FOREX: Early Dollar Strength Dissipates, US GDP/PCE Awaited

Aug-27 16:41

- Initial weakness for European stocks on Wednesday worked in favour of the dollar, prompting some notable weakness for the rest of the G10 FX complex. French political uncertainty likely stoked these concerns, weighing on EURUSD in particular. However, firmer sentiment for equities as the session progressed, and a bounce for French OATs then assisted a reversal back into the ranges for most major pairs.

- For EURUSD, the initial price action took spot below 1.16 and the key 50-day EMA pivot support, threatening an important bearish development. However, with spot now residing around 50 pips off the 1.1574 lows, the bullish overall trend looks set to stay intact.

- EURAUD breaking to new daily lows through the WMR fix puts the price clear of both the 50-dma at 1.7893 and likely avoids the formation of support at a possible uptrendline drawn off the February lows.

- Weakness for the New Zealand dollar still stands out, and despite the most recent bounce, spot has narrowed the gap to the pre-Powell lows overall, located at 0.5800.

- Friday’s low print adds to the medium-term significance of this level, which has proven an important pivot point dating back to late 2023. A break of the figure will be required for a deeper selloff, potentially targeting a move to 0.5728, the 61.8% retracement of the Apr/Jul rally.

- Despite USDJPY attempting to break back above 148.00 during the European morning, the pair tracks back around 147.50 as US GDP (2nd read) and PCE prints are awaited across Thursday and Friday.

- In emerging markets, more concrete details on a security deal being achieved between Mexico and the US provided a late boost for the Mexican peso. USDMXN had traded back up to resistance at 18.80 before the headlines, and the late dollar weakness provided an additional headwind for USDMXN, which trades back towards 18.69 approaching the APAC crossover.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SOFR OPTIONS: Midday Two-Way Trade

Jul-28 16:36

- -20,000 SFRZ5 95.25/95.62/96.12 call flys, 6.5

- -2,000 0QZ5 96.75 straddles 31.0 over 0QH6 97.12 calls ref 96.75/0.35%

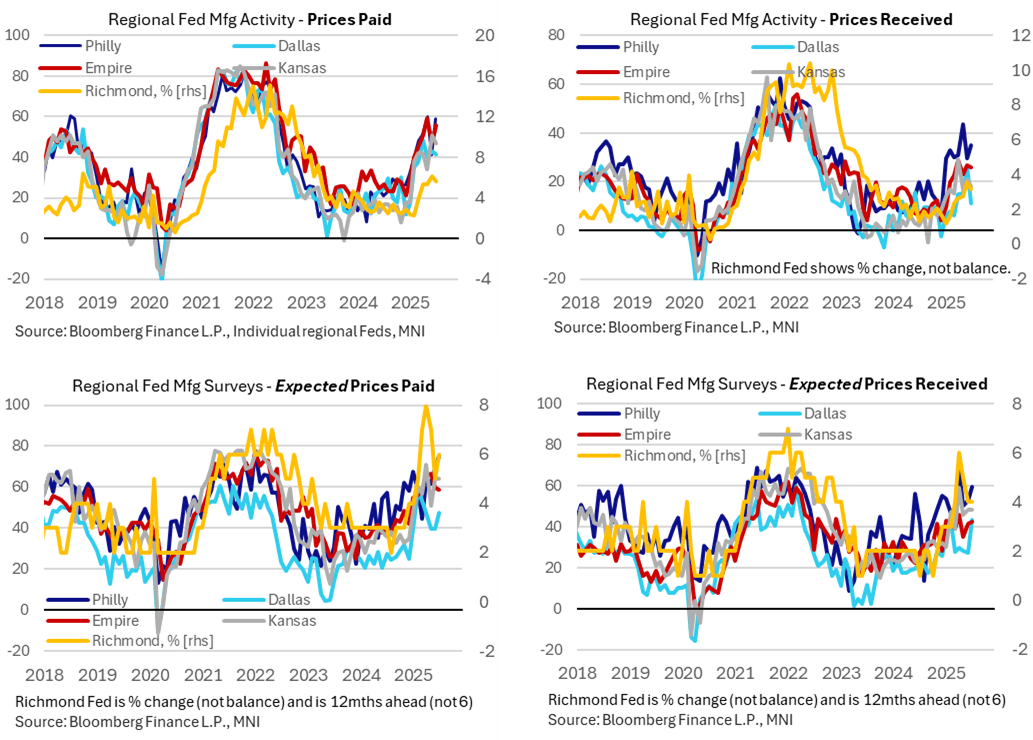

US DATA: Mixed Ability Of Firms To Pass Cost Increases On In Dallas Fed District

Jul-28 16:18

- The improvement in the Dallas Fed manufacturing survey for July came despite an apparent relative re-compression in margins although this in turn was countered by the opposite when looking six months out.

- The prices paid index remained at an elevated 41.7 after 43.0 in June (average of 43.5 since Apr 2 reciprocal tariff announcements, 30 in 1Q25 and 21 in 2024) but prices received dropped from 26.1 to 11.1 for the lowest since March (average 16.8 since Apr, 7 in 1Q25 and 7 in 2024).

- Countering this, the six-months ahead measures saw a marked increase in expectations for prices received with its highest since April 2022. The 43.2 compares with an average of 32 since April, 35 in 1Q25 and 21 in 2024.

- That said, whilst this uptick in expected prices received was a marked rise on the month, it’s only really catching up with relative levels seen in other regional Fed manufacturing surveys – see charts.

- Of course, whilst a particularly timely survey with a collection period of Jul 15-23, it still predates the US-EU deal made over the weekend with a 15% tariff rate on most EU goods (with the EU being the US’s largest source of imports).

US TSYS/SUPPLY: Preview 5Y Auction

Jul-28 16:15

- Tsy futures remain near mid-morning lows (FVU5 -3.5 at 108-04.25 vs. 108-03.5; TYU5 currently -6.5 at 110-25 vs. 110-24.5 low) ahead of the $70B 5Y note auction (91282CNN7) at 1300ET, WI is currently running at 3.981%, 10.2bp cheap to last month's tail.

- June auction recap: Tsy futures retreated slightly (FVU5 to 108-20.75 from 108-21.5) after the $70B 5Y note auction (91282CNK3) tailed: 3.879% high yield vs. 3.872% WI; 2.36x bid-to-cover vs. 2.39x prior (5 auction average).

- Peripheral stats: Indirect take-up retreated to 64.68% from 78.4% prior, directs bounced to 24.44% vs. 12.4% prior (5 auction low), primary dealer take-up at 10.88% vs. 9.2% prior.