AUSTRALIA DATA: Vacancies May Have Resumed Downtrend

Apr-03 01:23

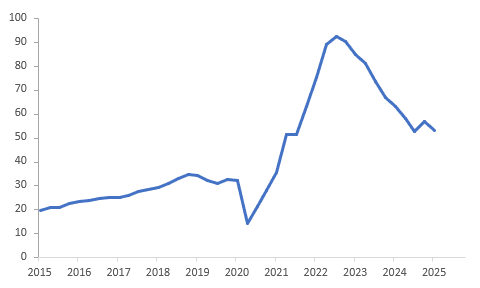

Q1 job vacancies fell 4.5% q/q following an upwardly-revised 5.2% q/q rise in Q4. It resulted in a 3.5pp drop in the vacancies/unemployment ratio, which signals an easing in the jobs market but it remains well above the historical average. The RBA said this week that “labour market conditions remain tight” and specifically mentioned “relatively low” underutilisation.

- The vacancy ratio fell to 53.4% from 57% in Q4, but was still above Q3’s 52.6%. It is now down almost 40pp from Q3 2022 peak of 92.7%. Q2 will indicate if the downtrend that stalled at the end of 2024 has resumed.

- Vacancies fell every quarter from Q3 2022 to Q4 2024 and the 4.5% drop in Q1 may suggest that was a blip. However, the RBA said in its April statement that surveys and its liaison “suggest that availability of labour is still a constraint for a range of employers”.

- The ABS said that the drop in February employment was due to fewer older workers returning to work. The fall in vacancies tentatively suggests that maybe some of their roles are not being refilled.

Australia job vacancies/unemployment %

Source: MNI - Market News/Refinitiv

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: CHINA PBOC CONDUCTS CNY38.2 BLN VIA 7-DAY REVERSE REPO TUES

Mar-04 01:23

- CHINA PBOC CONDUCTS CNY38.2 BLN VIA 7-DAY REVERSE REPO TUES

CHINA: USD/CNY Fixing Steady, Fixing Error Slightly Lower

Mar-04 01:20

The USD/CNY fix printed at 7.1739, versus a BBG market consensus of 7.2782

- Today's fixing outcome is little changed versus yesterday’s outcome. The fixing error was marginally better at -1043pips.

- The fixing error has taken the bulk of the USD gains in terms of the higher market fixing estimate today.

- The authorities appear to be willing to continue to support the domestic economy with the regulator will boost availability of financing channels for private and small firms.

- Markets are on NPC watch as it begins this week and there are high expectations for potential monetary and fiscal announcements.

- USD/CNH traded briefly through 7.30 in early trading, before settling at 7.2989.

AUSSIE BONDS: Richer & At Session Bests After Domestic Data & RBA Minutes

Mar-04 01:18

ACGBs (YM +7.0 & XM +7.0) are sharply stronger and at Sydney session highs after the release of the February RBA Meeting Minutes.

- "If the evolving data signalled that inflation was proving more persistent than expected, it would be reasonable to maintain a more restrictive stance of policy by holding the cash rate at 4.1 per cent for an extended period – given members’ assessment that this level would still be restrictive – or by even tightening policy if the outlook was for inflation to rise materially. On balance, members judged that accepting the risk of needing to adopt such a course of action was preferable to accepting the risk of holding interest rates high for too long.” (per RBA)

- Retail sales rose 0.3% m/m (estimate +0.3%) in January versus -0.1% in December.

- The current account deficit narrowed to A$12.547bn (estimate -A$12.0bn) in Q4 from a revised -A$13.885bn in Q3. Net exports from GDP was +0.2 ppts.

- Cash US tsys are 1-4bps richer, with a steepening bias, in today’s Asia-Pac session after yesterday’s solid gains.

- Cash ACGBs are 7bps richer with the AU-US 10-year yield differential at +13bps.

- Swap rates are 6-7bps lower.

- The bills strip has bull-flattened, with pricing +1 to +9.