AUSSIE 10-YEAR TECHS: (U5) Spikes With Treasuries

- RES 3: 96.501 - 76.4% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 2: 96.207 - 61.8% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 1: 95.960 - High Apr 7

- PRICE: 95.710 @ 15:52 BST Aug 12

- SUP 1: 95.415/95.300 - Low May 15 / Low Jan 14

- SUP 2: 95.275 - Low Nov 14 (cont) and a key support

- SUP 3: 94.707 - 1.0% 10-dma envelope

Aussie 10-yr futures received a boost from the US Treasury rally that followed both the recent poor NFP print as well as Tuesday’s inflation number. This keeps Aussie 10-year futures toward the top end of the recent range. To the upside, next resistance is at 96.207, a Fibonacci retracement point. Next support undercuts at 95.420 (pierced), the Feb 13 low, ahead of 95.275, the Nov 14 low and a key support. Clearance of this level would strengthen a bearish condition.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

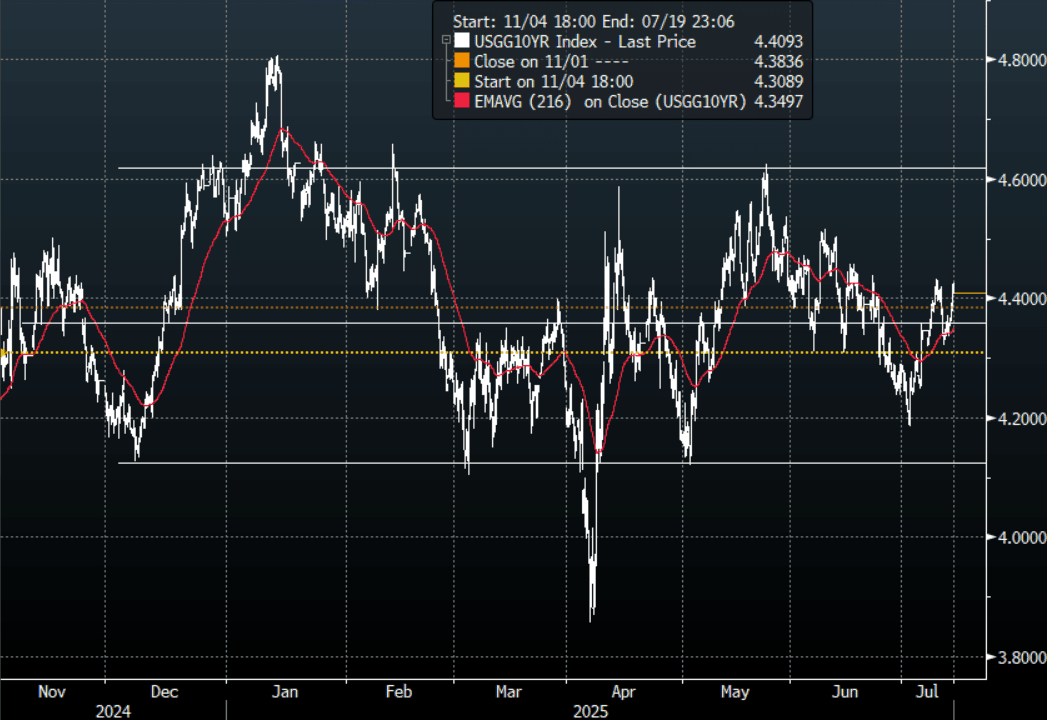

US TSYS: Yields Move Higher On Inflation Concerns, Led By The Long-End

TYU5 reopens at 110-26, up 0-03 from closing levels in today’s Asia-Pac session.

- Friday night the US 10-year yield had a range of 4.3577% - 4.4253%, closing around 4.41%.

- Treasury yields tested higher on Friday night on inflation fears; this was led by the long-end which saw the yield curve steepen (2s10s +4.46 at 52.016, 5s30s +4.11 at 97.462).

- MNI FED: Chicago's Goolsbee: Latest Tariffs Require Caution. Chicago Fed President. Goolsbee tells the Wall Street Journal in an interview Friday that this week's latest round of tariff announcements could force him and the FOMC to wait for longer before having enough clarity to cut rates.

- MNI US INFLATION: CPI Seen Picking Up In June, Core Goods Eyed For Early Tariff Hit. June CPI is the highlight of next week's US data slate, with MNI's early roundup of analyst expectations showing an anticipated acceleration in the main measures of inflation. Both core and headline CPI are seen rising to the mid 0.20s% M/M, from May's readings of 0.13% for core and 0.08% for headline.

- The 10-year yield is again testing the 4.40/45% pivot with its wider 4.10% - 4.65% range. The market is clearly worried about inflation and the CPI this week will be a critical input into the market's thinking. A sustained close back above the 4.45% area could see more longs pared back, above here and the focus will turn back to the 4.60% area.

Fig 1: 10-Year US Yield Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

USD: J.P. Morgan Expects More USD Downside

The global bank expects more USD weakness, it updates its FX forecasts and some key trade recommendations below.

J.P. Morgan: "Look for more USD weakness predicated on the same combination of cyclical (US moderation, tariffs) and structural (valuations, fiscal, flow dynamics, policy uncertainty) factors we’ve been flagging.

Some signals have become less USD-bearish or even bullish, which could signal consolidation in the near term, but we consider these less relevant over the medium term. The underlying macro landscape is undergoing a significant shift, which means model dislocations can get larger.

Stay bullish on EUR/USD and cyclical G10 FX (Antipodeans vs USD, Scandis vs EUR). Tactically neutral on EM FX while maintaining a medium-term more constructive stance. The risk of broad and outsized tariffs has resurfaced; if implemented, they pose global growth risks not priced and would result in defensives outperforming (CHF, JPY). Stay long JPY and initiate new CHF longs.

G10 Key targets: EUR/USD 3Q 1.19 (1.17) to signal still-bullish view; 1.22 peak unchanged. GBP downgraded on weak domestic data and renewed focus on fiscal. EUR/GBP 0.89 (0.87); GBP/USD 4Q 1.36 (1.40). USD/JPY 1y 139, AUD/USD 0.68 both unchanged.

EM: USD/CNY 1y 7.10, USD/BRL 5.75, USD/MXN 19.40 (all unchanged). HUF upgraded and favoured in CEE; EUR/HUF 385 (400)

New trade : Buy CHF vs GBP, EUR basket."

USD: Goldman Sachs Maintains Bearish USD Outlook

The global bank weighs in on the USD backdrop, maintaining a bearish stance, with US firms and households expected to pay for tariff outcomes. It also looks at drivers of the dollar to different type of tariff announcements. See below for more details.

Goldman Sachs: "USD: Return to sender. A key underpinning to our bearish Dollar outlook is that US firms and households will pay for the majority of the tariffs, which will weigh on US relative performance. This, together with broader policy uncertainty, will lead investors to reduce their exposure to US Dollars. Recent research from our US economists confirms that US firms have shouldered much of the load so far, even if the proportions and timing have been a little different than in the first trade war, and we will get a fresh update on how these proportions are evolving with next week’s CPI release. The imposition on the US is likely to be even clearer for some of the sectoral tariffs being initiated now, as tariffs on harder-to-substitute goods are likely to weigh on US terms of trade, which is consistent with the initial copper market reaction. We attribute the muted (and, arguably, backwards) market reaction to the Letters to two factors. First, and most importantly, market participants—and our economists—mostly do not expect these tariffs to go into effect. After seeing the pattern several times already this year, markets have likely determined that the rates being floated are too high to sustain, and so have mostly abstained from the self-defeating cycle of tighter financial conditions and policy backtracking. Second, the initial market reactions were consistent with prior episodes where bilateral trade disputes boosted the Dollar against specific trading partners. This is consistent with our framework that the FX market reaction is different when the US is negotiating with one country at a time rather than the whole world at once. If broad tariff rate hikes are implemented once again, we think the Dollar reaction would be negative again. We expect that over time this will reinforce the perception that US policy direction has made it more difficult for firms to operate and foreigners to invest. This is consistent with FX performance so far this year, where flows have played an outsized role, and faster Fed cuts together with the Dollar’s positive correlation with risk could lead to an even broader shifting in FX hedging and portfolio allocations."