EU CONSUMER STAPLES: Scandinavian Tobacco: 2Q Results

Aug-27 16:44

(STGDC; Baa3/NR)

2Q EBITDA margin comes in weak and is half on gross margin weakness, half rising staff costs. Guidance still points to positive FCF post dividend and lease payments this year but will still leave it with limited firepower to manage the rise in leverage towards 2.9-3.0x (on falling earnings). The 29s are protected with a 1.25% step-up if it is moved into HY - effective from the interest payment date (annual in September) following a downgrade. Moody's has thus far been very lenient (on stable outlook) as it notes last year saw acquisition spend and elevated equity pay-outs which pushed leverage away from co's 2.5x target.

- 2Q sales organic -4%, net of acquisitions unch at DKK 2.4b (€322m)

- Handmade Cigars +1%, Machine Rolled +3% while small (4% of group) next-gen exposure was -25% on discontinuation of ZYN online distribution in the US.

- adj. EBITDA DKK499m -14% y/y on a 21.1% margin (-340bps). Adjustments of -35m into statutory. Gross margin at 45.0% (-190bps) - rest of the margin headwind was from a opex increase of +4% mainly on staff costs that were +15%.

- FCF net of lease payments this half was 229m (vs. -70m LY) on better WC (80m), tax (160m), lower capex (-40m) and acquisition spend (-80m) - all that helped offset the fall in earnings.

- Reporting net debt of 5.7b, up from 5.4b at 1H last year. Levered 2.9x vs. 2.6x LY. Targets <2.5x.

- Has prefunded the 25s which it has tendered down to €113.5m (DKK 847m).

- Ended the half with DKK 70m of cash on hand. Note the annual dividend payment (DKK 670m) would have weighed on it this half. No buybacks done (vs. 434m in 1H LY).

- Implied guidance is pointing to near doubling in 2H FCF.

FY guidance unch for:

- revenue 9.1-9.5b (vs. 9.2b LY or +1 to -3% y/y)

- adj. EBITDA margin of 18-22% (vs. 22.6% LY)

- YTD it is running at 18.8% (vs. 21.2% LY)

- FCF ex. acquisitions of 0.8-1.0b (vs. 0.9b LY)

- YTD it is reporting 0.275b

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SOFR OPTIONS: Midday Two-Way Trade

Jul-28 16:36

- -20,000 SFRZ5 95.25/95.62/96.12 call flys, 6.5

- -2,000 0QZ5 96.75 straddles 31.0 over 0QH6 97.12 calls ref 96.75/0.35%

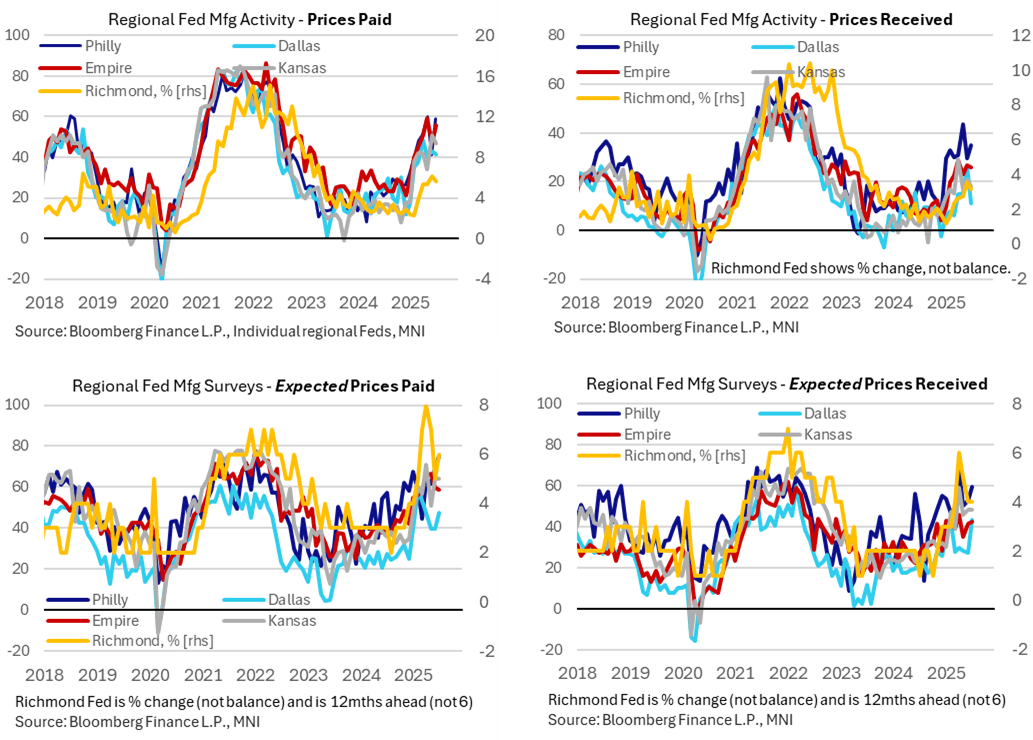

US DATA: Mixed Ability Of Firms To Pass Cost Increases On In Dallas Fed District

Jul-28 16:18

- The improvement in the Dallas Fed manufacturing survey for July came despite an apparent relative re-compression in margins although this in turn was countered by the opposite when looking six months out.

- The prices paid index remained at an elevated 41.7 after 43.0 in June (average of 43.5 since Apr 2 reciprocal tariff announcements, 30 in 1Q25 and 21 in 2024) but prices received dropped from 26.1 to 11.1 for the lowest since March (average 16.8 since Apr, 7 in 1Q25 and 7 in 2024).

- Countering this, the six-months ahead measures saw a marked increase in expectations for prices received with its highest since April 2022. The 43.2 compares with an average of 32 since April, 35 in 1Q25 and 21 in 2024.

- That said, whilst this uptick in expected prices received was a marked rise on the month, it’s only really catching up with relative levels seen in other regional Fed manufacturing surveys – see charts.

- Of course, whilst a particularly timely survey with a collection period of Jul 15-23, it still predates the US-EU deal made over the weekend with a 15% tariff rate on most EU goods (with the EU being the US’s largest source of imports).

US TSYS/SUPPLY: Preview 5Y Auction

Jul-28 16:15

- Tsy futures remain near mid-morning lows (FVU5 -3.5 at 108-04.25 vs. 108-03.5; TYU5 currently -6.5 at 110-25 vs. 110-24.5 low) ahead of the $70B 5Y note auction (91282CNN7) at 1300ET, WI is currently running at 3.981%, 10.2bp cheap to last month's tail.

- June auction recap: Tsy futures retreated slightly (FVU5 to 108-20.75 from 108-21.5) after the $70B 5Y note auction (91282CNK3) tailed: 3.879% high yield vs. 3.872% WI; 2.36x bid-to-cover vs. 2.39x prior (5 auction average).

- Peripheral stats: Indirect take-up retreated to 64.68% from 78.4% prior, directs bounced to 24.44% vs. 12.4% prior (5 auction low), primary dealer take-up at 10.88% vs. 9.2% prior.