EU CONSUMER CYCLICALS: Consumer & Transport: Week in Review

Compression took a pause in-line with broader index weakness but seems continuing strength in fund flows was enough to send primary in another direction; new Levi’s are -25 through our FV, El-Corte Ingles -14 through. These names are heading through comp’s we would clearly see as firmer risk and well through levels their shorter bonds were trading at only a few months ago. Perhaps supporting this sentiment though, earnings are generally coming in firm and pointing to a supportive macro backdrop. That is also leaving underperformers standing out and punished in both equity/credit markets. A return of M&A news this week sees Couche-Tard supply risk disappearing while we may be able to look forward to Flutter & Air-France supply. Notable earnings next week include Edenred, Groupe SEB, Wizz, LVMH, Carrefour and Loomis.

- Couche-Tard gives up on attempting to acquire its biggest US competitor, 7-Eleven. Equities and credit take a reprieve rally on the over $47b acquisition disappearing.

- Kering faces leaks it is attempting to exit its 30% Valentino stake (and hence contracts that may force it to buy the remaining 70% next year). They are swiftly denied by the counterparty to those option contracts, and current majority holder, Qatari Investment Fund Mayhoola.

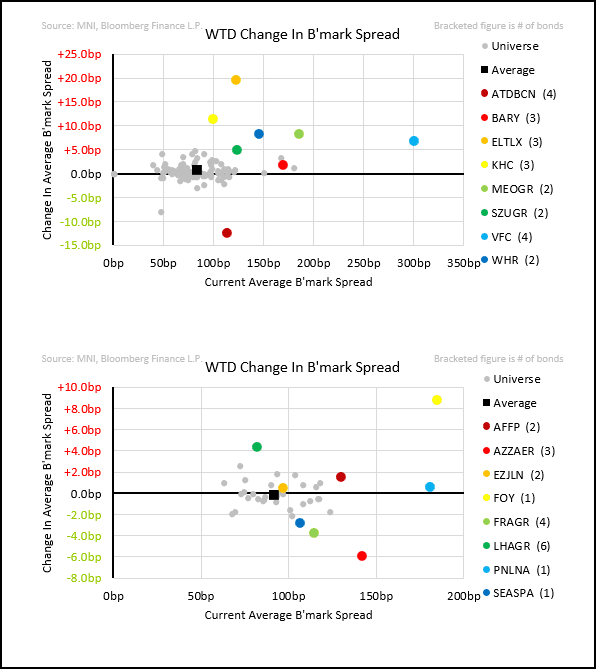

- Kraft Heinz is considering carving out 40% of its business according to the WSJ. We see no protective covenants under that scenario for the closer to, or above, par lines across €/£.

- Air France-KLM agreement to upsize Scandinavian Airlines stake to 61% leftt S&P unfazed. Unlike management, S&P disclose SAS net debt position of €2.1-2.2b, and sees debt funding coming.

- Flutter was stabilised (from positive outlook) at S&P - as expected after last week’s Fanduel buyout. S&P sees refi for $1.75b bridge facility arriving in the “coming weeks” (across bonds and loans).

- Reckitt divested 14% of its business for ~£1.7b in upfront cash and plans to send all proceeds to equity holders. Despite the shrinking business it has ambitious margin targets.

- B&M hit all-time lows as the pace of LFL growth through favourable Easter timing fails to satisfy markets. New CEO is still warming up in his role.

- Electrolux headline growth disappointed markets that were expecting a turnaround at a faster pace. Margin expansion will still support leverage cycling down – though unfavourable WC swing is acting as a (likely temporary) headwind to that.

- Richemont continues to report firm results while running a sizeable net cash position.

- Experian results remain strong, stock hits all time highs.

- Burberry results continue to point to a swift stabilisation under a new CEO

- easyJet results are supported by falling fuel prices and continued strong growth in Holidays business. That may leave the seemingly tight 31s unphased (for now).

- Primary (NIC in brackets): El Corte Ingles (-1), Levi 5NC2 (-10), Next PLC £-26s Tender (136.4/250m, all accepted).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILT AUCTION PREVIEW: On offer next week

The DMO has announced it will be looking to sell GBP3.25bln of the 4.375% Jan-40 Gilt (ISIN: GB00BQC82D08) at its auction next Wednesday, June 25.

MNI: US EIA: CRUDE OIL STOCKS EX SPR -11.47M TO 420.9M JUN 13 WK

- US EIA: CRUDE OIL STOCKS EX SPR -11.47M TO 420.9M JUN 13 WK

- US EIA: DISTILLATE STOCKS +0.51M TO 109.4M IN JUN 13 WK

- US EIA: GASOLINE STOCKS +0.21M TO 230.0M IN JUN 13 WK

- US EIA: CUSHING STOCKS -1M TO 22.7M BARRELS IN JUN 13 WK

- US EIA: SPR +0.23M TO 402.3M BARRELS IN JUN 13 WK

- US EIA: REFINERY UTILIZATION WEEK CHANGE -1.1% TO 93.2% IN JUN 13 WK

OPTIONS: Expiries for Jun19 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1415-25(E2.4bln), $1.1475-00(E2.5bln), $1.1510-20(E629mln), $1.1545-50(E1.2bln), $1.1585-00(E3.2bln)

- GBP/USD: $1.3500(Gbp511mln)

- EUR/GBP: Gbp0.8600(E519mln)

- EUR/JPY: Y161.90-00(E981mln)

- AUD/USD: $0.6460(A$741mln), $0.6550(A$683mln), $0.6600(A$1.1bln)