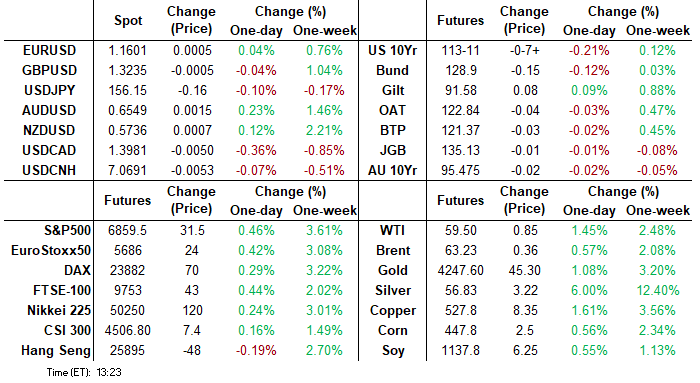

- Treasuries look to finish Friday's shortened post-Thanksgiving holiday session weaker across the board, volumes stepped up by the early close (TYH6 1.1M) despite the CME Group tech issue closure overnight.

- No obvious headline or flow driven trigger as Treasuries extend lows midmorning, TYH6 taps 113-09 low (-9.5) vs. 113-11 close, initial support below at 112-30, the 20-day EMA. Support at the 50-day EMA, lies at 112-25.

- Otherwise, a bullish theme in Treasuries remains intact and Tuesday’s gains reinforce current conditions. The recent breach of the 112-31 level, an area of congestion since Nov 5, marks an important short-term bullish development. This exposes 113-29+, the Oct 17 high and a key resistance

- Trading desks reported pre-emptive rate locks ahead corporate issuance next week as well as nascent month end selling ahead of today's early close at 1315ET.

- Reminder - the Fed enters policy blackout after midnight tonight through December 11, the day after the final FOMC of 2025. Monday look ahead: S&P Global Mfg PMI, ISM Mfg data.

MNI ASIA MARKETS ANALYSIS: Month-End FI Selling, Rate Locks

Nov-28 18:28By: Bill Sokolis

APAC+ 4

HIGHLIGHTS

- Treasuries look to finish Friday's shortened post-Thanksgiving holiday session weaker across the board, volumes stepped up by the early close (TYH6 1.1M) despite the CME Group tech issue closure overnight.

- There was a notable extension of greenback weakness into the month-end WMR fix, prompting fresh pullback lows for the DXY.

- Fed enters Blackout after midnight tonight, while Fed Chair Powell gives open remarks at memorial event late Monday, panel discussion (text, Q&A). Monday look ahead: S&P Global Mfg PMI, ISM Mfg data.

US TSYS

MNI US TSYS: Thanks Given for Early Market Close

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.05% (+0.04), volume: $3.297T

- Broad General Collateral Rate (BGCR): 4.02% (+0.05), volume: $1.288T

- Tri-Party General Collateral Rate (TCR): 4.02% (+0.05), volume: $1.258T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.88% (+0.00), volume: $89B

- Daily Overnight Bank Funding Rate: 3.88% (+0.00), volume: $171B

US SOFR/TREASURY OPTION SUMMARY

Liquidity challenged post-Thanksgiving holiday trade on Friday's shortened session: light SOFR options leaning on calls, scant Treasury options. Underlying futures weaker ahead the early close. Projected rate cut pricing steady in the near term vs. early morning (*): Dec'25 steady at -20.7bp, Jan'26 at -28.4bp, Mar'26 at -36.1bp (-36.5bp), Apr'26 at -43.4bp (-44.4bp).

SOFR Options:

+5,000 0QM6 96.00/96.25 put spd w/ 96.50/96.62 put spds, 5.0

+5,000 SFRZ5 96.31/96.37 2x1 put spds 1.0 ref 96.27

+2,000 SFRH6 96.43/96.56/96.68 call flys, 1.75 ref 96.45

+3,000 SFRZ5 96.12/96.18 put spds, 1.0 ref 96.27

-2,500 SFRF6 96.56 calls, 4.25 ref 96.45

+5,000 SFRZ5 96.31/96.43 call spds 0.75 ref 96.27

MNI FOREX: USD Index Prints Pullback Lows into Month-End, CAD Outperforming

- Despite a constructive start for the USD index on Friday, the week’s theme of a softer dollar took over across the US session. There was a notable extension of greenback weakness into the month-end WMR fix, prompting fresh pullback lows for the DXY. Sentiment this week has been bolstered by December easing expectations for the Fed, alongside speculation over a Hassett led FOMC next year prompting a dovish repricing further out the curve.

- Price adjustments across the G10 have been mixed Friday, perhaps owing to the lower volumes following the US thanksgiving holiday and an associated lack of conviction ahead of the weekend. However, outperformance for the Canadian dollar has certainly stood out.

- Canada's economy rebounded much faster than expected in the third quarter led by a drop in imports. USDCAD plumbed fresh lows for November on the headline data beat, and then extended below support at the 50-day EMA which intersected at 1.3995. The move south reached as low as 1.3939 into the WMR fix, exposing the base of a bull channel at 1.3923, drawn from the Jul 23 low.

- A solid rebound for NZDUSD also saw the pair reach recovery highs at 0.5744, extending the impressive bounce following the hawkish cut from the RBNZ this week. NZDUSD is threatening a close above its 50-day EMA, signalling scope for a stronger recovery to the medium-term pivot of 0.5800.

- GBPUSD has consolidated its post-budget squeeze, trading within a 1.3200-55 range Friday. While there have been some tepid reversal signs this week, plenty of fiscal concerns and likely BOE easing in December remain notable GBP headwinds, underpinning the dominant bearish theme.

- Perhaps to be expected USDJPY has traded in a much more contained manner this week, remaining within a 1% range. Spot is currently down just 25 pips from last Friday’s close, as firmer risk sentiment has been offset by the weaker greenback. Overall, the trend set-up in USDJPY remains bullish. The pair has recently entered overbought territory and a deeper retracement, if seen, would allow this condition to unwind. All focus turns to BOJ Governor Ueda’s speech to business leaders in Nagoya City on Monday.

MNI OPTIONS: Expiries for Dec01 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1525(E2.7bln), $1.1600(E1.5bln), $1.1795(E1.5bln)

- USD/JPY: Y155.00($744mln)

- GBP/USD: $1.2950(Gbp714mln)

- AUD/USD: $0.6550(A$522mln)

- USD/CAD: C$1.4025-30($1.1bln), C$1.4050($642mln)

MNI US STOCKS: Equities Roundup: Financials, Energy & Materials Outperform

- Stocks are holding moderate gains on Friday's shortened post-Thanksgiving holiday session - the DJIA, SPX emini and Nasdaq closing at 1300ET today.

- Currently, the DJIA trades up 298.41 points (0.63%) at 47723.77, S&P E-Mini Futures 23.75 points (0.35%) at 6851.75, Nasdaq up 81.9 points (0.4%) at 23296.93.

- Nascent month-end portfolio adjusting may be a supportive factor as Financials, Energy & Materials sector shares led advances ahead midday:

- Coinbase Global +3.66%, Block Inc +3.55%, Fiserv Inc +2.09%, JPMorgan Chase & Co +1.78% and Goldman Sachs Group +1.62%.

- EQT Corp +3.36%, Expand Energy +2.87%, ConocoPhillips +2.51%, Devon Energy +2.50% and Diamondback Energy +2.46%.

- Freeport-McMoRan +2.56%, Albemarle Corp +2.30%, Solstice Advanced Materials +1.56%, Corteva +1.43% and CF Industries Holdings In +1.17%

- Keeping advances in check, Health Care and Information Technology sector shares trade weaker:

Eli Lilly & Co -2.46%, Gilead Sciences -1.90%, Johnson & Johnson -1.32%, Incyte -1.19%, Baxter International -1.06% and GE HealthCare Technologies -1.03% - Oracle Corp-1.73%, NVIDIA Corp-1.51%, Dell Technologies -1.16% and Apple -0.33%.

MNI EQUITY TECHS: E-MINI S&P: (Z5) Bullish Recovery

- RES 4: 6953.75 High Oct 30 and bull trigger

- RES 3: 6900.50 High Nov 12

- RES 2: 6852.56 76.4% retracement of the Oct 30 - Nov 21 bear leg

- RES 1: 6856.75 High Nov 28

- PRICE: 6847.00 @ 1240 ET Nov 28

- SUP 1: 6674.50/6525.00 Low Nov 25 / 21

- SUP 2: 6500.00 Round number support

- SUP 3: 6476.62 23.6% retracement of the Apr 7 - Oct 30 uptrend

- SUP 4: 6427.00 Low Sep 2

S&P E-Minis are holding on to their latest gains following the recovery from the Nov 21 low. The climb has resulted in a breach of the 20- and 50- day EMAs. This highlights a bullish development and the likely end of the corrective cycle between Oct 30 and Nov 21. A continuation higher would signal scope for a move towards the key resistance and bull trigger at 6953.75, the Oct 30 high. Key support lies at 6525.00, the Nov 21 low.

MNI COMMODITIES: First Short-Term Bull Trigger for Gold at $4245.23

Recent weakness in WTI futures highlights a bearish theme. A resumption of the bear leg would open the key support and the bear trigger at $55.99, the Oct 20 low. Clearance of this level would resume the downtrend. Note that it is still possible a bullish corrective cycle remains in play. The contract has recovered from its latest low, resistance to watch is $61.84, the Oct 24 high. A clear break of this hurdle would signal scope for a stronger correction. The trend condition in Gold remains bullish and the bear phase between Oct 20 and 28 appears to have been a correction. This allowed a recent overbought condition to unwind. Key support to watch lies at the 50-day EMA, at $3981.6. Clearance of this EMA would signal scope for a deeper retracement. The first short-term bull trigger has been defined at $4245.23, the Nov 13 high.

- WTI Crude up $0.43 or +0.73% at $59.08

- Natural Gas up $0.09 or +2.02% at $4.65

- Gold spot up $15.39 or +0.37% at $4174.26

- Copper down $1 or -0.19% at $518.4

- Silver up $0.48 or +0.9% at $53.8493

- Platinum up $27.94 or +1.73% at $1642.19

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 01/12/2025 | 0730/0830 | ** | Retail Sales | |

| 01/12/2025 | 0815/0915 | ** | S&P Global Manufacturing PMI (f) | |

| 01/12/2025 | 0845/0945 | ** | S&P Global Manufacturing PMI (f) | |

| 01/12/2025 | 0850/0950 | ** | S&P Global Manufacturing PMI (f) | |

| 01/12/2025 | 0855/0955 | ** | S&P Global Manufacturing PMI (f) | |

| 01/12/2025 | 0900/1000 | ** | S&P Global Manufacturing PMI (f) | |

| 01/12/2025 | 0930/0930 | ** | BOE Lending to Individuals | |

| 01/12/2025 | 0930/0930 | ** | BOE M4 | |

| 01/12/2025 | 0930/0930 | ** | S&P Global Manufacturing PMI (Final) | |

| 01/12/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 01/12/2025 | 1445/0945 | *** | S&P Global Manufacturing Index (final) | |

| 01/12/2025 | 1500/1000 | *** | ISM Manufacturing Index | |

| 01/12/2025 | 1530/1530 | DMO to hold FQ4 consultations with investors / GEMMs | ||

| 01/12/2025 | 1530/1530 | BOE Dhingra Keynote at UK Trade Policy Observatory | ||

| 01/12/2025 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 01/12/2025 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 02/12/2025 | 0001/0001 | * | BRC Monthly Shop Price Index | |

| 02/12/2025 | 0030/1130 | * | Building Approvals | |

| 02/12/2025 | 0030/1130 | Balance of Payments: Current Account |