EU CONSUMER CYCLICALS: Burberry: 1Q (to June) results

(Baa3 Neg/NR)

UK capital markets showing efficiency - old CEO with questionable strategy was shown the door only 1-year ago, Josh Shulman was parachuted in and has (nearly) stabilised sales. That has helped equities double and £30s rally -120bps (note junking risk remains). Between Richemont & Burberry, excuses to blame Macro for luxury seem non-existent this quarter.

- 1Q LFL sales -1%, store space another -1% and FX -4% leaving net revenue at £433m, -6% y/y.

- On LFL, APAC -4%, China -5%, EMEIA +1%, Americas +4%

- APAC incl. China is half for Burberry, EMEIA 30%, Americas 22% (US 19%)

- Guidance is light outside a commitment to deliver "margin improvement"

- Unless it commits to paying down the £300m Sept-25s (had £700m in cash on hand), it is still looking at a likely Moody's Junking (ended March gross 3.8x levered vs. Moody's 3.0x threshold). Positive FCF is also a condition for Moody's - it came in at+£65m last year but was boosted on inventory clean-up/WC swing (+£75m). If that normalises this year there will be some offset from pullback in Capex (guiding to -£20m less at £130m), rest contingent on operating performance which is light on guidance.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

RIKSBANK: Early Analyst Views On June Decision and Rate Path

Early analyst views suggest the June MPR rate path is consistent with a 50% chance of another rate cut this year. In Q3, there is a larger chance of a move in September compared to the interim meeting in August.

Nordea: “According to our calculations, the rate path has only a minor bias, some 2bp, for an additional rate cut in August. Thus, a rate cut in August seems unlikely. The probability for a rate cut in Q3 is somewhat larger at around 5-8bp, or around 20-30%”.

- “The inflation forecast is revised downwards and is well in line with our view. The Riksbank sees some uncertainty regarding inflation in the near term, which probably is a reason why the bank is not in a hurry to cut rates again”.

- “The Riksbank has a bias for a rate cut, but it is later this year. In our view, the economic recovery will continue, reducing the need for additional rate cuts. In addition, inflation is close enough to 2% target next year and the ECB is probably done cutting rate cuts, suggesting that the Riksbank’s policy rate will bottom out at 2.0%, we think”.

SEB: “The rate forecast indicates 12bps lower policy rate later this year (which equals almost 50% probability for a rate cut)”….“ Also, the rate path indicates a small (3bps) probability for a rate cut already at the next meeting in August”.

- “In our opinion, the slightly more dovish message is sufficient to tip the scales, and we therefore lower our policy rate forecast and predict another rate cut to 1.75% later this year. A rate cut in September seems to be the most likely scenario, but we will listen to the press conference for more details regarding the timing. The forecasts for growth and inflation were lowered largely in line with our expectations”.

Swedbank: “We estimate that the rate path roughly translates to a likelihood of roughly 10% at the August meeting, 25% for a cut at the September meeting, while the total probability of another rate cut this year is around 50%”.

- “The Riksbank not only revised down their forecast for inflation, but also noted that price dispersion has decreased and that there are fewer driving forces now which – when they abate – implies lower inflation ahead”.

- “We expect macro data and indicators to remain weak this summer and that the Riksbank therefore will cut the policy rate again in September to 1.75%. Today’s communication indicates lower tolerance for economic underperformance and hence increases the likelihood of further monetary policy easing beyond September”.

SOFR OPTIONS: SFRH6 96.50/97.00/98.00 Broken Call Fly Lifted

SFRH6 96.50/97.00/98.00 broken call fly vs. 96.375 paper paid 2.5 on 5.5K all day.

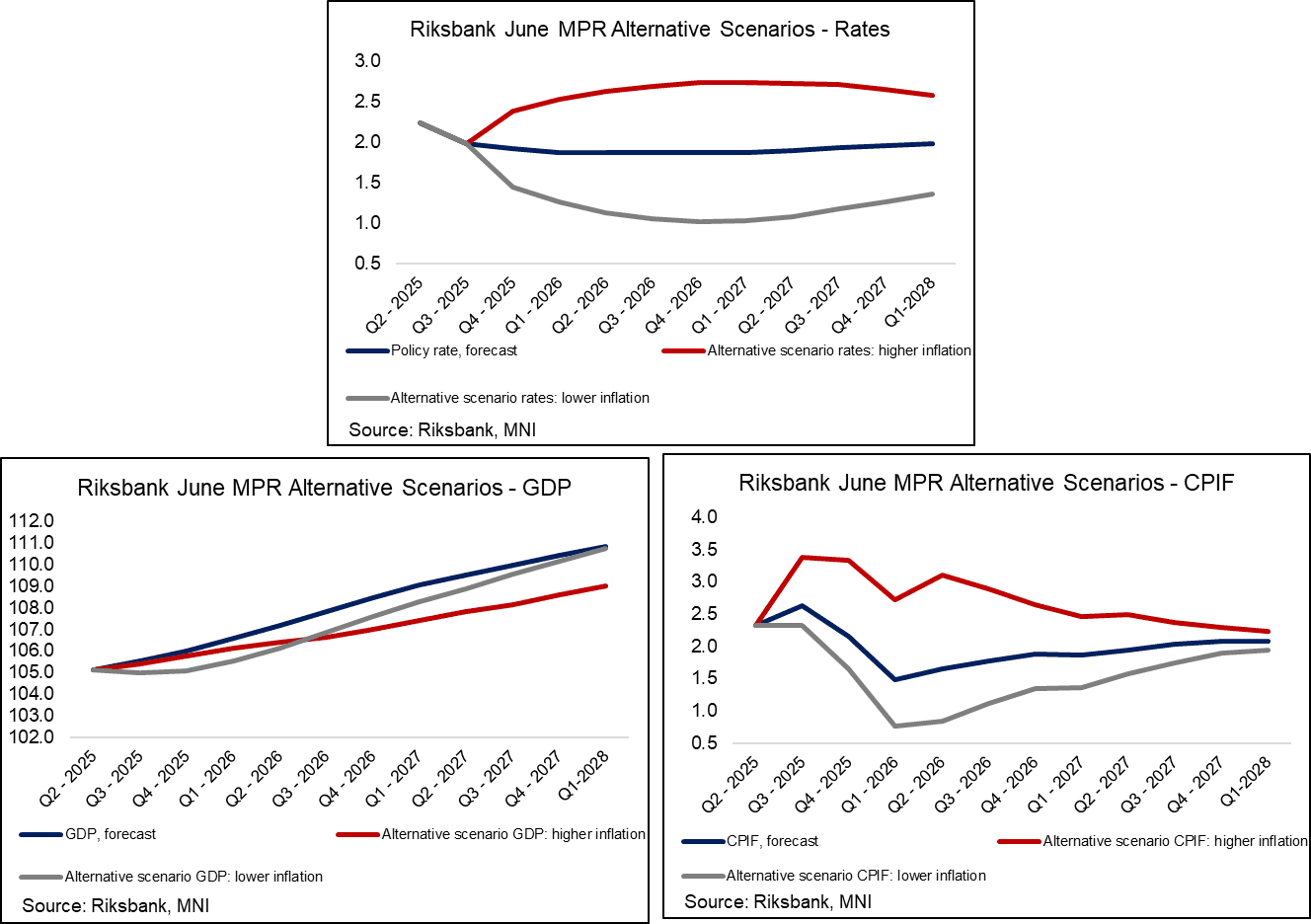

RIKSBANK: Alternative Scenarios: Rates Trough At 1% In Dovish Scenario

- As usual, the June MPR contains alternative scenarios. In the dovish scenario, "increased uncertainty could dampen demand and lead to lower inflation" and rates are seen troughing around 1% in late 2026. In the hawkish scenario, "large and widespread trade conflict caused prices to rise rapidly", and rates are seen peaking at 2.75% in early 2027. Notably, the hawkish scenario is one of stagflation, where the level of GDP is permanently below the baseline and dovish scenario in the latter half of the forecast horizon.

- Upside scenario: “It is assumed in the scenario that several of the ongoing negotiations between the United States and its trading partners will fail to reach an agreement”...” These measures will in turn lead to counter measures”

- “During the third quarter of this year, rising commodity prices and tariffs entail significant cost increases on many goods that are imported to Sweden,”.

- “The Riksbank begins to tighten monetary policy as early as September”…“During 2026, the policy rate is therefore raised on one further occasion”

- Downside scenario: “It is assumed that the uncertainty regarding the trade conflict and the security policy situation will gradually lead to increasingly large falls in confidence among households and companies. The effects on economic activity will become clear during the third quarter of this year”

- “At the same time, the krona exchange rate appreciates”

- “Because of the weak inflation outlook and the weak resource utilisation, the Riksbank will pursue a more expansionary monetary policy during the fourth quarter. The policy rate will then continue to be lowered in 2026”.

- Despite the dovish leaning nature of the decision, the Riksbank still notes that “the probability that inflation will be higher than in the forecast is assessed as roughly the same as the probability that it will be lower”.

- The Riksbank also gives an early opinion on the latest Israeli/Iran escalation: “Even though the [oil] price increase is not insignificant the impact on the inflation outlook is expected to be limited. In a scenario where the conflict in the Middle East escalates further, with a larger increase in oil prices, the consequences for energy prices in Sweden are also likely to be greater. In such a scenario, the economic outlook would also be affected and the Riksbank would then need to assess the overall effects on Swedish inflationary pressures.”