MNI ASIA MARKETS ANALYSIS: Mid-East Tensions Lend Tsy Support

HIGHLIGHTS

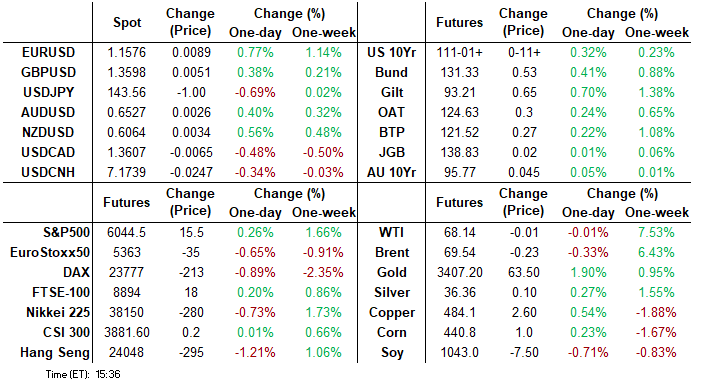

- Treasuries climb off early lows following rise in weekly & continuing jobless claims, geopolitical risk stemming from the Middle East and a strong 30Y bond auction re-open added support.

- A returning soft-USD theme continued to dictate proceedings in the FX space on Thursday, with markets extending the post US-CPI trend, bolstered by Trump's confirmation of incoming unilateral tariffs on countries without a trade deal.

- Curve flattening rally in rates helped projected rate cut pricing gain in the long end with Dec'25 pricing in just over a full 50bp in cuts.

US TSYS

MNI US TSYS: Rise in Weekly/Continuing Jobless Claims Lends to Early Rate Support

- Treasuries look to finish near session highs set after this morning's weekly and continuing jobless claims came out higher than expected, PPI inflation metrics more in-line with expectations. Rates gained additional risk-off support after wires reported that Israel was "considering military action against Iran" in coming days.

- At the moment, Sep'25 10Y futures trade +11 at 111-01 vs. 111-06 high, just off initial technical resistance at 111-14.5 (High Jun 5 & 61.8% of the May 1 - 22 downleg).

- Headline final demand PPI reading of 0.13% M/M was below the 0.2% expectation, and while that's offset by a decent upward revision to April (-0.24% from -0.47%), the overall index remains below its January level in seasonally adjusted terms, and up just 2.6% Y/Y.

- Initial jobless claims: 248k (sa, cons 242k) in the week to Jun 7 after a marginally upward revised 248k (initial 247k). Continuing claims: 1956k (sa, cons 1910k) in the week to May 31 after a marginally downward revised 1902k (initial 1904k).

- US $22B 30Y Bond auction re-open stopped through on decent demand, awarded 4.844% high yield vs. 4.859% WI; 2.43x bid-to-cover vs. 2.31x in the prior month.

- Focus turns to Friday's UofM sentiment and 1Y/5-10Y inflation expectations.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.28% (+0.00), volume: $2.600T

- Broad General Collateral Rate (BGCR): 4.27% (+0.00), volume: $1.075T

- Tri-Party General Collateral Rate (TCR): 4.27% (+0.00), volume: $1.042T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $111B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $282B

FED Reverse Repo Operation

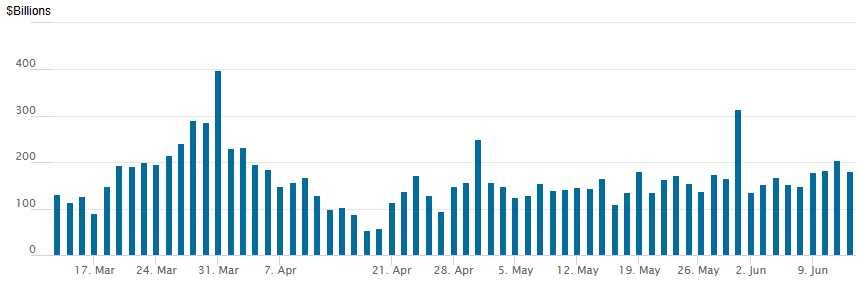

RRP usage retreats to $181.417B this afternoon from $204.625B yesterday, total number of counterparties at 34. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury puts turn mixed on larger volumes in the second half, vol buyers via 10Y straddles in Treasury options. Underlying futures holding near the top end of the range after this morning's data, projected rate cut pricing gaining out the curve vs. morning levels (*) as follows: Jun'25 at -0.8bp, Jul'25 at -5.9bp (-5.1bp), Sep'25 at -23.2bp (-21.8bp), Oct'25 at -35.9bp (-35.1bp), Dec'25 at -52.3bp (-51.9bp).

SOFR Options

-40,000 SFRH6 95.00/95.50 put spds, 1.25 ref 96.40

Block, 3,250 0QQ5 96.18/96.37 3x2 put spds, 4.0 net ref 96.70

Block, 19,500 SFRM5 95.68/95.75/95.81/95.87 put condors, 0.25 net/wings over ref 95.6925

+5,000 SFRN5 96.50/97.00 call spds, 0.75 ref 95.92

+5,000 SFRU5 95.56 puts, 0.5

over 41,000 0QM5 95.56 calls in pieces overnight from 2.5-4.0

2,500 0QM5 96.43/96.50/96.56/96.68 broken call condors ref 96.57

+6,000 SFRV5 96.1875/96.3125/96.4375 call fly, 1.0

+2,000 SFRM5 95.75 puts. 0.75

2,200 SFRM5 95.68 puts ref 95.6875

4,000 SFRN5 95.75 puts, 0.75 last

-2,000 SFRZ5 96.37/96.50 call spds vs. 95.75/95.87 put spd, 1.5 net

6,125 SFRN5 95.81/95.93/96.06 put flys ref 95.90

2,000 SFRX5 96.25/96.68 call spds ref 96.175

1,000 SFRU5 95.68/95.87/96.00 put flys ref 95.895

Treasury Options

Block, +11,100 TYN5 111 straddles, 50 ref 110-22, more on screen

+7,000 TYN5/TYQ5 111 straddle spd, 104-105 Aug bought over

over 8,100 USQ5 115/117/118 broken call trees ref 114-07

2,500 USN5 114.5/116 1x2 call spds

-7,500 USU5 103/107 put spds 20-19 ref 113-27

-2,500 USU5 103/107 put spd, 20

+3,000 wk2 TY 111.25 calls, 5

Block +12,000 Mon wkly TY 111.5 calls, 5

+6,000 Mon wkly TY 111.25 calls, 8

+1,500 TYU5 111/112.5/114 call flys, 16

+4,000 TYQ5/TYU5 110.5put spd, 17

-2,500 FVN5 108.25 calls, 12

+5,000 wk2 TY 111/111.25/111.5/111.75 call condors, 3 vs. 110-25 to -26

+3,000 TYN5 111.75 calls, 6

+5,000 TYN5 112 calls, 3

Block, 5,000 TYN5 111.5 calls vs. TYQ5 108.5 puts, 5 net cr/put sold over

+1,500 TYU5 107/109/110 put trees, 9 ref 110-23

MNI BONDS: EGBs-GILTS CASH CLOSE: Multiple Factors Drive Bull Flattening

Bund and Gilt yields dropped Thursday for the 3rd time in 4 sessions this week.

- UK monthly activity came in weaker than expected, boosting Gilts early, while EGB curves bull flattened on news of proposal for a 12-month phase-in period for Dutch pension reforms.

- Weak US jobless claims and soft producer prices saw core instruments hit the best levels of the session, with momentum largely carrying through to the cash close.

- Both the German and UK curves held bull flatter, with Gilts outperforming Bunds.

- Periphery / semi-core EGB spreads closed a little wider.

- Friday's calendar includes UK consumer survey and Eurozone industrial production / trade balance figures, while there will also be appearances by ECB's Nagel and Cipollone.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 2.9bps at 1.816%, 5-Yr is down 4.7bps at 2.079%, 10-Yr is down 5.7bps at 2.478%, and 30-Yr is down 7.3bps at 2.932%.

- UK: The 2-Yr yield is down 4.7bps at 3.866%, 5-Yr is down 5.8bps at 3.985%, 10-Yr is down 7.5bps at 4.477%, and 30-Yr is down 8.5bps at 5.193%.

- Italian BTP spread up 1.6bps at 92.7bps / Greek up 3.1bps at 74.5bps

MNI EGB OPTIONS: Euro Rates Upside Remains Prevalent

Thursday's Europe rates/bond options flow included:

- ERU5 98.25/98.50cs, bought for 2.25 in 15k

- ERU5 98.875c, bought for more at 0.25, now in another 10k (at least 30k bought this week)

- ERZ5 98.31/98.43 cs vs 97.93 put, buys the cs for 2.25 in 11k

- ERH6 98.1875/98.00ps, 1x1.5, bought for 5.25 in 2k

- ERH6/0RH6 98.375/98.625cs spread, bought for 0.75 (0.675 synth) in 10k Total

- SFIU5 96.00/96.20/96.40c fly, sold at 7.75 down to 7.50 in 10k

MNI FOREX: Soft Data Further Weighs on USD, Weaker Theme Prevailing

- A returning soft-USD theme continued to dictate proceedings in the FX space on Thursday, with markets extending the post US-CPI trend, bolstered by Trump's confirmation of incoming unilateral tariffs on countries without a trade deal. Furthermore, soft PPI readings for May and a high jobless claims figure further dented greenback sentiment, allowing the USD index to reach bearish cycle extremes.

- Most notable was the strengthening impact on the Euro, as EURUSD broke the bull trigger at 1.1573 and rose to a fresh high of 1.1631, the highest level since late 2021. Above here, 1.1685 provides the next target for the move, the 76.4% retracement of the Jan ‘21 - Sep ‘22 downleg.

- Softer risk sentiment stemming from increased geopolitical tensions around Iran have relatively weighed on the high beta currencies, and the likes of AUD and NZD in G10 and the emerging market FX basket have relatively underperformed. President Trump talked down the likelihood of a nuclear deal with Iran, and reports continue to circulate of a potential Israeli operation on the region to stem Tehran's nuclear ambitions.

- A poor monthly GDP release from the UK works further in favour of a sell-on-rallies theme for GBP, but this appears most beneficial for the crosses given the broad dollar weakness. This has prompted the EURGBP recovery to briefly extend to as much as 1.42% in just three sessions. Price action has been exacerbated by a break of resistance at 0.8442, the 50-day EMA, and the cross briefly pierced the May 2 high, printing 0.8547.

- Friday’s data focus will be on the UK quarterly consumer BOE/Ipsos Inflation Attitudes Survey, before Eurozone IP and trade balance figures. US prelim UMich sentiment and inflation expectations are also due.

MNI FX OPTIONS: Expiries for Jun13 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1400-05(E1.7bln), $1.1485-00(E2.0bln)

- USD/JPY: Y144.00($1.3bln)

- EUR/GBP: Gbp0.8475(E902mln)

MNI US STOCKS: Late Equities Roundup: Near Highs, Software & Pharmaceuticals Leading

- Stocks continue to drift in mildly positive territory late Thursday, this morning's post claims data support tempered by geopolitical tensions after Israel stated it was "considering military action against Iran" in coming days. Currently, the DJIA trades up 64.43 points (0.15%) at 42930.33, S&P E-Minis up 14 points (0.23%) at 6043.5, Nasdaq up 31.3 points (0.2%) at 19647.62.

- Information Technology and Health Care sectors continued to outperform in late trade, the former driven by software and services over chip makers for once: Oracle surged 13.35% on upbeat Q4 results on growing AI prospects, Gen Digital +3.09%, Palo Alto Networks +2.01% and ON Semiconductor +1.93%.

- Pharmaceuticals rebounded after trading weaker the last couple sessions: Cardinal Health +4.75%, Cencora +2.48%, United Health Groups +1.89%, Merck & Co +1.86%.

- On the flipside, Communication services continued to underperform in late trade: Fox Corp -2.42%, Match Group -2.35%, Paramount -2.08% and Live Nation Entertainment -1.25%.

- Meanwhile, the Industrials sector was weighed down by airlines following news of a Air India 787 jet crash overnight, killing most of the 242 on board: Boeing -4.67%, United Airlines -1.63%, Southwest Airlines -2.591% and Delta Air Lines -0.77%.

MNI EQUITY TECHS: E-MINI S&P: (M5) Bulls Remain In The Driver’s Seat

- RES 4: 6172.38 1.500 proj of the Apr 7 - 10 - 21 price swing

- RES 3: 6124.00 High Feb 24

- RES 2: 6080.75 High Feb 26

- RES 1: 6074.75 High Jun 11

- PRICE: 6018.00 @ 14:40 BST Jun 12

- SUP 1: 5921.50/58160.70 20- and 50-day EMA values

- SUP 2: 5756.50 Low May 23

- SUP 3: 5596.00 Low May 7

- SUP 4: 5455.50 Low Apr 30

The trend condition in S&P E-Minis remains bullish and the contract traded to a fresh cycle high yesterday, reinforcing current bullish conditions. The recent break of 5993.50, the May 20 high and a bull trigger, highlights a resumption of the uptrend and maintains a price sequence of higher highs and higher lows. Sights are on 6080.75 next, the Feb 26 high. Key support to watch lies at 5816.70, the 50-day EMA.

MNI COMMODITIES: WTI Edges Higher Amid Middle East Tensions, Gold Extends Gains

- WTI has risen today amid ongoing geopolitical tensions in the Middle East, with latest headlines suggesting that Israel is considering military action against Iran in the coming days.

- WTI Jul 25 is up by 0.3% at $68.3/bbl.

- Meanwhile, newswires have reported confirmation that President Trump's special envoy to the Middle East, Steve Witkoff, will travel to Oman on Sunday to attend the 6th round of US-Iran nuclear talks.

- For WTI futures, yesterday’s strong gains mark an acceleration of the current bull phase. The contract has cleared all key retracement points of the Apr 2 - 9 bear leg and this signals scope for an extension towards $71.10 the Apr 2 high and a key hurdle for bulls.

- On the downside, initial firm support to watch is $63.25, 50-day EMA.

- Meanwhile, spot gold has extended this week’s gains, rising by another 0.8% today to $3,384/oz.

- The move takes total gains this week to 2.2%, with the yellow metal benefitting from haven demand amid the increase in geopolitical tensions and a weaker dollar following soft US inflation data.

- A bullish theme in gold remains intact, and an extension higher would open $3,435.6 next, the May 7 high. A break of this hurdle would strengthen bullish conditions.

- On the downside, support to monitor is $3,255.0, the 50-day EMA.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 13/06/2025 | 0600/0800 | *** | Final Inflation Report | |

| 13/06/2025 | 0600/0800 | *** | HICP (f) | |

| 13/06/2025 | 0645/0845 | *** | HICP (f) | |

| 13/06/2025 | 0700/0900 | *** | HICP (f) | |

| 13/06/2025 | 0830/0930 | ** | Bank of England/Ipsos Inflation Attitudes Survey | |

| 13/06/2025 | 0900/1100 | ** | Industrial Production | |

| 13/06/2025 | 0900/1100 | * | Trade Balance | |

| 13/06/2025 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 13/06/2025 | 1230/0830 | ** | Wholesale Trade | |

| 13/06/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 13/06/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 13/06/2025 | 1500/1700 | ECB Elderson At Senior Supervisor's Conference | ||

| 13/06/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 13/06/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |