US TSYS: US Tsys Tracked German Bund, French Oat Earlier, Extend Late Highs

- Tsys reversed early weakness - extended highs in 2s-10s - following German Bund and French Oat contracts. Sources posited real$ bought the early dip in OATS squeezing shorts with Bunds then Tsys reacting in short order on decent volumes.

- Dec'25 10Y contract tapped 112-15, just below technical resistance at 112-15+, the Aug 5 high and the bull trigger. Clearance of this hurdle would resume the uptrend and pave the way for a climb towards 112-19 initially, a Fibonacci projection.

- Tsy curves twist steeper: 2s10s +3.484 at 61.533 (nearing mid-April's 3Y highs), 5s30s +3.160 at 120.597.

- No reaction to MBA composite mortgage applications dip -0.5% (sa) last week after -1.4% the week prior as they still holds onto most of its refi-driven 11% increase before that. New purchase applications increased 2.2%, their largest increase in a month, whilst refi applications fell another -3.5% after -3.1% following the 23% jump before that.

- NY Fed President Williams (permanent FOMC voter) on CNBC doesn't sound particularly concerned about the state of the labor market, in particular downplaying the weak nonfarm payrolls growth implied by the July employment report's downward revisions.

- Uncertainty over an independent Federal Reserve aside (following Trump's "firing" of Fed Gov Cook late Monday) Trump seeking a majority of like minded Fed boardmen in the aftermath of Chairman Powell's dovish Jackson Hole speech appears to be emboldening risk takers as SPX emini and Nasdaq indexes made new highs (6502.50 and 21616.18 respectively)

- Look ahead to Thursday's session: Weekly Claims, GDP, PCE and US Tsy $44B 7Y Auction.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDCAD TECHS: Either Side of 50-day EMA

- RES 4: 1.3920 High May 21

- RES 3: 1.3862 High May 29

- RES 2: 1.3798 High Jun 23

- RES 1: 1.3729/74 50-day EMA / High Jul 17

- PRICE: 1.3730 @ 19:47 BST Jul 28

- SUP 1: 1.3557 Low Jul 03

- SUP 2: 1.3540 Low Jun 16 and the bear trigger

- SUP 3: 1.3503 1.618 proj of the Feb 3 - 14 - Mar 4 price swing

- SUP 4: 1.3473 Low Oct 2 2024

Despite a recovery from last week’s lows and a further phase of strength Monday, the trend needle in USDCAD continues to point south and short-term gains appear corrective. Markets have traded either side of resistance at 1.3728, the 50-day EMA. A clear break of this average is required to highlight a possible stronger short-term reversal. For bears, sights are on key support at 1.3540, the Jun 16 low. Clearance of this level would confirm a resumption of the downtrend.

AUDUSD TECHS: Approaching Support At The 50-Day EMA

- RES 4: 0.6700 76.4% retracement of the Sep 30 ‘24 - Apr 9 bear leg

- RES 3: 0.6688 High Nov 7 ‘24

- RES 2: 0.6677 0.764 proj of the Jun 23 - Jul 11 - 17 price swing

- RES 1: 0.6625 High Jul 24

- PRICE: 0.6517 @ 19:45 BST Jul 28

- SUP 1: 0.6513 Low Jul 28

- SUP 2: 0.6505/6455 50-day EMA / Low Jul 17

- SUP 3: 0.6373 Low Jun 23 and a bear trigger

- SUP 4: 0.6357 Low May 12

Last week’s fresh trend highs in AUDUSD reinforce bullish conditions and the latest pullback is considered corrective. Gains have resulted in a print above key short-term resistance at 0.6595, the Jul 11 high and bull trigger. This marks a resumption of the uptrend and sights are on 0.6688, the Nov 7’ 24 high. Support to watch is at the 50-day EMA, at 0.6505. A clear break of this EMA would highlight a stronger reversal.

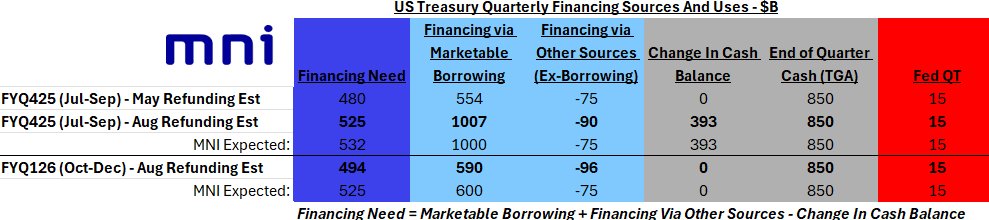

US TSYS/SUPPLY: Borrowing Requirements Upped In Line With MNI Expectations

Treasury's estimates of privately-held net marketable borrowing for the July - September 2025 and October - December 2025 quarters released Monday were almost exactly in line with MNI's estimates (Sources and Uses Table here - PDF).

- We would characterize the current quarter borrowing estimates as slightly on the high side of the median analyst expectation, with the latter quarter fairly close to expectations given what is usually a wide range for the further-out quarter. As such this should have little to no impact on expectations for Wednesday's Refunding announcement.

- For the Jul-Sep quarter, Treasury expects a $525B financing need (MNI expected $532B) with a $1007B borrowing requirement (MNI expected $1000B), with cash rising $393B to $850B by quarter-end (in line with consensus). Analyst borrowing requirement estimates for this quarter ranged from $942B - $1,087B.

- This represents a borrowing estimate $60B higher than announced in April's refunding, when excluding the cash raise that is now expected following the lifting of the federal debt limit ($453B more borrowing this quarter on $393B more cash by end-quarter).

- For the Oct-Dec quarter, Treasury expects a $494B financing need (MNI expected $525B) with a $590B borrowing requirement (MNI expected $600B), with cash remaining at $850B at quarter-end. Analyst borrowing requirement estimates for this quarter ranged from $534B - $726B.

- Note that regarding the April-June quarter, "excluding the lower than assumed end-of-quarter cash balance, actual borrowing was $56 billion lower than announced in April".