EU CONSUMER STAPLES: Consumer & Transport: Week in Review

Aug-29 14:34

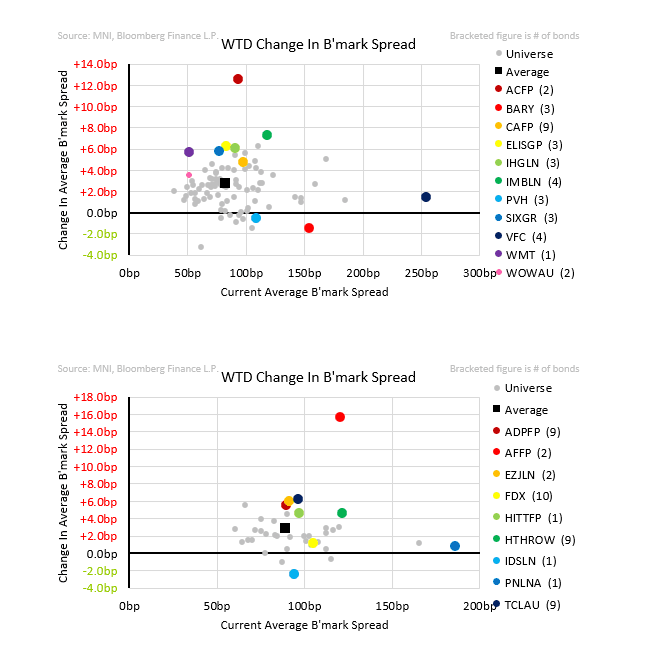

Issuance was skewed to French names all of whose secondary struggled in the aftermath. More broadly widening showed no clear trend, with Yankee high-grade names like Walmart widening same amount as (rich) French names like ADP. Keurig Dr Pepper funding the acquisition of JDE with €16b in debt will leave us with more M&A supply to look forward to this year in consumer.

- JDE Peet’s is acquired by Keurig Dr Pepper in a $23b transaction that will likely see ~16b of supply. We viewed the transaction as credit negative – but subject to revision when it announces capital allocation plans for the planed spin-off of the Coffee-co. Rating agencies were mixed on their views but all are guiding to BBB- ratings for now. If so, it will prevent CoC from being triggered.

- Kering majority owner Pinault may be scouting for buyers of its 29% stake in Puma according to Bloomberg leaks. It may restart concerns if the holding company (Artemis) can service its own debt as Kering’s dividend is cut. It quashed these concerns in late July when a spokesperson for Artemis responded to Reuters with: “it is incorrect to assume that we are dependent on Kering's dividend flows to finance the company. In fact, other companies in the Group pay regular and significant dividends which cover most of our debt servicing needs”.

- Woolworths equities dropped -15% on concerns it is underperforming the mid-single digit growth in key competitor Coles. Selling emerged on the 32s but we see credit impact muted for now. If it continues we will see relative value.

- Scandinavian Tobacco results pointed to LSD growth that was offset by termination of ZYN online distribution in the US. There were indications it is underperforming Cigar market in certain regions. Protection is there with 1.25% coupon step on any HY ratings - Moody’s thus far has been lenient on the above target leverage.

- PVH 2Q stayed on sales growth but with continued gross margin weakness. Guidance is for sales to fall slightly in 3Q and for FY EBIT margin to contract 150bps. Low leverage may leave credit able to look past for it for now but we would stay acute to any deterioration in sales.

- Bunzl reported final 1H results, reiterated FY guidance including for leverage to be at low-end of target and restarted its buyback. Euro-31s continue to price away from ratings.

- Aeroports de Paris is screening rich both against its own government curve (to which it is nearly flat to) and to higher rated airports.

- FedEx unconsented 31s reversed a recent rally after it began pricing over 5pts/100bps for the freight Guarantor. Note on a full sale/spin-off the guarantee would still be lost.

- Primary (NIC in brackets): Elis 6y (+2), Accor 7y (+7), Carrefour 3.25y (+9), Air-France 5y (+5), East-Japan Railway 12y (+2), £20y (-2)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: US EIA: CRUDE OIL STOCKS EX SPR +7.7M TO 426.7M JUL 25 WK

Jul-30 14:30

- US EIA: CRUDE OIL STOCKS EX SPR +7.7M TO 426.7M JUL 25 WK

- US EIA: DISTILLATE STOCKS +3.64M TO 113.5M IN JUL 25 WK

- US EIA: GASOLINE STOCKS -2.72M TO 228.4M IN JUL 25 WK

- US EIA: CUSHING STOCKS +0.69M TO 22.6M BARRELS IN JUL 25 WK

- US EIA: SPR +0.24M TO 402.7M BARRELS IN JUL 25 WK

- US EIA: REFINERY UTILIZATION WEEK CHANGE -0.1% TO 95.4% IN JUL 25 WK

GBP: Acceleration of GBP Correction Exposes 1.3140 in Near-term

Jul-30 14:11

- GBP breaking down further in recent trade - evident in both the GBP/USD slippage to new lows as well as the sharp intraday bounce in EUR/GBP. As such, the slippage in GBP/USD through support (namely at 1.3365-70) isn't just a USD story, and shows the correction in GBP may have legs into next week's BoE decision.

- The 15-min candle chart shows the downtick accelerating on the break of the trendline drawn off the Jul18 low, exposing the more major of 1.3140 in the near-term.

- A renewed phase of USD strength could provide the next catalyst here - particularly with the FOMC and NFP risks due today and Friday. Today's market moves show the happiness with which FX will react to positive data surprises, and the break and close above the 50-dma this week in the USD Index has cleared the major technical hurdle to a constructive recovery. That level helped characterize the downtrend this year - adding to the importance of this week's break.

GILTS: Resistance In Futures Intact, 10s In Middle Of Multi-Month Range

Jul-30 14:07

Post-U.S. data weakness in Tsys weighs on gilts, leaving the July 22 high in futures (92.15) intact, back to 91.75 from session highs of 92.11.

- The contract remains in a bit of a holding pattern between that resistance point and the bear trigger (91.08).

- Yields 1-2bp lower on the day, 10s outperform on the curve.

- 10s trade around the middle of the rough 4.40-4.80% range in play since early February.

- Spillover from Tuesday’s extension higher in Tsys, solid demand at this morning’s long end gilt tender and some focus on comfortably larger than average month-end extension projections had provided support for gilts ahead of the U.S. data.

- Gilts still outperform Bunds by ~2.5bp on the day and are also 7bp stronger vs. Tsys at the 10-Year point.

- Short end pricing little changed on the day, showing ~47bp of cuts through year-end.

- Lower tier Lloyd’s business barometer data is due overnight, but that won’t be a market mover.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Aug-25 | 3.993 | -22.4 |

Sep-25 | 3.962 | -25.5 |

Nov-25 | 3.812 | -40.5 |

Dec-25 | 3.755 | -46.2 |

Feb-26 | 3.650 | -56.7 |

Mar-26 | 3.618 | -59.9 |