FOREX: Return of Intraday Vol Supports Haven FX, Boosts Volumes

- Intraday vol saw a significant pick-up across G10 FX Friday, as duelling reports on the state of UK government finances triggered a wide range for both spot GBP and Gilt yields, which briefly posted the sharpest intraday gain in months. Sentiment soon settled to moderate both the GBP sell-off and stress in UK bond markets, but speculation over fiscal policy is likely to endure in the coming weeks.

- A soft equity open on very little news helped trigger a bout of risk-off in both global stock markets and Treasury bonds - prompting spillover buying in JPY, CHF and USD - this soon faded into the London close, however.

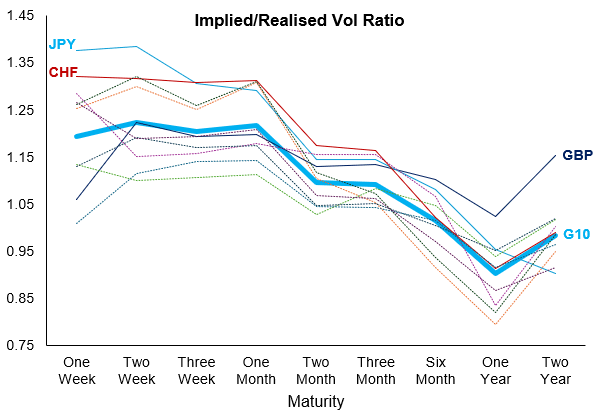

- G10 FX implied vols skewed aggressively toward the front-end on very heavy volumes. We see GBP volumes nearly doubling their daily average, JPY 40% above and EUR 30% clear of a usual trading session. Resultantly, haven currencies now have the highest implied/realised volatility ratios across G10 - a signal that markets poised for further swings in risk sentiment headed into the new week - particularly as delayed data from the US begins to come back online.

- In contrast, the GBP implied/realised vol curve has moderated significantly in the front-end, indicating markets may see a smoother path into the November Budget now the OBR forecast is likely not as bad as feared. Nonetheless, the longer-end of the curve remains elevated - suggesting markets see GBP as structurally volatile across 2026 and beyond.

Source: MNI / Bloomberg Finance L.P.

- EURCHF pierced significant support during this morning's volatility, with the 0.9206-0.9211 zone having held prices well just last month, as well as twice last year. As a result, prices hit the lowest levels since the withdrawal of the 1.20 floor in 2015 but have since recovered back above 0.9200. Markets will be closely watching both the formation of the daily candle (as well as the weekly candle) for any evidence prices are trying to find a bottom.

- Markets await any firm schedules for data releases from US statistics agencies after the government reopen following yesterday's BLS announcement they are working to release information "as soon as possible".

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OPTIONS: Large Trading In And Out Of Euribor Call, Mixed Trade In Sonia

Wednesday's Europe rates/bond options flow included:

- ERZ5 98.25c, sold at 0.5 in 10k. Earlier: ERZ5 98.25c, bought for half in 33k

- SFIZ5 96.30/96.40/96.50c fly, bought for 1 in 4k

- SFIZ5 96.20/96.30cs 1x2, bought for 0.25 in 2.5k.

- SFIH6 96.25/96.05/95.85p fly, bought for 4.75 in 5.5k

US OUTLOOK/OPINION: ADP Weaker Than Non-Paywalled Revelio Labs And Carlyle

Two indicators that have recently been un-paywalled in response to the government shutdown offer alternative tracking estimates for jobs growth. The Revelio estimate implies no further softening than recent trends in the latest BLS payrolls data published to August (3mth average 29k, 6mth 64k or private sector averages of 29k and 67k) whilst others are weaker.

- Revelio Labs estimate jobs growth of 60k in September with growth driven by education and health services, an area that has been a major driver of nonfarm payrolls growth in the BLS report for some time now. See their range of labor-related releases here.

- Carlyle Group comes up with a more pessimistic estimate, eyeing a 17k increase in September. This is based on operational data from its portfolio companies which employ more than 700k people globally (see more, here). From the linked interview with Bloomberg: “What’s so interesting about the moment we’re in is the discrepancy between payrolls and the other economic indicators we’re looking at,” said Jason Thomas, Carlyle’s head of global research and investment management. “If you looked at the employment data, you’d think it’s an economy that’s on the cusp of or in a recession. That is nowhere else in the data.”

- Whilst both soft, and likely close to or below payrolls breakeven estimates, both are tracking stronger than the widely known and publicly available ADP release. The latter saw its biggest private payrolls drop (-32k) since March 2023 and before that, Jun 2020. And the prior 54k was revised down to -3k, so the first back-to-back drops since the pandemic. We touch more on this below.

SECURITY: US Edges Closer To Imposing New Penalties On Russia

US Treasury Secretary Scott Bessent told reporters, “anyone purchasing Russian energy is subsidizing attacks on the Ukrainian people,” per Reuters. Bessent’s comment comes as the US appears to be edging towards imposing new penalties on Russia, and the Trump administration weighs up selling Ukraine long-range Tomahawk missiles.

- Earlier today, US Defense Secretary Pete Hegseth said at the NATO defence ministerial meeting in Brussels, “If this war does not end, if there is no path to peace in the short term, then the United States, along with our allies, will take the steps necessary to impose costs on Russia for its continued aggression.”

- US Ambassador to NATO Matthew Whitaker told La Repubblica yesterday, “Tomorrow, the US will make an important announcement regarding arms supplies to Ukraine… There are almost—I don’t want to say unlimited possibilities—but certainly there are many consequences for not reaching a peace agreement that could be used against the Russians.”

- Politico reports that Senate Majority Leader John Thune (R-SD) “left the door open Tuesday to voting on a long-stalled Russia sanctions bill as soon as this month. He didn’t commit to putting it on the floor — noting he still has to coordinate strategy with the White House — but said he believes the issue is ‘pretty ripe.’”

- US Senators are also working to set up a bipartisan meeting with Ukrainian President Volodymyr Zelenskyy alongside his White House meeting with Trump on Friday.