EU TRANSPORTATION: FedEx: 31s still moving

Aug-28 07:24

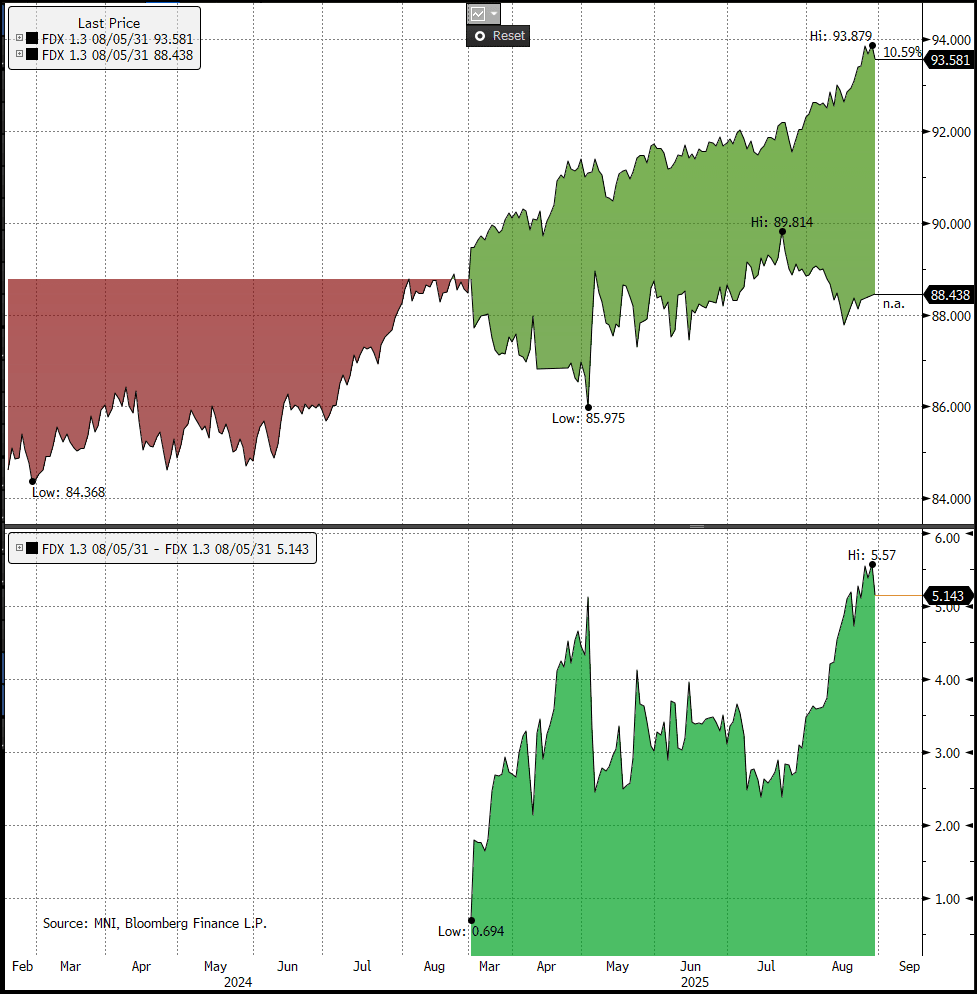

(FDX: Baa2/BBB)

- FDX unconsented €355m 31s are -0.3pt/+12bps cheaper this morning. Outside the €1.25b 27s, it is the only other line we see with Freight guarantee post a partial (but not full) spin-off.

- MWC is at greater than par or B+25 (will be par).

- There is 5pt/100bps currently priced for the guarantor/chance of clean up.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURIBOR: Record Volume day in the Calendar spread Yesterday

Jul-29 07:21

- We noted some notable early flow in the Blue (Euribor) ERH9/M9 calendar spread, being sold down to 4.5 from a 5.5 record high printed last Week, and also a massive day in the ERM7/U7 spread seller at 7.5.

- While the Volume is those Calendar spreads are non existent today, the chart clearly shows a record day in the ERM7/ERU7 Yesterday.

- Also note that plenty more were done on legs, so not showing in that total outright volume.

(Chart source: Bloomberg Finance LLP/MNI).

STIR: Trendline Support In ERH6 Holds

Jul-29 07:17

Euribor futures are -0.5 to -2.0 ticks through the blues, unwinding a little of yesterday’s recovery. We wrote last week that ERH6 had bounced off trendline support drawn from the May 2024 low, and this level continues to underpin price action in the contract.

- Although the US-EU agreement struck over the weekend should reduce near-term trade policy uncertainty, a 15% near-universal tariff rate is still a net-negative to the growth outlook, and more severe than the ECB’s June macroeconomic projection baseline.

- The MNI Policy Team latest sources piece, released yesterday, suggested the ECB’s hawkish shift following its last Governing Council meeting is more limited than markets’ reaction would suggest, particularly given the weekend’s trade deal, Eurosystem national central bank sources told MNI, admitting that while there is a new mood music it has been overinterpreted…. sources told MNI there is still a strong possibility of a further 25-basis-point cut, even if most Governing Council members would now need to see a deterioration in the outlook for this to occur.

- ECB-dated OIS continue to lean in favour of one more 25bp cut this cycle, with 16bps of easing priced through December.

- Spanish GDP was stronger-than-expected at 0.7% Q/Q (vs 0.6% cons and prior). The ECB’s June consumer expectations survey is due at 0900BST.

| Meeting Date | ESTR ECB-Dated OIS (%) | Difference Vs. Current Effective ESTR Rate (bp) |

| Sep-25 | 1.885 | -3.8 |

| Oct-25 | 1.849 | -7.4 |

| Dec-25 | 1.762 | -16.1 |

| Feb-26 | 1.742 | -18.1 |

| Mar-26 | 1.710 | -21.3 |

| Apr-26 | 1.710 | -21.3 |

| Jun-26 | 1.713 | -21.0 |

| Jul-26 | 1.715 | -20.8 |

| Source: MNI/Bloomberg Finance L.P. | ||

SONIA: Large Basis Trade

Jul-29 07:02

Large Sonia Basis trade, helps explain the Volume at that Expiry.

- SFIM7 10k at 96.42.

Trending Top

Jan-30 21:43

Jan-30 21:11