MNI ASIA MARKETS ANALYSIS: DJIA Climbs to New Record High

HIGHLIGHTS

- Treasuries added to the post FOMC rally Thursday after Initial jobless claims ‘surprised’ higher at 236k (sa, cons 220k) in the week to Dec 6; Tsys consolidated much of the move by the close.

- September's goods and services trade deficit came in on the smaller side of expectations, at $52.8B ($63.1B consensus) - the smallest shortfall since June 2020.

- Post-Fed dollar weakness had been offset by Oracle-related equity weakness initially on Thursday, however, as the major equity benchmarks steadily recovered throughout the session, the USD index extended to fresh pullback lows.

- Stocks remain broadly mixed Thursday, the DJIA continuing to extend record highs (48,756.34) while the tech heavy Nasdaq remains weaker in late trade (SPX eminis make modest gains).

US TSYS

US TSYS: Jobless Claims Rise Most Since July 2021, Fed Speakers Return Friday

- Still bid after the bell, Treasuries are well off first half highs - adding to the post-FOMC rally in rates. Currently, TYH6 trades +7.5 at 112-14.5 vs. 112-23 high.

- The bearish theme in Treasuries remains intact and the latest bounce appears corrective. An important short-term support at 112-07, the Nov 5 low and a bear trigger, has been cleared. The breach strengthens a bear theme and signals scope for a move towards 111-19 next a Fibonacci projection. Curves steeper: 2s10s +.658 at 61.320, 5s30s +2.315 at 107.738.

- Treasuries tapped extended gains after higher than expected weekly jobless claims while continuing claims sharply lower than expected. Trade balance declines, as do imports & exports.

- Initial jobless claims ‘surprised’ higher at 236k (sa, cons 220k) in the week to Dec 6, a consensus reading that had looked for surprisingly little rebound considering it followed the 3+ year low of 219k in the week to Nov 29 in what had looked likely down to difficulty in adjusting around the Thanksgiving holiday. Continuing claims meanwhile were also lower than expected at 1838k (sa, cons 1938k) in the week to Nov 29 after a marginally downward revised 1937k (initial 1939k).

- September's goods and services trade deficit came in on the smaller side of expectations, at $52.8B ($63.1B consensus) - the smallest shortfall since June 2020. It's a far cry from the $100+B deficits in the 1st quarter, and came on the back of the smallest goods deficit since September 2020 ($79.0B).

- Look ahead to Friday: Muted data with Business formation statistics from Census Bureau/Commerce Dept at 1000ETR. Otherwise, Fed speakers return:

- 0800 Philly Fed Paulson economic outlook (text, Q&A) at 0800ET

- 0830 Cleveland Fed Hammack real estate roundtable (no text, Q&A), 0830ET

- 1035 Chicago Fed Goolsbee economic outlook symposium (no text, Q&A) 1035ET

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.90% (-0.03), volume: $3.222T

- Broad General Collateral Rate (BGCR): 3.87% (-0.03), volume: $1.326T

- Tri-Party General Collateral Rate (TCR): 3.87% (-0.03), volume: $1.297T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.89% (+0.00), volume: $98B

- Daily Overnight Bank Funding Rate: 3.89% (+0.00), volume: $184B

FED Reverse Repo Operation

RRP usage retreats to $2.874B with 7 counterparties this afternoon from $5.045B Wednesday. Compares to Tuesday November 18: $0.905B - lowest level since mid-March 2021; this years highest excess liquidity measure: $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury option flow remained mixed late Thursday, two-way put structures amid some chunky buying in the second half. Underlying futures firmer but off morning highs. Projected rate cut pricing has gained slightly vs. early morning levels (*): Jan'26 at -6.1bp (-5bp), Mar'26 at -13.2bp (-12.7bp), Apr'26 at -19.6bp (-19.1bp), Jun'26 at -33.31bp (-32bp).

SOFR Options:

+3,500 SFRH6 96.43/96.50/96.62/96.68 call condors, 1.5 vs. 96.485/0.05%

-1,650 SFRM6 96.68 straddles, 33.25 ref 96.67

-4,000 SFRF6 96.12/96.18/96.37/96.43 put condors, 2.75 ref 96.46

-6,000 SFRH6 96.25/96.37 put spds 0.75 over 96.50/96.62/96.75/96.87 call condors

+40,000 0QH6 96.50 puts, 4.5 ref 96.845 to -.85

Block, 2,500 SFRZ5 96.25/93.31 call spds 3.25 ref 96.285

-8,000 0QF6 96.25/96.50/96.75 put flys, 4.5 vs. 96.825/0.20%

4,000 2QF6 96.12/96.25/96.37/96.50 put condors ref 96.69

Blocks, +7,500 0QH6 96.25/96.50 put spds, 3 ref 96.84

1,500 SFRH6 96.50 straddles, 18.5

2,500 SFRG6 96.31/96.50/96.56 broken call trees

Block, +3,250 SFRF6 96.56 calls, 2.75 vs. 96.445/0.25%

3,000 SFRZ6 96.87 puts

-2,000 SFRZ6 96.62/96.87 put spds, 12.5

over 14,000 SFRZ6 96.75 puts, total volume over 28k includes broken put fly:

over +6,000 SFRZ6 96.12/96.75/97.12 broken put flys, 6.0 vs. 96.90/0.05

Treasury Options:

4,568 FVF6 108/108.25 2x1 put spds ref 109-10.5

5,288 FVG6 107.25/107.75 2x1 put spds ref 109-10.5

-20,000 FVF6 109.25/109.75 call spds, 13-12.5 ref 109-11.5

5,000 FVF6 109/109.25 call spds ref 109-07.75

+2,000 TYF6/TYG6 115 call spds, 6 net vs. 112-17.5/0.07%

-2,000 TYF6 110.5/112 put spds, 13 vs. 112-14.5/0.29%

-2,000 TYF6 110/111.5 put spds, 6 vs. 112-14/0.16%

2,000 TYH6 113 calls, 44 ref 112-14.5

-5,000 TUF6 103.87/104.12/104.5 2x3x1 put flys, 8.5

over 12,200 TYF6 112.75 calls, 19 last

+2,750 TYH6 113 calls, 45 vs. 112-14/0.37%

+2,750 TYH6 112.5 puts, 103 vs. 112-10/0.52%

+4,000 TYF6 113.5 calls, 6

5,000 wk2 TY 112.75/113 call spds ref 112-14

MNI BONDS: EGBs-GILTS CASH CLOSE: Yields Tick Lower On Fed Relief

EGB and Gilt yields pulled back Thursday, in the wake of the Federal Reserve decision.

- Treasuries led overnight global gains after the Fed's communications proved less hawkish than feared.

- The European short-end saw some relief in an overall steepening move across curves.

- Germany saw outright bull steepening with the short-end outperforming on the curve after recent underperformance; Gilts however outperformed Bunds in absolute terms, with outperformance in the UK belly.

- Gilts held on to early gains better than Bunds, which at one point retraced overnight gains despite little apparent macro/headline driver.

- 10Y Gilt spreads to Bunds set another fresh post-September 2024 low.

- Periphery / semi-core EGB spreads tightened, with gains led by Spain and Portugal.

- Friday's data includes UK monthly economic activity and final French/German/Spanish November inflation.

Closing Yields / 10-Yr EGB Spreads To Germany

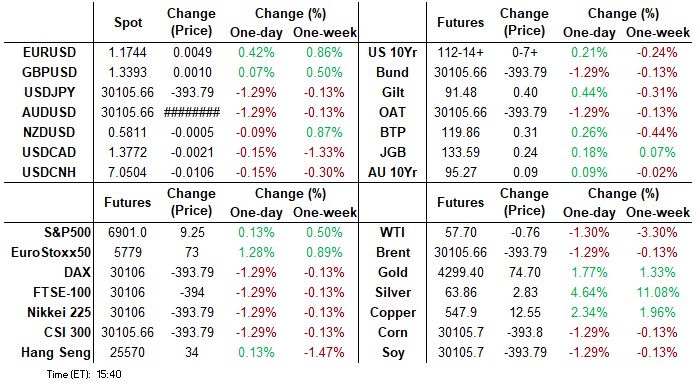

- Germany: The 2-Yr yield is down 1.7bps at 2.16%, 5-Yr is down 1.2bps at 2.464%, 10-Yr is down 0.8bps at 2.843%, and 30-Yr is down 0.1bps at 3.452%.

- UK: The 2-Yr yield is down 1.9bps at 3.771%, 5-Yr is down 2.4bps at 3.959%, 10-Yr is down 2.2bps at 4.484%, and 30-Yr is up 0.2bps at 5.207%.

- Italian BTP spread down 1.2bps at 68.4bps / Portuguese down 1.7bps at 31.1bps

MNI EGB OPTIONS: Less Upside Lean Than Usual Across Rates And Bonds Thursday

Thursday's Europe rates/bond options flow included:

- DUF6 106.8/106.9/107 call fly ~6.7K given at 0.75

- ERH6 97.9375/97.875/97.8125p fly, bought for 1.15 (synth) in 10k

- SFIU6 96.80/96.90cs, traded for 2.5 in ~10.25k

- SFIZ6 96.70/97.00cs, traded for 8.5 in 7.8k

MNI FOREX: Greenback Weakness Extends, CHF Continues to Outperform Post-SNB

- Post-Fed dollar weakness had been offset by Oracle-related equity weakness initially on Thursday, however, as the major equity benchmarks steadily recovered throughout the session, the USD index extended to fresh pullback lows. This dynamic was exacerbated by the higher-than-expected jobless claims data, boosting concerns over the US labour market. This has prompted the USD index to extend its three-week selloff to around 2.25%.

- The broad greenback weakness translated to roughly 0.5% rallies for the likes of EUR and JPY, while AUD was a notable underperformer following the weaker-than-expected jobs report during APAC hours.

- For EURUSD, spot grinded steadily higher above the 1.17 handle to narrow the gap significantly to 1.1779, the Oct 01 high. Despite the initial Aussie pressure, AUDUSD has done a good job in rallying back to within striking range of the week’s highs at 0.6686, highlighting the resilient technical profile. 0.6717 remains a key resistance.

- Elsewhere, the Swiss Franc continues to outperform, rising a further 0.7% against the dollar today amid the SNB’s decision to hold rates. Despite downwardly revised inflation forecasts, the SNB’s conviction for a medium-term CPI uptick remains firm. USDCHF weakness picked up momentum through two lows at 0.7992, signalling scope for a move towards 0.7873 and year’s lows at 0.7829.

- In emerging markets, USDMXN continues to erode last year’s post-election rally, sinking to the lowest levels seen since July 2024. The pair now resides just above the psychological 18.00 handle, and technical signals point to a growing likelihood of a move towards 17.4491, as we approach next week’s Banxico meeting.

MNI FX OPTIONS: Expiries for Dec12 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1550(E1.5bln), $1.1600(E629mln), $1.1700(E840mln)

- USD/JPY: Y154.00($614mln), Y155.00($1.3bln), Y156.00-15($1.2bln)

- GBP/USD: $1.3240-55(Gbp1.1bln), $1.3330(Gbp782mln), $1.3415(Gbp593mln)

- AUD/USD: $0.6650(A$897mln)

- USD/CAD: C$1.3780-00($1.6bln)

MNI US STOCKS: Late Equities Roundup: DJIA Near New Record Highs, IT Underperforming

- Stocks remain broadly mixed Thursday, the DJIA continuing to extend record highs (48,722.98) while the tech heavy Nasdaq remains weaker in late trade (SPX eminis make modest gains).

- Currently, the DJIA trades up 640.38 points (1.33%) at 48698.78, S&P E-Mini Futures up 13.25 points (0.19%) at 6904.5, Nasdaq down 56.6 points (-0.2%) at 23596.41.

- Materials, Financials and Health Care sector shares continued to lead advances in late trade:

- Mosaic Co +6.19%, Newmont Corp +5.79%, CF Industries Holdings +3.69%, Freeport-McMoRan +3.38%, Ball Corp +2.91% and Smurfit WestRock +2.65%.

- Visa Inc +5.62%, Hartford Insurance Group +4.16%, Mastercard +4.15%, Chubb +3.59% and Progressive Corp +3.46%.

- Elevance Health +5.57%, Centene +5.22%, Molina Healthcare +5.16%, Cigna Group +3.53%, Humana +3.39% and Baxter International Inc +2.90%.

- Conversely, Information Technology and Communication Services sector shares led the declines in the second half - questions over AI and chip maker valuations weighed heavily on the tech sector again.

- Off earlier lows, Oracle is still down over 11% in late trade after reporting lower than expected revenues on soft cloud infrastructure sales. Other weaker tech stocks included: Super Micro Computer -4.21%, Intel Corp-3.29%, Hewlett Packard Enterprise -3.01%, Applied Materials -2.37%, Micron Technology -2.35% and Qnity Electronics -2.16%.

- Communication Services sector shares also remained in the spotlight: Trade Desk Inc -5.00%, Paramount Skydance -2.92%, Alphabet -2.23% and Charter Communications -1.28%.

MNI EQUITY TECHS: E-MINI S&P: (Z5) Corrective Pullback

- RES 4: 7000.00 Psychological round number

- RES 3: 6953.75 High Oct 30 and bull trigger

- RES 2: 6918.50 High Oct 31

- RES 1: 6908.00 High Dec 10

- PRICE: 6905.00 @ 1445 ET Dec 11

- SUP 1: 6815.09 20-day EMA

- SUP 2: 6762.27 50-day EMA

- SUP 3: 6674.50 Low Nov 25

- SUP 4: 6525.00 Low Nov 21 and a key support

A bull cycle in S&P E-Minis remains intact and today’s pullback appears corrective - for now. Note that recent gains signal the likely end of the corrective cycle between Oct 30 and Nov 21. A resumption of gains would highlight potential for a move towards the key resistance and bull trigger at 6953.75, the Oct 30 high. Key support lies at 6525.00, the Nov 21 low. First support to watch is at 6815.09, the 20-day EMA.

MNI COMMODITIES: Crude Falls Amid Oversupply Concerns, Precious Metals Extend Gains

- WTI crude prices have fallen on Thursday, with focus on Russia-Ukraine peace talks and oversupply concerns. Bearish pressure was added to by a Bloomberg report that Zelenskiy may be willing to put territorial control over Ukraine’s Donbas to a referendum.

- WTI Jan 26 is down by 1.3% at $57.7/bbl.

- Meanwhile, tensions between the US and Venezuela continue to escalate amid reports that the Trump administration has imposed new sanctions on three nephews of President Maduro and six companies shipping its oil.

- A bearish theme in WTI futures remains intact, with moving average studies in a bear-mode position, highlighting a dominant medium-term downtrend. Key support and the bear trigger lies at $55.99, the Oct 20 low.

- Meanwhile, precious metals have rebounded today, as post-Fed dollar weakness has extended following higher-than-expected jobless claims data.

- Spot gold has risen 1.1% to a 7-week high at $4,276/oz, while silver rose to a fresh all-time high earlier, currently up 3.2% at $63.8/oz.

- Silver has been buoyed by tight physical supply, which has seen a breakdown in the Gold/Silver ratio to its lowest level since May 2021.

- Gold is in consolidation mode, with key resistance and the bull trigger at $4,381.5, the Oct 20 high. Key support to watch is the 50-day EMA, at $4,059.9.

- For silver, the trend unsurprisingly remains bullish, with sights on $64.227 which has been pierced, followed by round number resistance at $65.0.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 12/12/2025 | 0700/0700 | *** | UK Monthly GDP | |

| 12/12/2025 | 0700/0800 | ** | Unemployment | |

| 12/12/2025 | 0700/0700 | ** | Trade Balance | |

| 12/12/2025 | 0700/0700 | ** | Index of Services | |

| 12/12/2025 | 0700/0700 | ** | Index of Production | |

| 12/12/2025 | 0700/0800 | *** | Germany CPI (f) | |

| 12/12/2025 | 0700/0700 | ** | Output in the Construction Industry | |

| 12/12/2025 | 0700/0800 | *** | Germany CPI (f) | |

| 12/12/2025 | 0745/0845 | *** | HICP (f) | |

| 12/12/2025 | 0800/0900 | *** | HICP (f) | |

| 12/12/2025 | 0930/0930 | ** | Bank of England/Ipsos Inflation Attitudes Survey | |

| 12/12/2025 | - | *** | Money Supply | |

| 12/12/2025 | - | *** | Social Financing | |

| 12/12/2025 | - | *** | New Loans | |

| 12/12/2025 | 1300/0800 | Philly Fed's Anna Paulson | ||

| 12/12/2025 | - | ECB de Guindos at ECOFIN Meeting | ||

| 12/12/2025 | 1330/0830 | * | Building Permits | |

| 12/12/2025 | 1330/0830 | ** | Wholesale Trade | |

| 12/12/2025 | 1330/0830 | Cleveland Fed's Beth Hammack | ||

| 12/12/2025 | 1535/1035 | Chicago Fed's Austan Goolsbee | ||

| 12/12/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 12/12/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 12/12/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly |