MNI ASIA MARKETS ANALYSIS: Hawkish Fed Sentiment Weighs

MNI (NEW YORK) -

HIGHLIGHTS:

- A volatile session saw early equity losses reverse, with the S&P 500 closing flat

- Treasuries softened to end the week, with early safe-haven driven gains dissipating and the cash curve ending bear steeper

- Duelling reports on the state of UK government finances triggered a wide range for both spot GBP and Gilt yields

- September's US nonfarm payrolls report has been rescheduled for next Thursday but no word on other major data releases

US TSYS: Softer To End The Week As Intraday Rally Reverses

Treasuries softened to end the week, with early gains dissipating and the cash curve ending bear steeper.

- An overnight selloff in Gilts related to UK fiscal concerns spilled over lightly into the US in early trade, but maintained a cautious tone for Treasuries following on from Fed commentary earlier in the week dampening enthusiasm for a December rate cut as well as weak long-end Treasury auctions.

- However a pullback in equities was enough to provide a safe-haven bid in equities which saw TY futures briefly touch the best levels of November so far. That would reverse however, with equities finding their footing and turning higher for the day and returning Treasuries to early morning levels.

- With the federal government shutdown now over, some postponed data is starting to come into view, with the BLS scheduling September's delayed nonfarm payrolls report for next Thursday, and the Census Bureau set to publish some delayed August data next week.

- Still, there's no official word on the fate of the October CPI release, which looks very likely to be cancelled altogether, or the date of the October employment report's publication (which is likely to see an establishment survey but not a household one).

- Against this backdrop, Friday's Fed commentary (with the usual exception of Gov Miran calling for further easing in December) was roundly hawkish, with Dallas's Logan and KC's Schmid reiterating their opposition to a December rate cut, largely out of concern over entrenched inflation. A December cut remained around 50/50 priced.

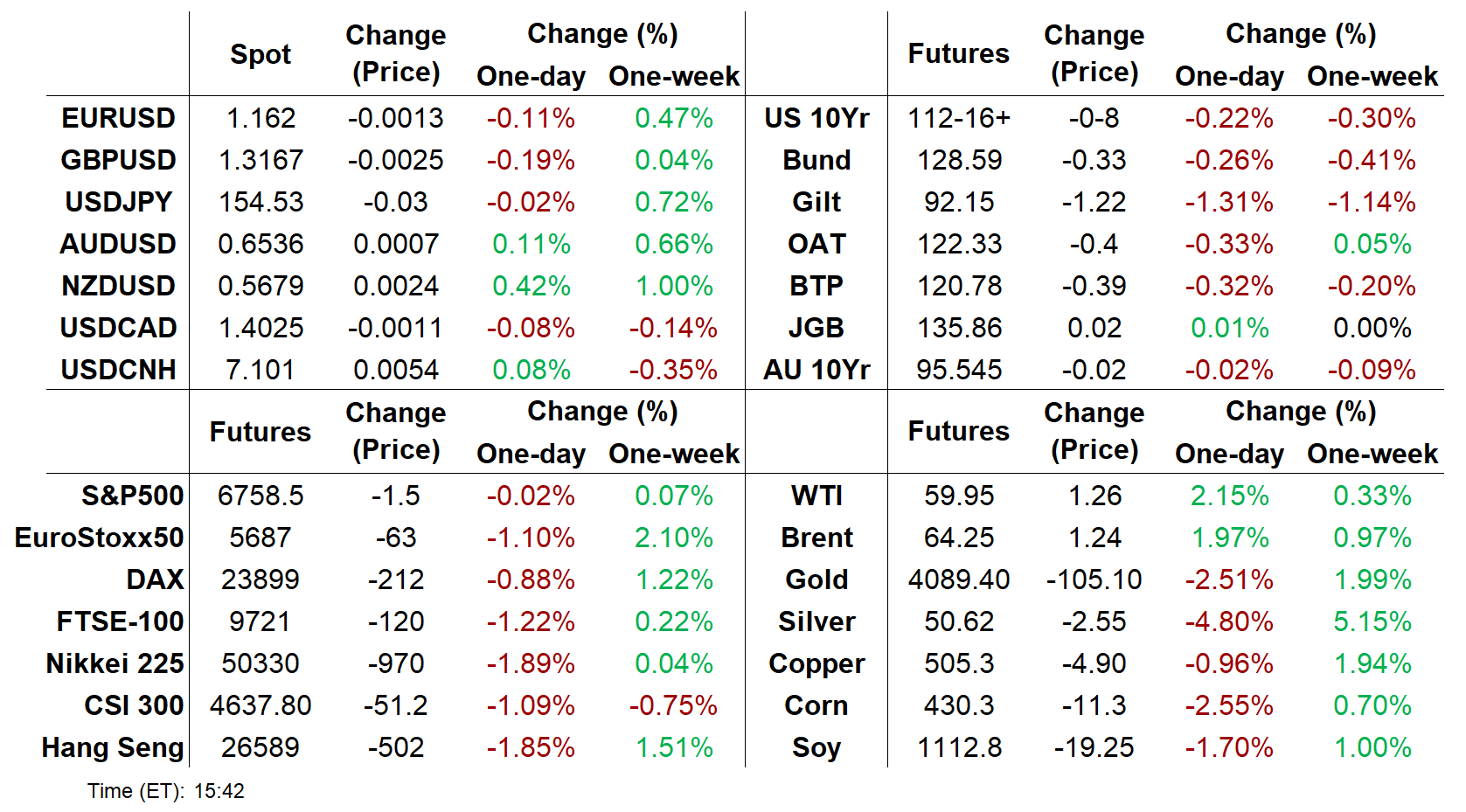

- Latest levels: The 2-Yr yield is up 2.1bps at 3.6121%, 5-Yr is up 2.6bps at 3.7327%, 10-Yr is up 2.7bps at 4.1463%, and 30-Yr is up 3.4bps at 4.7458%. Dec 10-Yr futures (TY) down 7.5/32 at 112-17 (L: 112-16 / H: 113-04.5)

- Along with the newly-rescheduled data mentioned above, next week's calendar includes the October FOMC minutes (we're watching for color on the debate over whether to ease any further) and flash November PMI data.

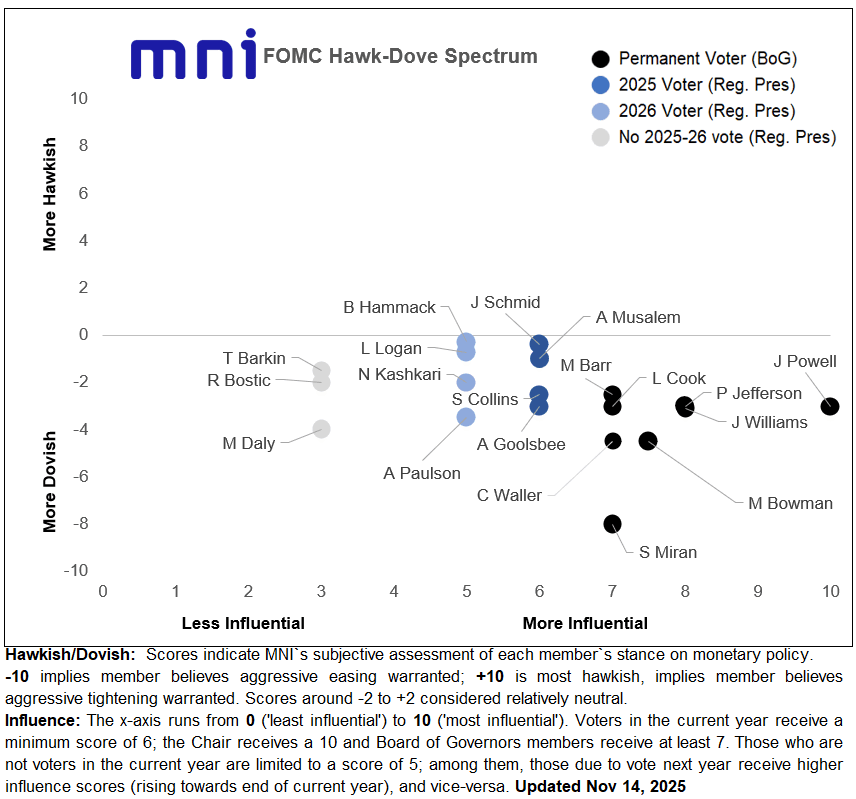

FED: Dallas's Logan Reiterates Cut Opposition; Regional Voters Getting Hawkish

Dallas Fed President Logan, a 2026 FOMC voter, reiterates that she doesn't currently see the need for a rate cut in December - recall she said after the October meeting that she opposed that cut.

- “I think it would be hard to support another rate cut unless we were to get convincing evidence that inflation is really coming down faster than my expectations or that we were seeing more than the gradual cooling that we’ve been seeing in the labor market". She says that “until I see convincing evidence that we are headed all the way back to our 2% target, I really do think modestly restrictive policy is appropriate." In general "it does not seem like a labor market to me that would for me... to see that it would be appropriate for further preemptive insurance."

- She was appearing at a joint Dallas-KC Fed event, the latter of whose president Schmid dissented in favor of a hold in October.

- Logan's comments are a reminder that the 2026 FOMC regional Fed presidential voters appear to be leaning increasingly hawkish: Logan, Cleveland's Hammack, and Minneapolis's Kashkari all say they did not support the October cut, though Philadelphia's Paulson appears to be more dovish-leaning.

- Generally speaking, the regional presidents have become quite hawkish versus the Fed Board - of the 12 presidents, it's only really SF's Daly and Philadelphia's Paulson that seem clearly amenable to further near-term rate cuts. Our latest Hawk-Dove update is below.

- We'll be watching in the FOMC Minutes (1400ET next Wednesday) for the degree of expressed opposition to October's rate cut and color on the debate over whether to ease any further. At the press conference, Chair Powell highlighted FOMC division over prospects for a December cut: “there's a growing chorus now of feeling like maybe this is where we should at least wait a cycle, something like that”, and noted that the meeting minutes would offer some more color on the internal debate. Since the meeting it's been clear that the hawks have become more vocal and arguably more entrenched, with more reluctance to ease any further given the federal data "fog".

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

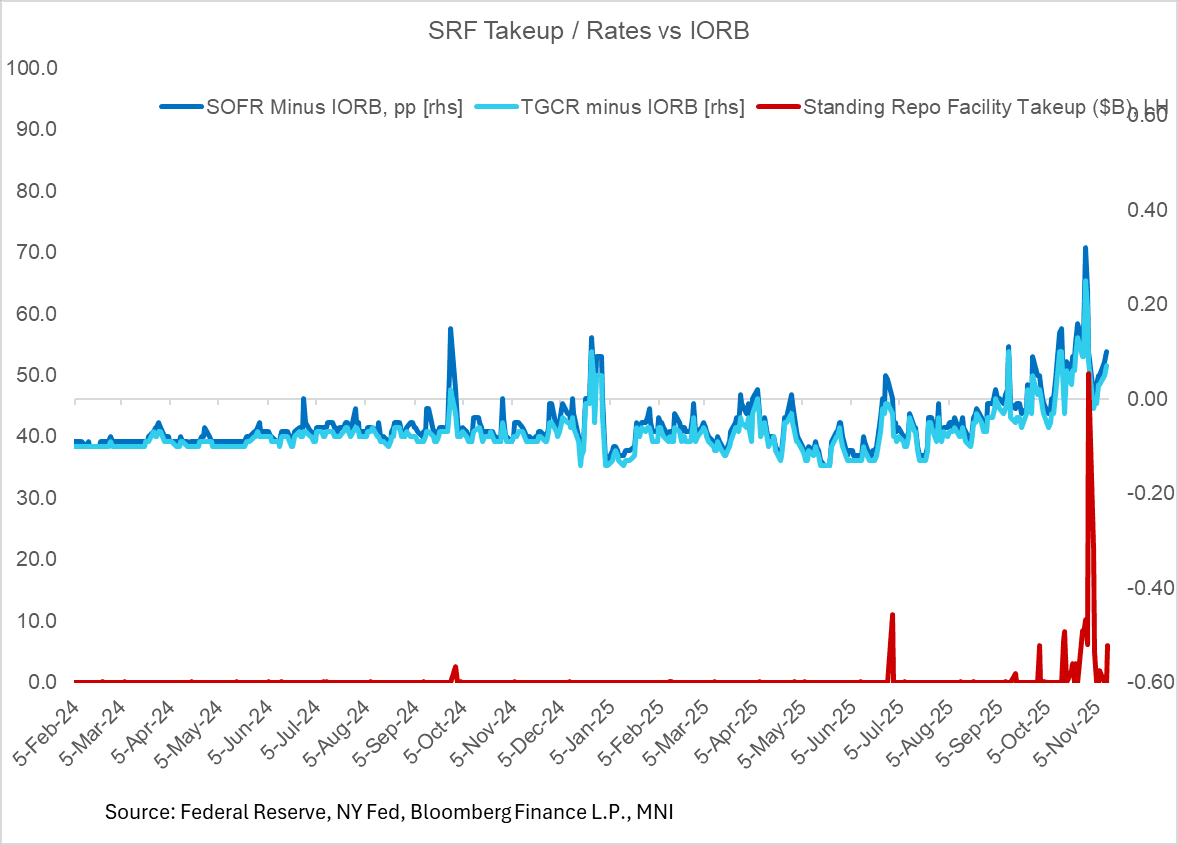

US TSYS/OVERNIGHT REPO: Rates Tick Up As KC Fed's Schmid Mentions IORB Tweak

Secured financing rates remained underpinned by Treasury bill settlements Thursday, with 2bp rises in SOFR to 4.00% and TGCR to 3.97%. That's 10bp and 7bp above IORB (3.90%), respectively, highest since Nov 3 and remaining elevated overall vs levels seen in recent years.

- As we noted yesterday there may be some slight relief Friday after a combined $37B in bill settlements on Weds/Thurs, though Monday could see rates underpinned once again due to $26.8B in coupon settlements.

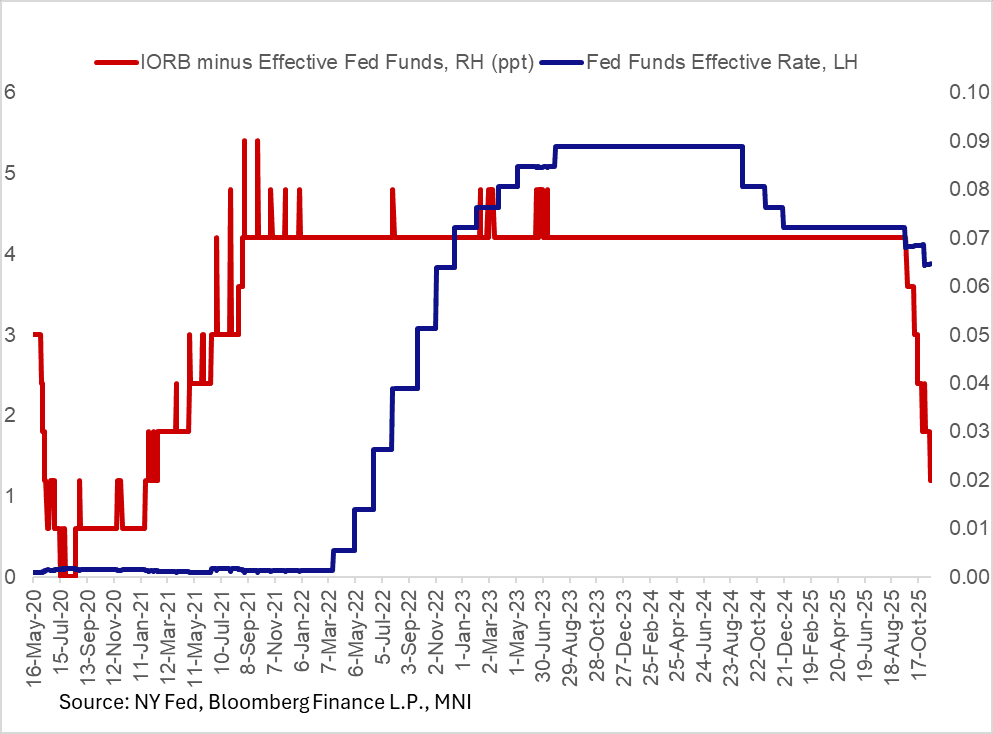

- Effective fed funds picked up 1bp to 3.88%, marking the highest point relative to the Fed's target range (2bp below IORB, vs 7bp seen for most of 2021-25) since early 2021.

- We took note of KC Fed Pres Schmid's speech released today that mentioned lowering IORB, a technical adjustment which would see repo rates fall and in theory allow the Fed to hold fewer reserves than it otherwise would: "Another possible action could be to lower the interest rate that the Fed pays on reserves within the target band. Currently this rate is 15 basis points above the bottom of the band. Lowering the rate within the band would allow more space for other interest rates to move before bumping up against the top of the band. This would allow for a greater range of private intermediation of reserve demand before the Fed would feel the need to take action."

- Recall that when SOFR and TGCR spreads widened versus IORB in 2018, the Fed lowered IORB relative to the Funds range.

REPO REFERENCE RATES (rate, change from prev. day, volume):

* Secured Overnight Financing Rate (SOFR): 4.00%, 0.02%, $3197B

* Broad General Collateral Rate (BGCR): 3.97%, 0.02%, $1260B

* Tri-Party General Collateral Rate (TGCR): 3.97%, 0.02%, $1227B

New York Fed EFFR for prior session (rate, chg from prev day):

* Daily Effective Fed Funds Rate: 3.88%, 0.01%, volume: $78B

* Daily Overnight Bank Funding Rate: 3.87%, no change, volume: $172B

OPTIONS: US Options Roundup - 14 Nov 2025

Friday's U.S. rates/bond options flow included:

- TY Week4 (expiry 28th Nov) 112.75/113.50cs vs 112.25p, bought the cs for flat in 30k

- TYZ5 113.00 calls ~5.6K given at 0-13.

- SFRZ5 96.37/96.43cs, traded 0.5 in 11k.

- SFRZ5 96.31/96.43cs, traded 1.75 in 4k.

- SFRZ5 96.31/96.37cs 1x2, traded flat in 7.5k.

- SFRZ5 96.31/96.37cs, traded 1.5 in 2k.

- SFRZ5 96.25^, traded 15.25 in 2k.

- SFRZ5 96.25/96.31/96.43c fly, traded 0.75 in 5k.

- SFRF6/H6 96.31/96.50^^ spread, bought for 6.25 in 2k. This was also bought into the close Yesterday for 6 in 5k.

- SFRH6 96.18/96.06ps 1x2, bought for 2.25 in 5k. This was also bought into the close Yesterday for 2 in 20k

- SFRU6 99.00/100.00/101.00c fly, traded 1.25 in 2k.

- SFRU6 96.87/97.12cs vs 0QU6 97.12/97.37cs, bought the front for 0.75 in 2.5k.

- 0QZ5 97.00/97.06/97.18c fly 2x3x1, traded 1.5 in 5k.

- 0QZ5 97.00/97.06/97.18/97.25c condor, traded for 1 in 4k.

- 0QF6 96.93/97.06cs, traded 4.5 in 10k.

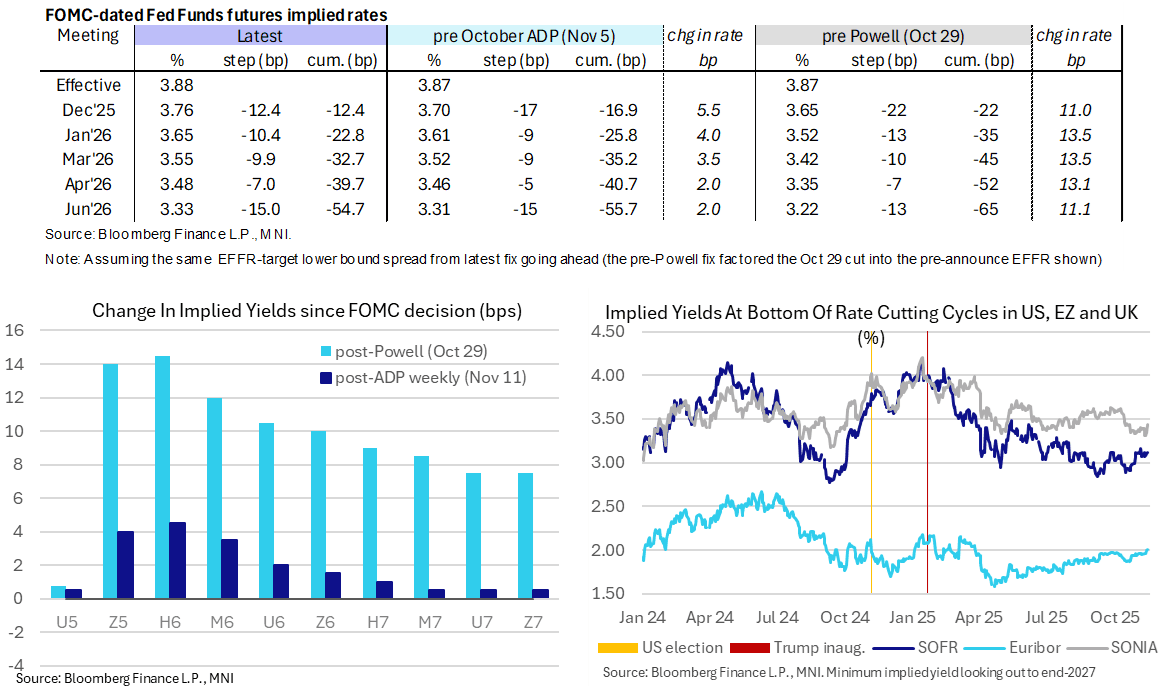

STIR: US Rates Back To Most Hawkish End Of The Week’s Range

- The aforementioned recovery in risk sentiment has seen US rates reverse their earlier rally, taking them back to levels as US desks filtered in.

- Fed Funds cumulative cuts from 3.88% effective (after a latest tick higher): 12.5bp Dec, 23bp Jan, 33bp Mar, 39.5bp Apr and 55bp Jun.

- SOFR futures are back to ranging between -0.015 (H6-M6) and -0.005 (Z6 onwards).

- The terminal implied yield of 3.11% (H7) is within the 3.065-3.16% range for closes over the past two weeks driven by labor releases.

- No data releases today have limited drivers to broader sentiment, and a hawkish Schmid (’25 voter, dissented favoring a hold last month) won’t have surprised - we think he will argue for another hold in December.

- Still to come today, Logan (’26, hawk) and Bostic (non-voter, surprisingly retiring in Feb). Logan said shortly after the the Oct FOMC decision that she would have preferred to hold rates steady and would find it difficult to cut rates again in December. Bostic recently called for holding rates until inflation is moving to 2% and sees price pressures persisting until mid-to-late 2026.

- There is still nothing concrete on revised data schedules, certainly of any note. The BLS said yesterday “it may take time” and the BEA and Census Bureau are still working on it, whilst indications remain that we’ll get the September nonfarm payrolls report next week but to be confirmed.

BONDS: EGBs-GILTS CASH CLOSE: Gilts Underperform On Renewed Fiscal Uncertainty

Gilts sold off sharply Friday on renewed UK fiscal concerns.

- Overnight reports that the Labour government would not raise income tax rates in the upcoming budget saw a sharp bear-steepening selloff in the UK curve, pushing yields to month-to-date highs across the curve in the biggest overall daily move since July.

- The selloff abated after reports/speculation that this apparent U-turn was facilitated by improved OBR forecasts rather than an outright politically-motivated capitulation, but the damage was done.

- EGB yields rose in sympathy, though not nearly to the same degree, with the German curve only bear steepening slightly.

- Periphery spreads widened alongside a risk-off move in equities but closed off their wides as stocks staged a late bounce; BTPs underperformed on the day.

- For the week, there was bear steepening in both the UK (2Y yield +4.8bp, 10Y +10.8bp) and German (2Y +4.6bp, 10Y +5.4bp) curves.

- After hours, Fitch's sovereign review of Greece is anticipated (an upgrade to BBB from BBB- would not be entirely surprising).

- Next week's scheduled highlights are flash November PMIs and UK October CPI.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.8bps at 2.036%, 5-Yr is up 1.9bps at 2.312%, 10-Yr is up 3.2bps at 2.72%, and 30-Yr is up 3.9bps at 3.319%.

- UK: The 2-Yr yield is up 8.2bps at 3.846%, 5-Yr is up 11bps at 4.011%, 10-Yr is up 13.7bps at 4.574%, and 30-Yr is up 16.4bps at 5.395%.

- Italian BTP spread up 2.2bps at 75.3bps / French OAT up 0.7bps at 73.8bps

EUROPE OPTIONS: UK Rate Selloff Sees Renewed Interest In Upside

Friday's Europe rates/bond options flow included:

- OATZ5 123.25/123.75cs vs 120.25/119.75ps, traded 5 for the cs in 2k.

- ERZ5 98.18c, bought for 0.25 in 11k

- ERM6 97.93/97.81ps 1x2, bought the 1 for flat in 7.25k

- SFIH6 96.25/96.35/96.65/96.75 call condor, bought for 6 & 6.25 in +10k

- SFIM6 96.70/96.85/96.90/97.05c condor, bought for 2.5 in 10k.

- SFIM6 96.80/96.90cs, bought for 2.25 in 5k

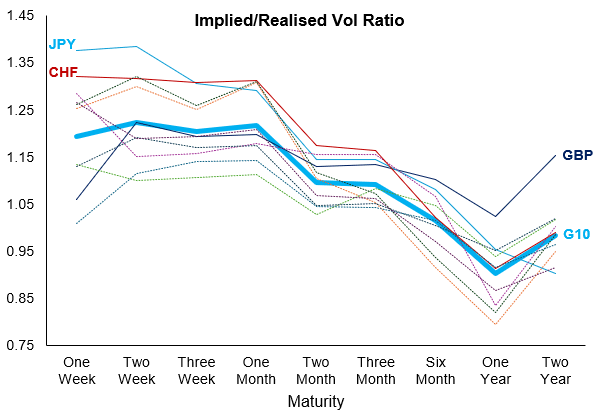

FOREX: Return of Intraday Vol Supports Haven FX, Boosts Volumes

- Intraday vol saw a significant pick-up across G10 FX Friday, as duelling reports on the state of UK government finances triggered a wide range for both spot GBP and Gilt yields, which briefly posted the sharpest intraday gain in months. Sentiment soon settled to moderate both the GBP sell-off and stress in UK bond markets, but speculation over fiscal policy is likely to endure in the coming weeks.

- A soft equity open on very little news helped trigger a bout of risk-off in both global stock markets and Treasury bonds - prompting spillover buying in JPY, CHF and USD - this soon faded into the London close, however.

- G10 FX implied vols skewed aggressively toward the front-end on very heavy volumes. We see GBP volumes nearly doubling their daily average, JPY 40% above and EUR 30% clear of a usual trading session. Resultantly, haven currencies now have the highest implied/realised volatility ratios across G10 - a signal that markets poised for further swings in risk sentiment headed into the new week - particularly as delayed data from the US begins to come back online.

- In contrast, the GBP implied/realised vol curve has moderated significantly in the front-end, indicating markets may see a smoother path into the November Budget now the OBR forecast is likely not as bad as feared. Nonetheless, the longer-end of the curve remains elevated - suggesting markets see GBP as structurally volatile across 2026 and beyond.

Source: MNI / Bloomberg Finance L.P.

- EURCHF pierced significant support during this morning's volatility, with the 0.9206-0.9211 zone having held prices well just last month, as well as twice last year. As a result, prices hit the lowest levels since the withdrawal of the 1.20 floor in 2015 but have since recovered back above 0.9200. Markets will be closely watching both the formation of the daily candle (as well as the weekly candle) for any evidence prices are trying to find a bottom.

- Markets await any firm schedules for data releases from US statistics agencies after the government reopen following yesterday's BLS announcement they are working to release information "as soon as possible".

OPTIONS: Larger FX Option Pipeline

- EUR/USD: Nov18 $1.1675(E1.3bln), $1.1700(E1.0bln); Nov19 $1.1700(E1.1bln), $1.1800(E1.6bln); Nov20 $1.1500(E2.0bln), $1.1630(E1.2bln), $1.1675-80(E1.5bln)

- USD/JPY: Nov18 Y153.00($1.3bln); Nov20 Y150.00($1.3bln), Y155.00($1.3bln)

- USD/CNY: Nov20 Cny7.1080-89($2.0bln)

US STOCKS CLOSE: Equities Recover From Intraday Pullback

Equities recovered from a sharp intraday sell-off to close roughly flat Friday, with the Nasdaq and S&P 500 almost unchanged but the the Dow Jones retracing 0.7% after Thursday's outperformance.

- Reeling from concerns over AI-related valuations and waning prospects for a December Fed cut, the S&P fell as much as 1.3% (6,646.87) which would have marked the lowest close in a month, but bounced to trade roughly flat on the session.

- Energy (+1.4%) and tech (0.7%) outperformed on the S&P 500, with losses led by financials (-1.0%) and materials (-1.2%).

- Megacaps NVidia (+1.6%) and Microsoft (+1.3%) were the biggest upside contributors, offsetting downside for Google (-0.7%), Netflix (-3.4%) and Amazon (-1.1%) in the tech/communications space, while JPM (-1.8%), Visa (-1.7%) and Mastercard (-1.8%) pulled down financials.

- Latest futures levels: Dow Jones mini down 325 pts or -0.68% at 47253, S&P 500 mini down 6.25 pts or -0.09% at 6762.5, NASDAQ mini down 13.75 pts or -0.05% at 25125.25.

DATA/EVENTS CALENDAR* (NOT UPDATED FOR LATEST U.S. BLS / CENSUS BUREAU RESCHEDULING)

| Date | GMT/Local | Impact | Country | Event |

| 15/11/2025 | 1330/1430 | ECB Schnabel Chairs Panel at Econ/FinStab Conference | ||

| 17/11/2025 | 2350/0850 | *** | GDP | |

| 17/11/2025 | 0430/1330 | ** | Industrial Production | |

| 17/11/2025 | 0800/0900 | Flash GDP | ||

| 17/11/2025 | 0815/0915 | ECB de Guindos Speech at Euro Finance Week | ||

| 17/11/2025 | 0900/1000 | ** | Italy Final HICP | |

| 17/11/2025 | 1000/0500 | * | CREA Existing Home Sales | |

| 17/11/2025 | 1315/0815 | ** | CMHC Housing Starts | |

| 17/11/2025 | 1320/1320 | BOE Mann on DMP and MonPol | ||

| 17/11/2025 | 1330/0830 | * | International Canadian Transaction in Securities | |

| 17/11/2025 | 1330/0830 | *** | CPI | |

| 17/11/2025 | 1330/0830 | ** | Empire State Manufacturing Survey | |

| 17/11/2025 | 1400/0900 | New York Fed's John Williams | ||

| 17/11/2025 | 1430/0930 | Fed Vice Chair Philip Jefferson | ||

| 17/11/2025 | 1445/1545 | ECB Lane Lecture on ECB MonPol | ||

| 17/11/2025 | 1600/1700 | ECB Cipollone at ECON Digital Euro Hearing | ||

| 17/11/2025 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 17/11/2025 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 17/11/2025 | 1800/1300 | Minneapolis Fed's Neel Kashkari | ||

| 17/11/2025 | 2035/1535 | Fed Governor Christopher Waller | ||

| 18/11/2025 | 1000/1100 | ECB Elderson at Banking Supervision Press Conference | ||

| 18/11/2025 | 1300/1300 | BOE Pill Fireside Chat on MonPol | ||

| 18/11/2025 | 1330/0830 | ** | Import/Export Price Index | |

| 18/11/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 18/11/2025 | 1415/0915 | *** | Industrial Production | |

| 18/11/2025 | 1500/1000 | ** | NAHB Home Builder Index | |

| 18/11/2025 | 1500/1500 | BOE Dhingra on Income Growth and Consumption | ||

| 18/11/2025 | 1530/1030 | Fed Governor Michael Barr | ||

| 18/11/2025 | 1600/1100 | Richmond Fed's Tom Barkin | ||

| 18/11/2025 | 2100/1600 | ** | TICS | |

| 18/11/2025 | 2300/1800 | Dallas Fed's Lorie Logan | ||

| 19/11/2025 | 2350/0850 | * | Machinery orders | |

| 19/11/2025 | 0001/0001 | * | Brightmine pay deals for whole economy | |

| 19/11/2025 | 0030/1130 | *** | Quarterly wage price index | |

| 19/11/2025 | 0700/0700 | *** | Consumer Inflation Report (1dp) | |

| 19/11/2025 | 0700/0700 | *** | Producer Prices | |

| 19/11/2025 | 0700/0700 | *** | Consumer Inflation Report (2dp) | |

| 19/11/2025 | 0900/1000 | ** | EZ Current Account | |

| 19/11/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 19/11/2025 | 1000/1100 | *** | EZ HICP Final | |

| 19/11/2025 | 1000/1100 | *** | EZ HICP Final | |

| 19/11/2025 | 1000/1100 | *** | EZ HICP Final | |

| 19/11/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 19/11/2025 | 1330/0830 | *** | Housing Starts | |

| 19/11/2025 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 19/11/2025 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 19/11/2025 | 1730/1230 | BOC Deputy Vincent speaks in Quebec City (Time TBC) | ||

| 19/11/2025 | 1745/1245 | Richmond Fed's Tom Barkin | ||

| 19/11/2025 | 1800/1300 | ** | US Treasury Auction Result for 20 Year Bond | |

| 19/11/2025 | 1900/1400 | FOMC Minutes | ||

| 19/11/2025 | 1900/1400 | New York Fed's John Williams | ||

| 20/11/2025 | 0700/0800 | ** | PPI | |

| 20/11/2025 | 1000/1100 | ** | EZ Construction Output | |

| 20/11/2025 | 1100/1100 | ** | CBI Industrial Trends | |

| 20/11/2025 | 1330/0830 | *** | Jobless Claims | |

| 20/11/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 20/11/2025 | 1330/0830 | * | Industrial Product and Raw Material Price Index | |

| 20/11/2025 | 1330/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 20/11/2025 | 1345/0845 | Cleveland Fed's Beth Hammack | ||

| 20/11/2025 | 1500/1000 | *** | NAR existing home sales | |

| 20/11/2025 | 1500/1000 | * | Services Revenues | |

| 20/11/2025 | 1500/1600 | ** | Consumer Confidence Indicator (p) | |

| 20/11/2025 | 1530/1030 | ** | Natural Gas Stocks | |

| 20/11/2025 | 1600/1100 | ** | Kansas City Fed Manufacturing Index | |

| 20/11/2025 | 1600/1100 | Fed Governor Lisa Cook | ||

| 20/11/2025 | 1740/1240 | Chicago Fed's Austan Goolsbee | ||

| 20/11/2025 | 1800/1300 | ** | US Treasury Auction Result for TIPS 10 Year Note | |

| 20/11/2025 | 1830/1830 | BOE Dhingra Speech on Trade and Tariffs | ||

| 21/11/2025 | 2200/0900 | *** | Judo Bank Flash Australia PMI | |

| 21/11/2025 | 2330/0830 | *** | CPI | |

| 20/11/2025 | 2345/1845 | Philly Fed's Anna Paulson | ||

| 21/11/2025 | 0001/0001 | ** | Gfk Monthly Consumer Confidence | |

| 21/11/2025 | 0030/0930 | ** | Jibun Bank Flash Japan PMI | |

| 21/11/2025 | 0700/0700 | *** | Public Sector Finances | |

| 21/11/2025 | 0700/0700 | *** | Retail Sales | |

| 21/11/2025 | 0745/0845 | ** | Manufacturing Sentiment | |

| 21/11/2025 | 0800/0900 | ECB de Guindos Remarks/Q&A at Foro Gran Via | ||

| 21/11/2025 | 0815/0915 | ** | S&P Global Services PMI (p) | |

| 21/11/2025 | 0815/0915 | ** | S&P Global Manufacturing PMI (p) | |

| 21/11/2025 | 0830/0930 | ** | S&P Global Services PMI (p) | |

| 21/11/2025 | 0830/0930 | ** | S&P Global Manufacturing PMI (p) | |

| 21/11/2025 | 0830/0930 | ECB Lagarde Speech at European Banking Congress | ||

| 21/11/2025 | 0900/1000 | ** | S&P Global Services PMI (p) | |

| 21/11/2025 | 0900/1000 | ** | S&P Global Manufacturing PMI (p) | |

| 21/11/2025 | 0900/1000 | ** | S&P Global Composite PMI (p) | |

| 21/11/2025 | 0930/0930 | *** | S&P Global Manufacturing PMI flash | |

| 21/11/2025 | 0930/0930 | *** | S&P Global Services PMI flash | |

| 21/11/2025 | 0930/0930 | *** | S&P Global Composite PMI flash | |

| 21/11/2025 | 1000/1100 | Negotiated Wage Growth | ||

| 21/11/2025 | 1130/1230 | ECB de Guindos Remarks/Q&A at Deusto Business School | ||

| 21/11/2025 | 1230/0730 | New York Fed's John Williams | ||

| 21/11/2025 | 1330/0830 | ** | Retail Trade | |

| 21/11/2025 | 1330/0830 | Fed Governor Michael Barr | ||

| 21/11/2025 | 1345/0845 | Fed Vice Chair Philip Jefferson | ||

| 21/11/2025 | 1400/0900 | Dallas Fed's Lorie Logan | ||

| 21/11/2025 | 1445/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 21/11/2025 | 1445/0945 | *** | S&P Global Services Index (flash) | |

| 21/11/2025 | 1500/1000 | *** | U. Mich. Survey of Consumers | |

| 21/11/2025 | 1500/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 21/11/2025 | 1540/1540 | BOE Pill in Panel at Swiss National Bank | ||

| 21/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 21/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly |