FED: Dallas's Logan Reiterates Cut Opposition; Regional Voters Getting Hawkish

Dallas Fed President Logan, a 2026 FOMC voter, reiterates that she doesn't currently see the need for a rate cut in December - recall she said after the October meeting that she opposed that cut.

- “I think it would be hard to support another rate cut unless we were to get convincing evidence that inflation is really coming down faster than my expectations or that we were seeing more than the gradual cooling that we’ve been seeing in the labor market". She says that “until I see convincing evidence that we are headed all the way back to our 2% target, I really do think modestly restrictive policy is appropriate." In general "it does not seem like a labor market to me that would for me... to see that it would be appropriate for further preemptive insurance."

- She was appearing at a joint Dallas-KC Fed event, the latter of whose president Schmid dissented in favor of a hold in October.

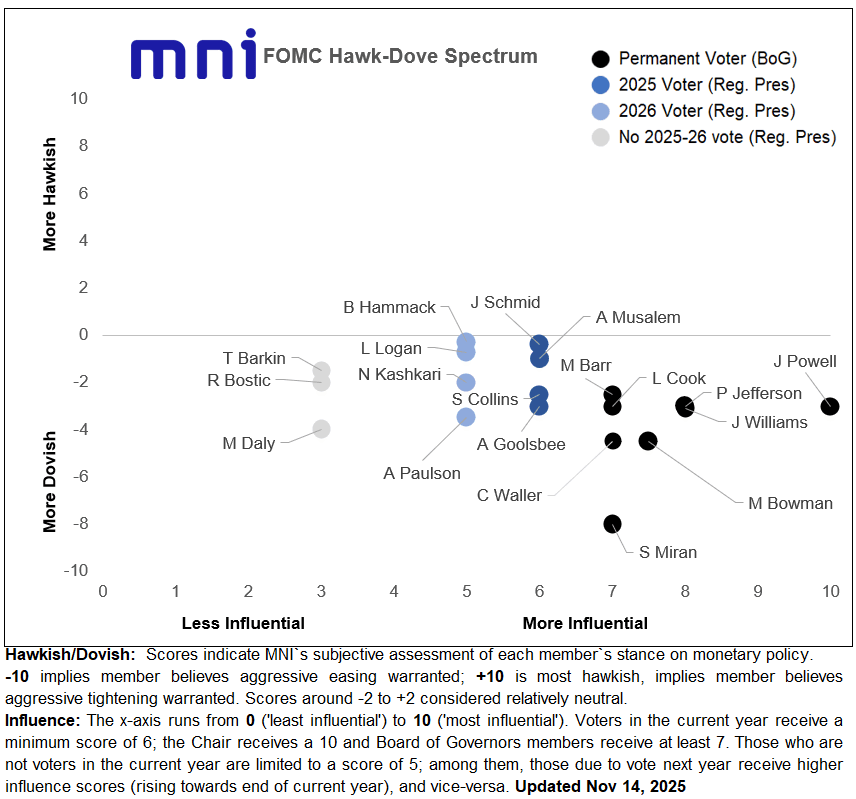

- Logan's comments are a reminder that the 2026 FOMC regional Fed presidential voters appear to be leaning increasingly hawkish: Logan, Cleveland's Hammack, and Minneapolis's Kashkari all say they did not support the October cut, though Philadelphia's Paulson appears to be more dovish-leaning.

- Generally speaking, the regional presidents have become quite hawkish versus the Fed Board - of the 12 presidents, it's only really SF's Daly and Philadelphia's Paulson that seem clearly amenable to further near-term rate cuts. Our latest Hawk-Dove update is below.

- We'll be watching in the FOMC Minutes (1400ET next Wednesday) for the degree of expressed opposition to October's rate cut and color on the debate over whether to ease any further. At the press conference, Chair Powell highlighted FOMC division over prospects for a December cut: “there's a growing chorus now of feeling like maybe this is where we should at least wait a cycle, something like that”, and noted that the meeting minutes would offer some more color on the internal debate. Since the meeting it's been clear that the hawks have become more vocal and arguably more entrenched, with more reluctance to ease any further given the federal data "fog".

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: QT Conclusion Seen A Little Earlier After Powell Comments

Chair Powell's speech Tuesday, titled "Understanding the Fed's Balance Sheet", included a passage that saw some expectations brought forward for the timing of the end of Fed balance sheet runoff: "Our long-stated plan is to stop balance sheet runoff when reserves are somewhat above the level we judge consistent with ample reserve conditions. We may approach that point in coming months, and we are closely monitoring a wide range of indicators to inform this decision."

- Analyst expectations for QT to end are roughly focused on end-year timing, with at least one analyst eyeing an end as soon as November with some still seeing early 2026 (February/ Q1). Note that the NY Fed's latest Survey of Market expectations showed the median respondent expects Fed balance sheet runoff to end in January.

- TD: "Given the Chair's focus, we believe the end of QT is likely to be announced at the October FOMC meeting (compared with our prior call for early-2026). This will

ensure that the Fed will no longer allow Treasury runoff starting in November...while we expect the SOMA portfolio to remain steady, substantial year-end pressure

could lead the Fed to consider resuming open market purchases of securities as early as 2026." - BofA: "Powell comments affirm our Fed B/S base case: (1) QT stop at end '25 & move MBS repays into UST, likely bills, at pace of $10-20b/m (2) Fed B/S growth in Mar '26 to offset liability growth (i.e currency & reserves), likely into bills, at pace of $15b/m. Both should see Fed buys in secondary market due to cash flow timing issues. This could provide ~$30b/m of bill support. Fed bill buying helpful for UST WAM shift. Risks are Fed could: (a) end QT or offset liability growth later (b) buy mix of bills & coupons. Fed B/S liability driven growth not QE b/c minimal duration risk removal / financial condition easing."

- Goldman: "We are pulling forward our forecast for the end of balance sheet runoff. We now expect the FOMC to announce at its January meeting that runoff will end in February. We see these comments as broadly consistent with our expectation that runoff will end at the end of Q1, though we think they raise the risk that runoff stops a bit earlier."

- Deutsche: "Our interpretation is December" (re Powell's mention of balance sheet runoff potentially ending in the “coming months”).

- JPMorgan: "In footnotes to [Powell's] remarks, it was observed that reserves are currently about 10% of GDP and were 8% of GDP when funding pressures emerged in 2019. We continue to think that balance sheet runoff ends in 1Q26."

USDCAD TECHS: Bullish Theme

- RES 4: 1.4200 Round number resistance

- RES 3: 1.4167 50.0% retracement of the Feb 3 - Jun 16 bear leg

- RES 2: 1.4111 High Apr 10

- RES 1: 1.4080 Intraday high

- PRICE: 1.4038 @ 16:00 BST Oct 15

- SUP 1: 1.3939/3870 20- and 50-day EMA values

- SUP 2: 1.3802 Bull channel base drawn from the Jul 23 low

- SUP 3: 1.3727 Low Aug 29 and a bear trigger

- SUP 4: 1.3689 Low Jul 28

A bull cycle in USDCAD remains intact and this week’s gains reinforce current conditions. Last Thursday’s rally confirmed a recent bull flag on the daily chart and a resumption of the current uptrend. MA studies are in a bull-mode position, highlighting a dominant uptrend. Sights are on 1.4111, the Apr 10 high, and further out scope is seen for an extension towards 1.4167, a Fibonacci retracement. First key support is 1.3870, 50-day EMA.

US TSYS: Tsys Whipsaw Lower, Risk Sentiment Tested on Policy & Trade

- Treasuries ratcheted lower Wednesday, buffeted by several rounds of selling and a reversal in overall sentiment that triggered selling in equities.

- Treasuries retreated through early overnight levels, coinciding with EU headlines that the EU is discussing "preferential treatment to give domestic firms bidding for public contracts worth about €2.5 trillion ($2.9 trillion) a year," Bbg. Note, however, 10Y Bund also declined and is rebounding.

- Treasuries moderated near session lows following comments by Fed Gov Miran (voter) at a Nomura Research Forum stated that US-China trade tensions tied to rare-earth curbs "pose significant downside risks". Ironically, this comes after after Treasury Sec Bessent suggested the possibility of a "longer tariff truce with China tied to rare-earth imports" helped risk sentiment earlier.

- Currently, Tsy Dec'25 10Y contract trades 113-09 (-4) vs. 113-06.5 low, yld tapped 4.0455% high; curves flatter/off lows: 2s10s -1.490 at 53.445 (51.608 low), 5s30s -1.561 at 100.734 (98.827 low). Initial technical support at 112-26 (20-day EMA) followed by the 50-day EMA at 112-16. A clear break of the average would expose 111-13+, the Aug 18 low and a key support.

- Cross asset: Bbg US$ index off lows, -3.35 at 1211.09 (1210.10 low), stocks off early highs: DJIA down down 72.67 points (-0.16%) at 46,200.11, S&P E-Minis up 12.5 points (0.19%) at 6,699.25, Nasdaq up 91.7 points (0.4%) at 22,611.45.

- Look ahead: Thursday's Retail Sales, PPI and Business Inventories suspended due to the Gov shutdown. On the other hand, Weekly Jobless Claims on a state level likely to be gradually parsed out.