AUSSIE 10-YEAR TECHS: (Z5) Returns Lower

- RES 3: 95.982 - 76.4% retracement Sep’24 - Nov’24 downleg

- RES 2: 95.960 - High Apr 7 (cont.)

- RES 1: 95.900 - High Oct 17

- PRICE: 95.745 @ 15:25 GMT Oct 29

- SUP 1: 95.510 - Low Sep 3

- SUP 2: 95.415/95.300 - Low May 15 / Low Jan 14

- SUP 3: 95.275 - Low Nov 14 (cont) and a key support

Aussie 10-yr futures slipped lower Wednesday on the back of hotter-than-expected Australian inflation. This returned prices lower despite nascent signs of a technical recovery as recently as last week. The sustainability of the pullback will be dependent on prices holding above key short-term support at 95.510, the Sep 3 low. Near-term resistance remains 95.780, the Sep 12 high. A clear break of this level signals scope for a continuation higher and opens 95.960, the 76.4% retracement level for the Sep’24 - Nov’24 downleg.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: UK SEP BRC SHOP PRICES +0.2% M/M, +1.4% Y/Y

- MNI: UK SEP BRC SHOP PRICES +0.2% M/M, +1.4% Y/Y

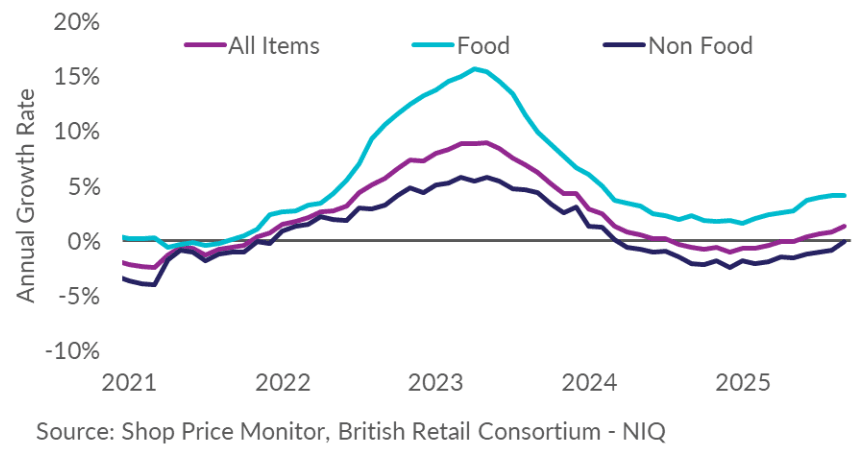

UK DATA: BRC Sep Shop Prices: Non-food Back to Flat, Food Inflation Remains High

September BRC Shop Price data showed an increase of 1.4% Y/Y (vs 0.9% Aug). The month-on-month rate is 0.2%, unchanged from August. The data continues to show strong food inflation, while non-food inflation has returned to be close to unchanged on a year-on-year basis after having been more deflationary for a number of months.

- Food inflation was 4.2% Y/Y, unchanged from August, a touch above the 3-month average of 4.1%. The M/M figure was 0.2%, down 0.2ppt from August.

- The press release notes that, despite the unchanged figure, "increased labour and energy costs continue to push up input prices for many farmers, particularly of cattle, with dairy and beef prices remaining high."

- Non-food inflation rose to -0.1% Y/Y (vs -0.8% Aug) and 0.3% M/M (vs 0.0% Aug). DIY and gardening saw price rises, whereas some back-to-school-related categories continued to fall due to promotions ahead of the new school year.

- Given the much smaller range of goods accounted for in the data compared to the ONS's CPI basket, any indication of what might happen in September's headline inflation print should be taken with caution.

- The data covers the retail prices of 500 commonly-bought high street products between 1 - 7 September 2025.

BONDS: NZGBS: Richer With US Tsys After US Gov Shutdown Buoys

In local morning trade, NZGBs are 3bps richer after US tsys finished Monday’s session 2-5bps stronger, with a flatter curve.

- US Government shutdown concerns buoy Tsys into the close. The Bureau of Labor Statistics' key economic releases would be postponed in the event of a government shutdown, per the Department of Labor's plan for such an event.

- Bloomberg - "RBNZ Proposes Expanding Use of Word 'Bank' to More Lenders. RBNZ issues a consultation paper that proposes expanding the use of the word 'bank' to all deposit takers that become licensed under the Deposit Takers Act, the central bank says in a statement."

- MNI - The ANZ business survey for September is released on Tuesday. T he activity assessment compared to a year ago is an important signal for GDP in the quarter. Business confidence and the activity outlook are off the May lows, following the announcement of US tariffs, but remain below the Q4 2024 peak. The price/cost components are also important to monitor.

- RBNZ dated OIS pricing is showing 32bps of easing for October, with a cumulative 61bps by November 2025.

- On Thursday, the NZ Treasury plans to sell NZ$250mn of the 4.50% May-30 bond and NZ$200mn of the 4.50% May-35 bond.