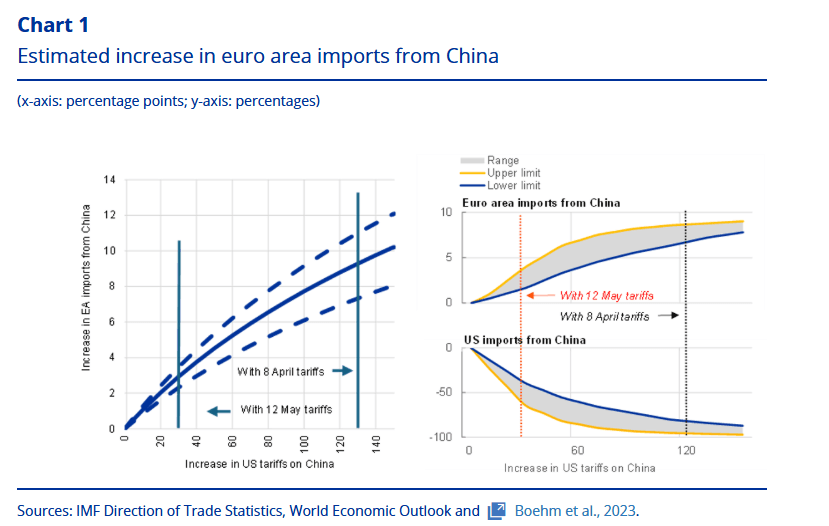

ECB: Worst Case Scenario Of Chinese Trade Diversion Would Reduce HICP By 0.15pp

An ECB staff blog, published today, suggests a 10% increase in Euro area imports from China under a severe trade scenario could reduce non-energy industrial goods inflation by 0.5pp in 2026, impliyng a negative peak impact on headline HICP inflation of 0.15pp. The estimates are based on the same severe trade scenario outlined in the June macroeconomic projections, where the US effective tariff rate on Chinese goods is 135%. Of course, the current effective tariff rate is closer to ~30% following the May 12 trade agreement, which looks to have been extended for another 90 days after talks between the US and China in Stockholm this week. As such, the estimates should be considered a worst case scenario, not a forecast based on current conditions.

- Staff note that the Euro area could be more impacted by Chinese trade diversion at present compared to 2018 due to:

- A similar composition of Chinese exports to the US and the EU

- "Established supply chain links, which have expanded since the last China-US trade war, and ongoing industrial upgrades in China facilitate the redirection of trade flows"

- "Chinese businesses have laid the groundwork to facilitate faster market entry."

- "The depreciation of the Chinese renminbi makes Chinese goods cheaper and more attractive for European importers."

- "Many [Chinese] firms, especially those in final goods production, still have room to absorb reduced profit margins".

- Following a 10% rise in Chinese imports, "assuming that domestic demand remains the same in the short term, this increase in imports would result in an excess supply of goods equivalent to 1.3% of overall goods consumption. For consumers to absorb this additional volume of imported goods – either by replacing other imports or substituting domestic production – the prices of Chinese imports would need to decrease. Specifically, our calculations indicate that lower Chinese import prices would reduce overall import prices by 1.6%."

- "But it will take some time for consumer prices to drop. While stronger supply from China may trigger a swift decline in import prices, consumer prices for non-energy industrial goods (NEIG) tend to respond more gradually, with the strongest impact materialising one to one-and-a-half years after the initial shock".

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

LOOK AHEAD: Monday Data Calendar: MNI Connect Event - Atlanta Fed Bostic Outlook

- US Data/Speaker Calendar (prior, estimate)

- 06/30 0945 MNI Chicago PMI (40.5, 42.9)

- 06/30 1000 Atlanta Fed Bostic economic outlook at MNI event (no text, Q&A)

- 06/30 1030 Dallas Fed Manf. Activity (-15.3, -12.0)

- 06/30 1130 US Tsy $79B 13W & $71B 26W bill auctions

- 06/30 1300 Chicago Fed Goolsbee moderated discussion at Aspen Ideas Festival

- Source: Bloomberg Finance L.P. / MNI

US TSY FUTURES: Net Short Setting Most Prominent On Friday

OI data points to net short setting dominating on Friday, with the most prominent positioning adjustment coming in WN futures (~$3.1mn DV01).

- Modest net long cover was seen in FV & US futures.

| 27-Jun-25 | 26-Jun-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,269,109 | 4,253,499 | +15,610 | +603,799 |

FV | 7,116,709 | 7,119,040 | -2,331 | -101,770 |

TY | 5,037,897 | 5,016,950 | +20,947 | +1,399,846 |

UXY | 2,411,409 | 2,404,834 | +6,575 | +580,670 |

US | 1,758,599 | 1,760,182 | -1,583 | -200,474 |

WN | 1,904,272 | 1,887,316 | +16,956 | +3,103,720 |

|

| Total | +56,174 | +5,385,792 |

US 10YR FUTURE TECHS: (U5) Holding On To Its Recent Gains

- RES 4: 114-14 High Apr 7 and key resistance

- RES 3: 113-07 76.4% retracement of the Apr 7 - 11 bear leg

- RES 2: 112-23 High May 1 and key resistance

- RES 1: 112-04+ High May 2

- PRICE: 111-31 @ 11:16 BST Jun 30

- SUP 1: 111-11+/110-27 Low Jun 25 / 50-day EMA

- SUP 2: 110-10+/109-28 Low Jun 16 / Low Jun 6 / 11

- SUP 3: 109-12+ Low May 22 and the bear trigger

- SUP 4: 109-09+ Low Apr 11 and key support

Treasury futures traded higher last week and the contract is holding on to its gains. Resistance at 111-14+, the Jun 5 high and 61.8% of the May 1 - 22 downleg, has been cleared. The break strengthens a bullish cycle. Note too that last Thursday’s gains delivered a print above 111-30, 76.4% of the May 1-22 downleg. A clear break of this level would strengthen current conditions. Initial pivot support to watch lies at 110-27, the 50-day EMA.