentiment for equities as the session progressed, and a bounce for French OATs then assisted a reversal back into the ranges for most major pairs.

- For EURUSD, the initial price action took spot below 1.16 and the key 50-day EMA pivot support, threatening an important bearish development. However, with spot now residing around 50 pips off the 1.1574 lows, the bullish overall trend looks set to stay intact.

- EURAUD breaking to new daily lows through the WMR fix puts the price clear of both the 50-dma at 1.7893 and likely avoids the formation of support at a possible up-trendline drawn off the February lows.

- Weakness for the New Zealand dollar still stands out, and despite the most recent bounce, spot has narrowed the gap to the pre-Powell lows overall, located at 0.5800.

- Friday’s low print adds to the medium-term significance of this level, which has proven an important pivot point dating back to late 2023. A break of the figure will be required for a deeper selloff, potentially targeting a move to 0.5728, the 61.8% retracement of the Apr/Jul rally.

- Despite USDJPY attempting to break back above 148.00 during the European morning, the pair tracks back around 147.50 as US GDP (2nd read) and PCE prints are awaited across Thursday and Friday.

- In emerging markets, more concrete details on a security deal being achieved between Mexico and the US provided a late boost for the Mexican peso. USDMXN had traded back up to resistance at 18.80 before the headlines, and the late dollar weakness provided an additional headwind for USDMXN, which trades back towards 18.69 approaching the APAC crossover.

MNI FX OPTIONS: Expiries for Aug28 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600(E624mln), $1.1625(E561mln), $1.1675(E694mln)

- GBP/USD: $1.3405-25(Gbp656mln)

- USD/JPY: Y148.10-25($593mln)

- USD/CAD: C$1.3740-45($714mln), C$1.3780-95($767mln), C$1.3950($508mln)

MNI US STOCKS: Late Equities Roundup: New Highs for SPX, Nasdaq

- Stocks continue to drift near or above last Friday's record highs this Wednesday. Reminder: Nvidia earnings expected to be announced after today's close (1620-1630ET with Nvidia expected to host a conference call at 1700ET).

- Currently, the DJIA trades up 187.41 points (0.41%) at 45605.62 (off Friday's 45727 record high), S&P E-Mini Future up 18.5 points (0.29%) at 6501.25 - surpassing Friday's 6401.25 high, and Nasdaq up 57.7 points (0.3%) at 21601.63 vs. 21616.18 record high today.

- Energy and Information Technology sector shares led gainers in late trade, oil and gas stocks rising with a moderate rebound in crude this morning (WTI +0.90 at 64.15): APA +2.53%, Valero Energy +2.50%, Marathon Petroleum +2.43%, Phillips 66 +2.19%, Halliburton +2.10% and Diamondback Energy +2.05%.

- The tech sector buoyed by: Datadog +3.71%, ServiceNow +2.48%, Salesforce +2.42% and Intel Corp +2.22%.

- On the flipside, Communication Services and Health Care sector shares underperformed: Paramount Skydance -5.87% on downgrade at from Morgan Stanley, Meta Platforms -0.85%, News Corp -0.55% and Live Nation Entertainment -0.43%..

- Health Care sector laggers included DaVita -0.61%, Amgen I-0.52%, Humana -0.46% and Gilead Sciences -0.41%.

MNI EQUITY TECHS: E-MINI S&P: (U5) Northbound

- RES 4: 6600.00 Round number resistance

- RES 3: 6586.68 2.0% 10-dma envelope

- RES 2: 6523.63 1.764 proj of the May 23 - Jun 11 - 23 price swing

- RES 1: 6508.75 High Aug 15 and all-time High

- PRICE: 6488.50 @ 14:32 BST Aug 27

- SUP 1: 6362.75 Low Aug 20

- SUP 2: 6313.25 Low Aug 6

- SUP 3: 6311.73.76 50-day EMA

- SUP 4: 6239.50 Low Aug 1

The dominant uptrend in S&P E-Minis remains intact and the contract is trading at its recent highs. Moving average studies are in a bull-mode position, highlighting a clear uptrend and positive market sentiment. Attention is on 6508.75, the Aug 15 high and the bull trigger. Clearance of this level would confirm a resumption of the uptrend and open 6523.63, a Fibonacci projection. Support to watch lies at 6311.73, the 50-day EMA.

MNI COMMODITIES: Crude Finds Support, Gold Unchanged, Copper Declines

- Oil prices found support on Wednesday, supported by a slightly larger than expected US crude stock draw.

- A breakdown in E3 talks with Iran also added support earlier in the session, along with growing threats from the EU to further sanctions on Russia – though its options remain limited.

- WTI Oct 25 is up by 1.4% at $64.2/bbl.

- A bear cycle in WTI futures remains intact and the latest round of short-term gains appear corrective - for now.

- Initial support is at $61.99, the Jun 30 low, which has recently been breached, strengthening a bearish theme. Initial resistance to watch is at $66.56, the Aug 4 high.

- Elsewhere, spot gold is broadly unchanged on the session around $3,395/oz, after rallying off session lows following the IAEA-Iran headlines that flagged that monitors have not yet returned to damaged Iranian sites. Reports also suggested that Iran isn’t providing adequate access to inspectors.

- The medium-term trend condition for gold remains bullish, with initial resistance seen at $3,409.2, the Aug 8 high, followed by $3,439.0, the Aug 23 high.

- Meanwhile, copper has fallen by 0.9% to $449/lb today.

- Copper futures are in consolidation mode, with initial resistance at $488.17, the 50-day EMA. On the downside, a continuation lower would signal scope for a test of key support at $418.85, the Apr 7 low.

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 28/08/2025 | 0700/0900 | ** | Economic Tendency Indicator | |

| 28/08/2025 | 0700/0900 | *** | GDP | |

| 28/08/2025 | 0700/0900 | ** | KOF Economic Barometer | |

| 28/08/2025 | 0800/1000 | ** | M3 | |

| 28/08/2025 | 0800/1000 | ** | ISTAT Consumer Confidence | |

| 28/08/2025 | 0800/1000 | ** | ISTAT Business Confidence | |

| 28/08/2025 | 0900/1100 | * | Consumer Confidence, Industrial Sentiment | |

| 28/08/2025 | 1230/0830 | *** | Jobless Claims | |

| 28/08/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 28/08/2025 | 1230/0830 | * | Current account | |

| 28/08/2025 | 1230/0830 | * | Payroll employment | |

| 28/08/2025 | 1230/0830 | *** | GDP / PCE Quarterly | |

| 28/08/2025 | 1400/1000 | ** | NAR Pending Home Sales | |

| 28/08/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 28/08/2025 | 1500/1100 | ** | Kansas City Fed Manufacturing Index | |

| 28/08/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 28/08/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 28/08/2025 | 1700/1300 | ** | US Treasury Auction Result for 7 Year Note | |

| 28/08/2025 | 2200/1800 | Fed Governor Christopher Waller | ||

| 29/08/2025 | 2330/0830 | * | Labor Force Survey | |

| 29/08/2025 | 2330/0830 | ** | Tokyo CPI | |

| 29/08/2025 | 2350/0850 | ** | Industrial Production | |

| 29/08/2025 | 2350/0850 | * | Retail Sales (p) |