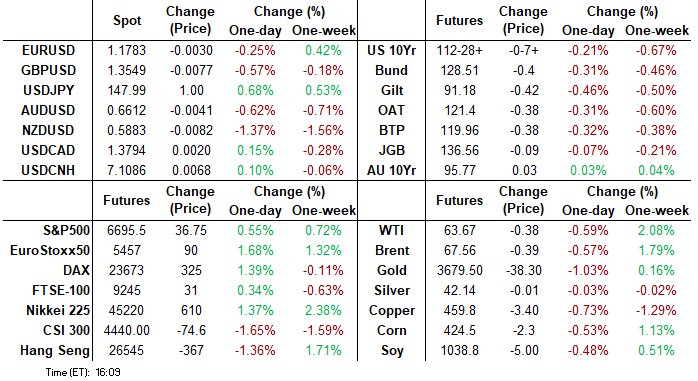

MNI ASIA MARKETS ANALYSIS: Hedging For More Rate Cuts

HIGHLIGHTS

- Treasuries reversed early gains/extended lows after this morning's better than expected weekly and continuing jobless claims.

- Curves bear steepened and derivatives hedging centered on more year end rate cuts than currently priced (-45.2bp for December).

- Major US equity indexes extended record highs in the first half, drew late day profit taking as indexes scaled off highs.

- Both the Bank of England vote split and APF reduction were in line with expectations provided little fresh impetus for GBP (-0.51%) on Thursday, allowing cable to suffer from broader dynamics.

US TSYS

MNI US TSYS: Treasury Yields Rising As Weekly Jobless/Continuing Claims Improve

- Treasuries look to finish weaker but off early Thursday lows. Rates traded firmer overnight - paring Wednesday's post-FOMC sell-off - but reversed course/extended lows after better than expected weekly & continuing claims.

- Initial jobless claims were lower than expected at 231k (sa, cons 240k) in the week to Sep 13, a payrolls reference week. It follows a marginally upward revised 264k (initial 263k) in what was a much higher than expected print at the time after a spike in Texas initial claims in what has since been revealed as linked to ID fraud that has increased since Labor Day.

- Continuing claims meanwhile also offer a relatively encouraging report, easing to 1920k (sa, cons 1950k) in the week to Sep 6 after yet another downward revision to 1927k (initial 1939k).

- After the bell the Tsy Dec'25 10Y contract trades -6.5 at 112-29.5 (yld 4.1140% +.0269) vs. 112-23.5 low (113-12 o/n high) - initial technical support at 112-15.5 (High Aug 5 and 14). Curves steeper: 2s10s +.833 at 54.026, 5s30s +2.156 at 105.571.

- Information Technology sector shares led equity indexes run to new highs - namely semiconductor makers after Intel surged nearly 30% to new 52-wk highs of 32.37 after Nvidia (+3.31% - recovering from Wednesday's decline) announced a $5B investment and AI infrastructure collaboration.

- Both the Bank of England vote split and APF reduction were in line with expectations provided little fresh impetus for GBP (-0.51%) on Thursday, allowing cable to suffer from broader dynamics.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.38% (-0.01), volume: $2.853T

- Broad General Collateral Rate (BGCR): 4.35% (-0.01), volume: $1.149T

- Tri-Party General Collateral Rate (TCR): 4.35% (-0.01), volume: $1.125T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $96B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $192B

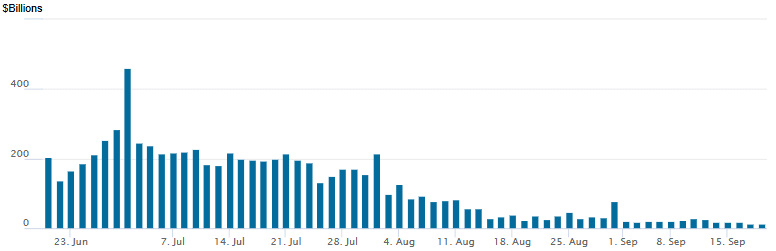

FED Reverse Repo Operation

RRP usage slips to new low of $13.707B with 13 counterparties this afternoon from $13.963B Wednesday, usage at lowest levels since early April 2021. Compared to this year's high usage of $460.731B occurred on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury option flow remained mixed on net while the direction of trade reversed around miidday from better puts to upside calls as underlying futures pared losses. Note: *large scale seller of SOFR call fly calendar hedging a shift in more rate cuts by year end. Projected rate cut pricing largely steady vs. early morning levels (*): Oct'25 at -21.8bp (-22.2bp), Dec'25 at -43.9bp (-44.3bp), Jan'26 at -56.5bp (-57.3bp), Mar'26 at -70.1bp (-71.6bp).

SOFR Options:

*-20,000 SFRV5 96.25/96.50/96.62 call flys vs. SFRZ5 96.31/96.50/96.62 call flys, 3.5 to 2.75

+2,000 SFRU7 97.00 straddles, 88.0 ref 96.955

-1,500 SFRZ5 96.25/96.43 strangles, 9.5

+15,000 SFRZ5 96.18/96.31/96.50/96.62 call condors, 7.0 ref 96.35

+3,000 SFRU6 96.25 puts, 6.0 ref 96.82/0.14%

-25,000 2QH6 98.00/98.25 call spds, 0.5

Block, 9,500 SFRZ5 96.50 calls, 2.75 vs. 96.32/0.20%

+6,000 SFRZ5 96.25/96.37/96.50/96.62 call condors, 6.5-6.25

-10,000 0QH6 97.37/97.62 call spds 5.25

+5,000 SFRZ5 96.43/96.50/96.56/96.68 broken call condors, 0.5

+5,000 0QV5 96.62/96.81/96.87/97.00 put trees, 3.0

+5,000 SFRZ5 95.87/96.00 put spds, 0.5

4,000 SFRH6 96.25/96.62 2x1 put spds ref 96.615

10,000 SFRH6 96.18/96.31/96.43/96.62 call condors ref 96.615

+16,000 SFRZ5 95.75/95.81/95.87/95.93 put condors, cab ref 96.365

25,000 SFRZ5 95.81/95.87/95.93 put trees, 0.0 ref 96.365

appr +40,000 SFRZ5 95.87 puts, cab

3,000 SFRZ5 96.12 puts, ref 96.365

1,500 0QH6 96.50/96.87/97.00 broken put trees, 1.5 vs. 97.075/0.08%

Block, 5,000 SFRZ5 95.93/96.06 put spds, 0.75 ref 96.36

+5,000 SFRZ5 96.06/96.18 put spds, 2.0 ref 96.37

+2,000 0QZ5 96.75/96.87/97.12 broken put trees vs. 97.37 calls, 0.0 net ref 97.065

3,000 SFRZ5 95.87/96.12 put spds vs. 6,000 95.93/96.06 put spds

(note: Wed's -100k+ 0QZ5 9700/9725 call spds mostly at 10: closer with OI -91k & 70k respectively)

Treasury Options:

+10,000 TYX5 113.5/TYV5 114.25 call diagonal spds, 25 net ref 112-26.5

+10,000 TYX5 112.5/113.5 strangles, 60

+4,000 TYV5 113.25 puts, 17 ref 113-10.5

1,500 TYV5 113/113.5 call spds, 19 ref 113-09.5

Block/screen, over +87,700 TYV5 115.25 calls, 1 vs. 113-13.5 to -15/0.02% (OI 57,393)

-3,000 FVX5 111.5 calls, 3.5 vs. 109-23.75/0.09%

3,500 FVV5 109.75 calls, 5 ref 109-16.75

-2,000 TYV5 110.5/111 straddle strip

over -11,300 FVV5 109.5 puts, 6.5-6.0

-3,000 TYX5 112/113 put spds, 20-21

+4,000 TYV5 112 puts, 1

-4,000 TYX5 111 puts, 5

1,850 TYV5 113.5 calls ref 113-04

MNI BONDS: EGBs-GILTS CASH CLOSE: Bear Steeper As BOE Delivers Expected Hold

European curves bear steepened Thursday.

- Early trade saw limited moves in EGBs and Gilts, with little net impact from the Federal Reserve decision the previous day after the cash close.

- The BOE decision (7-2 vote for a hold) was fully as expected, though there was a bit of twist steepening subsequently seen in the UK curve as the front-end faded a pre-meeting buildup of hawkish positioning.

- Stronger-than-expected US jobless claims data saw a sell-off in Treasuries spill over into Europe.

- In an interview later in the session, BOE's Bailey pointed to ongoing expectations for further rate cuts, while assuaging fears over the impact of QT, helping limit Gilt losses going into the close.

- ECB Vice President de Guindos told an MNI Connect event that the risk of persistent inflation undershooting is not that big.

- The German and UK curves both bear steepened on the day, with little difference in performance. Periphery / semi-core EGB spreads were little changed.

- Friday concludes a busy week for the UK with retail sales and public sector finance data, while we also get French confidence data.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.7bps at 2.011%, 5-Yr is up 2.7bps at 2.306%, 10-Yr is up 5.1bps at 2.726%, and 30-Yr is up 7.9bps at 3.309%.

- UK: The 2-Yr yield is up 0.2bps at 3.961%, 5-Yr is up 2.9bps at 4.103%, 10-Yr is up 5.1bps at 4.676%, and 30-Yr is up 7.7bps at 5.507%.

- Italian BTP spread up 0.7bps at 79.7bps / French OAT up 0.2bps at 80.8bps

MNI EGB OPTIONS: Upside Structures In Sonia Prevalent After BOE Rate Hold

Thursday's Europe rates/bond options flow included:

Pre-BOE decision:

- RXV5 129.50c vs RXX5 130.50c calendar spread, bought the Nov for 9 in 2.1k.

- RXV5/RXX5 130c calendar spread, bought the Nov for 29 in 4.2k.

Post-BOE decision:

- ERU6 97.81/97.68/97.56/97.43p condor, bought for 1.5 in 2.5k

- ERU6 98.25/98.50cs x1 vs ERU6 97.93p x0.5, bought the cs for half in 10k

- SFIZ5 96.15/96.25/96.30/96.40C Condor, bought for 2.25 in 4k

- SFIH6 96.40/96.60cs , bought for 4.5 in 2k

- SFIH6 96.40/96.60/96.80c fly, bought for 3 in 3k

- SFIH6 96.60/96.75cs, bought for 1.5 in 10k

- SFIM6 96.45/96.75cs , bought for 8.75 in 5k

- SFIM6 96.45/96.75 call spread paper paid 8.75 on 5K (vs. 40).

- SFIZ5 96.30/96.55/96.80c fly, sold at 0.75 in 11.5k

MNI FOREX: Greenback Relief Rally Extends Following Strong US Data

- The lack of conviction on the FOMC about the rate path forward was a key theme of the September meeting’s release materials, as well as Chair Powell’s press conference. This prompted the USD’s bearish momentum to stall on Wednesday and aggressively reverse higher.

- Better-than-expected US jobless claims and Philly fed data then bolstered the relief rally Thursday. At its highest point today, USDJPY (+0.70%) recovered by an impressive 278 pips from the post-Fed lows, potentially exacerbated by the lingering political uncertainty in Japan, the close proximity to the BOJ meeting Friday and a bullish reversal signal on the chart.

- The New Zealand dollar is the standout underperformer in the G10 space, following a particular weak set of Q2 GDP data overnight. The much weaker-than-expected growth figures have weighed heavily on the Kiwi, currently down 1.4% as we approach the APAC crossover, placing the renewed short-term focus on pivot support at the 0.5800 mark.

- The NZ data trumped the weaker-than-expected August employment change figure out of Australia, which has notably allowed AUDNZD to extend its impressive rally from the April lows to ~5.9%.

- Price action today has seen the cross rise above 1.12 for the first time since late 2022 and steady appreciation saw spot eclipse the next target for the move of 1.1250, the 76.4% Fibonacci retracement of the 2022 price swing. Above here, resistance appears scant until the 2022 highs, located at 1.1491.

- Both the Bank of England vote split and APF reduction coming in line with expectations provided little fresh impetus for GBP (-0.51%) on Thursday, allowing cable to suffer from broader dynamics. A bullish theme for cable remains intact and the move down from Wednesday’s high is considered corrective at this juncture, with a deeper retracement potentially allowing an overbought condition to unwind. Initial firm support to watch is 1.3492, the 50-day EMA.

- Aside from the BOJ decision and press conference, UK and Canadian retail sales highlight Friday’s data calendar.

MNI US STOCKS: Late Equities Roundup: Holding Near Record Highs, Late Profit Taking

- Stocks continue to drift near new record highs set earlier Thursday - following this morning's better than expected weekly jobless claims and carry-over support from Wednesday's rate cut spurring expectations for more before year end.

- Currently, the DJIA trades up 115.13 points (0.25%) at 46131.34 vs. 46317.52 record high, S&P E-Minis up 38 points (0.57%) at 6696.75 vs. 6719.75 record high, Nasdaq up 234.2 points (1.1%) at 22494.41 vs. 22540.93 record high.

- Information Technology sector shares continued to lead gainers in the second half, namely semiconductor makers after Intel surged nearly 30% earlier to a new 52-wk highs of 32.37 after Nvidia (+3.56% - recovering from Wednesday's decline) announced a $5B investment and AI infrastructure collaboration.

- Other chipmakers benefitting from the news included: Synopsys +12.27%, KLA +6.12%, Applied Materials +6.04%, Palantir Technologies +5.47% and Micron Technology +5.41%.

- Meanwhile, a mix of Industrial and Utility sector shares followed: Quanta Services +3.89%, Cummins +3.75%, Caterpillar +3.19%, AES Corp +3.32%, Vistra Corp +1.95% and Constellation Energy +1.24%.

- Leading decliners in the second half included Consumer Staples and Energy sector shares: Philip Morris Int -2.43%, Monster Beverage -1.77%, Altria Group -1.66% and Procter & Gamble -1.59% weighed on the former, while the Energy sector was weighed down by APA Corp -1.78%, EQT Corp -1.66%, Devon Energy -1.52% and Phillips 66 -1.37%.

MNI EQUITY TECHS: E-MINI S&P: (Z5) Northbound

- RES 4: 6787.63 1.382 proj of the Aug 1 - 15 - 20 price swing

- RES 3: 6750.50 2.000 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 2: 6748.50 1.236 proj of the Aug 1 - 15 - 20 price swing

- RES 1: 6719.75 Intraday high

- PRICE: 6701.50 @ 1452 ET Sep 18

- SUP 1: 6578.36 20-day EMA

- SUP 2: 6536.50 Low Sep 8

- SUP 3: 6468.72 50-day EMA

- SUP 4: 6417.25 Low Aug 12

A bull cycle in S&P E-Minis remains intact and the contract has today traded to a fresh cycle high. Price has breached the 6700.00 handle and this signals scope for an extension towards 6748.50, a Fibonacci projection point. Moving average studies remain in a bull-mode position, highlighting a dominant uptrend and positive market sentiment. Initial support to watch lies at 6578.36, the 20-day EMA.

MNI COMMODITIES: Crude Falls, Gold Edges Lower Amid Dollar Relief Rally

- WTI has fallen today after Bloomberg reported that the EC may be more focused on targeting Russian LNG, rather than oil, in its latest sanctions package.

- The EC is considering the phasing out of all Russian LNG imports earlier than the end of 2027, which was the EU’s initial plan. Its focus is turning to Russian LNG, given that many EU countries are reluctant to hit India and China with tariffs for purchases of Russian oil.

- WTI Oct 25 is down by 0.8% at $63.5/bbl.

- Meanwhile, the market is weighing the pledged rise in OPEC+ output against the bloc’s spare capacity to follow through on production hikes, coupled with Chinese storage buying.

- The trend condition in WTI futures is still bearish, with initial support at $61.29, the Aug 13 low and the bear trigger, followed by $57.71, the May 30 low. Initial resistance to watch is $66.03, the Sep 2 high.

- Elsewhere, spot gold has fallen by 0.5% to $3,642/oz, as a relief rally in the dollar, bolstered by better-than-expected US data, weighed on the yellow metal.

- Despite the move, the trend structure for gold remains bullish and short-term weakness is for now, considered corrective.

- Another all-time high, earlier this week, confirmed a resumption of the primary uptrend and an extension of the sequence of higher highs and higher lows. The next objective is $3,705.2, a Fibonacci projection. Initial firm support lies at $3,566.4, the 20-day EMA.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 19/09/2025 | 0600/0700 | *** | Public Sector Finances | |

| 19/09/2025 | 0600/0700 | *** | Retail Sales | |

| 19/09/2025 | 0600/0800 | ** | PPI | |

| 19/09/2025 | 0645/0845 | ** | Manufacturing Sentiment | |

| 19/09/2025 | 1005/1205 | ECB Lagarde and Cipollone at Eurogroup ECOFIN Meeting | ||

| 19/09/2025 | 1230/0830 | ** | Retail Trade | |

| 19/09/2025 | 1230/0830 | ** | Retail Trade | |

| 19/09/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 19/09/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 19/09/2025 | 1830/1430 | San Francisco Fed's Mary Daly |