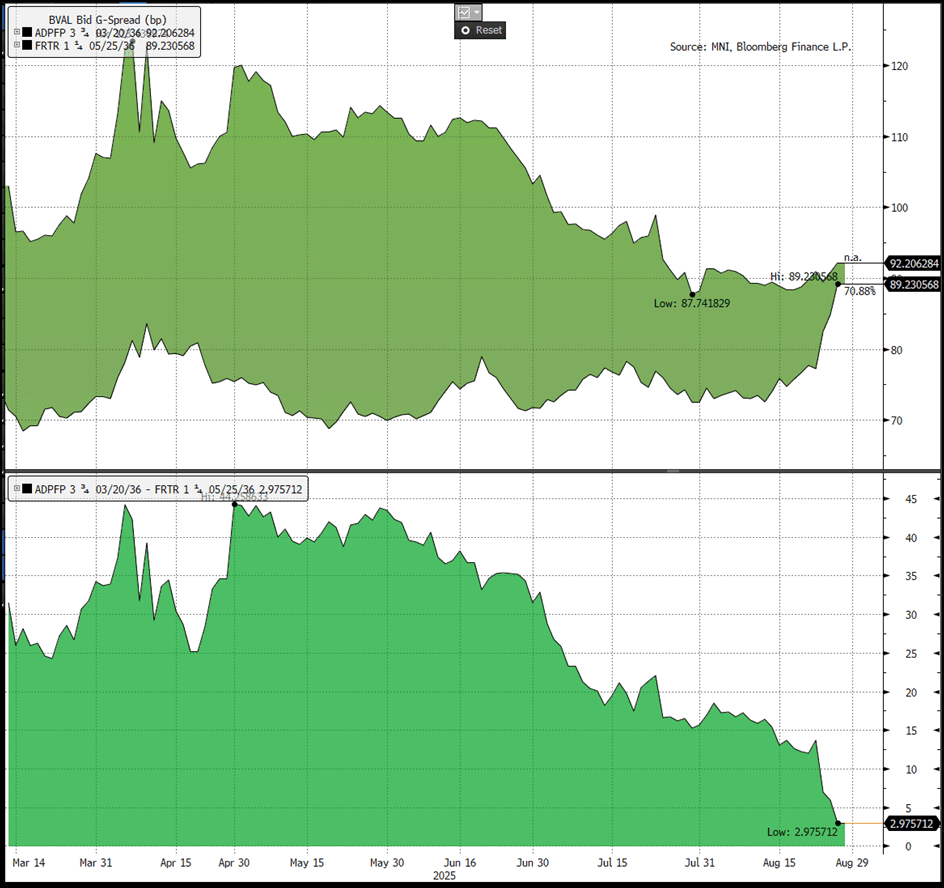

EU TRANSPORTATION: Aeroports de Paris; RV vs. OATs

(ADPFP; NR/A-/BBB+)

French corp's have held quiet resilient through the OAT sell off this week. Among the more surprising is the new ADP 11y that is now nearly flat to French Govvies despite 3-4 notch lower rating. It does have circa 20% of its earnings outside France through a 46% stake in Turkish operator TAV (contributes 26% of EBTIDA when fully consolidated) and a 46% economic stake in Indian operator GMR Airports (recorded under equity intertest but would add another 25% to group EBITDA if fully consolidated). Earnings are fine with HSD growth guiding to drive small deleveraging.

ADP long-end also screens rich vs. higher rated airports (like Norwegian state owned Avinor 34s).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

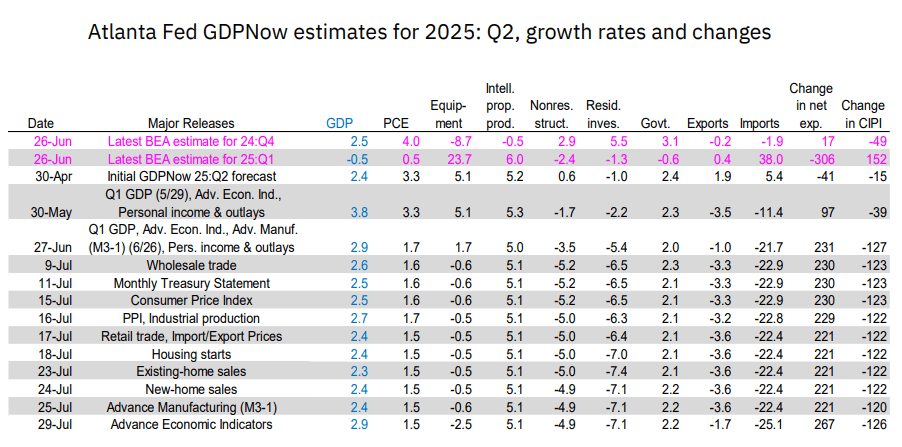

US OUTLOOK/OPINION: Final GDPNow Estimate Picks Up, But Weaker Domestic Demand

The Atlanta Fed's final GDPNow estimate for Q2 GDP has risen to 2.9% from the prior 2.4% estimate made last week, due entirely to today's trade data which showed a smaller-than-expected goods trade deficit for June. This estimate is above the 2.5% currently seen by Bloomberg consensus for Wednesday's official GDP release.

- Net exports are now seen by the Atlanta Fed model as contributing 4.0 percentage points to Q2 growth, vs 3.3pp in last week's estimate and almost a complete reversal of Q1's 4.6pp subtraction. Indeed we noted after the advance trade data for June that "Q2 tracking could be revised higher after today’s June release".

- However, the final reading is a little weaker on the underlying domestic demand front: equipment investment is now seen falling 2.5% in real terms, the weakest estimate of the quarter (vs -0.6% as of last week, the initial forecast of +5.1% and Q1's +23.7%).

- Indeed when netting out inventories (seen subtracting a little more after today's data, at -2.2pp vs -2.1pp prior and +2.6pp in Q1), real domestic final sales, which is more closely watched by the Fed than the headline GDP reading, is estimated to print 1.1% Q/Q SAAR, down from 1.2% last week (and after 1.5% in Q1). That would be the weakest since Q3 2022.

- When netting out government's contribution to growth (0.4pp), that's seen at closer to 0.7% Q/Q SAAR, after 1.6% in Q1 - which would be the weakest since Q4 2022.

US TSY FUTURES: BLOCK: Sep'25 5Y Sale

- -5,000 FVU5 108-09.75, sell through 108-10 post-time bid at 1024:34ET, DV01 $213,000

- The 5Y contract trades 108-10 last (+5.5)

GILT AUCTION PREVIEW: On offer next week

The DMO has announced it will be looking to sell GBP4.5bln of the 4.50% Mar-35 Gilt (ISIN: GB00BT7J0027) at its auction next Tuesday, August 5.