EU CONSUMER STAPLES: Suedzucker; 1H results

(SZUGR; Baa3/BBB-)

We see leverage including est. factoring rising from net 3.1x to 4.9x and interest cover dropping to low 1-handle. But we still see FCF small positive mainly on WC efficiencies and factoring. Longer term fundamentals are harder to call - Sudz is exposed to various commodity prices, some like Ethanol that are very volatile, and with cost side pressures that we do not have visibility on. The €32s are German retail bonds; precedent from Metro’s €29s shows they can trade with little regard for fundamentals until an actual junking. Metro’s results on 19 May made the downgrade obvious, yet the bonds rallied another 20bps into the double-notch junking a month later, before widening 45bps (all vs. index). On that note, we see only negative outlooks for now, not junkings. If one were to occur today, we see 30–40bps of widening.

6m to Aug:

- revenue €4.2b (-18%), EBITDA €189m (-55%), adj. EBIT €42m (vs. €269m LY) and net of restructuring expenses €1m (vs. €286m LY)

EBITDA by segment - Sugar: -€50m (vs. €120m LY) on falling sugar prices (lower revenue)

- Special Products: €115m (vs. €150m LY) on 'significantly higher costs'

- Fruit: €87m (vs. €70m LY) on higher prices for fruit juice concentrates (higher revenue)

- Starch: €29m (vs. €43 LY) on higher raw material costs and lower selling prices

- CropEnergies: €4m (vs. €40m LY) on maintenance work impacting revenue and lower ethanol prices

- WC +€197m vs. -€31m LY and includes +€518m reduction in trade receivables mainly benefiting from its factoring programme (selling receivables to banks for immediate cash)

- FCF was breakeven (vs. +€72m LY), net of dividends and debt repayments it saw cash outflow of -€113m.

- net debt ex hybrid at €1.7b, still down from the €2b this time LY (again on benefit of factoring)

- incl. hybrid at 50% €2b

- incl. factoring we est. €2.45b. S&P does add back factoring as debt. Co hasn't disclosed exact amount for 1H but we assume €400m total (€235m was recorded to end LY, clear indication pace has picked up since).

Recently cut FY guidance left unch as expected:

- Group EBITDA €450-570m vs. €723m LY

- Group EBIT €100-200m vs. €350m LY

- Sugar loss of -€150 to -€250m expected as fundamentals remain weak into new sugar year (failing to support the price recovery it expected)

- reported net debt (ex. hybrid) to be largely unch y/y

Some asides:

- FY guidance still holds - but looking at slightly below the midpoint (implies EBITDA <€510m). Not large enough though that it needs to change.

- Net 3.5x is comfort level/soft target. Clear commitment for IG rating. Solution: cost cutting and trying to decrease capex - but latter not easy as it has contracts in place it says.

- Was reporting net 2.4x in FY25. On €500m EBITDA and unch debt load (per guidance) will move to 3.4x

- We see it net 3.1x rising to 4.9x (incl. hybrid + est. factoring)

- €200m in cost savings within 3 years, €100m for sugar within 2 years

- Says high Cocoa prices, and hence lower chocolate demand driving lower sugar demand

- Says removal of cash flow trigger on Hybrid was part of "modernising" the capital structure

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OUTLOOK: Price Signal Summary - Bear Threat In Oil Futures Remains Present

- On the commodity front, Gold remains in a clear bull cycle and last week’s gains plus this week’s bullish start to the week, reinforce current conditions. The yellow metal has traded to a fresh all-time high. The break also confirms a resumption of the primary uptrend and an extension of the sequence of higher highs and higher lows. The next objective is $3674.8, A 2.382 projection of the Dec 30 ’24 - Apr 3 - 7 price swing. Initial firm support lies at $3474.7, the 20-day EMA.

- In the oil space, the trend condition in WTI futures is unchanged - a bear cycle remains intact. The pullback from the Sep 2 high highlights a possible reversal and the end of the corrective phase. Initial resistance to watch is $66.03, the Sep 2 high. Key short-term resistance has been defined at $69.36, the Jul 30 high. A stronger resumption of weakness would pave the way for a move towards $57.71, the May 30 low.

US TSY FUTURES: BLOCK: Dec'25 2Y Buy

- +4,000 TUZ5 104-12.62, buy through 104-12.5 post time offer at 0713:00ET, DV01 $163,200.

- The 2Y contract trades 104-12.5 last (-.62)

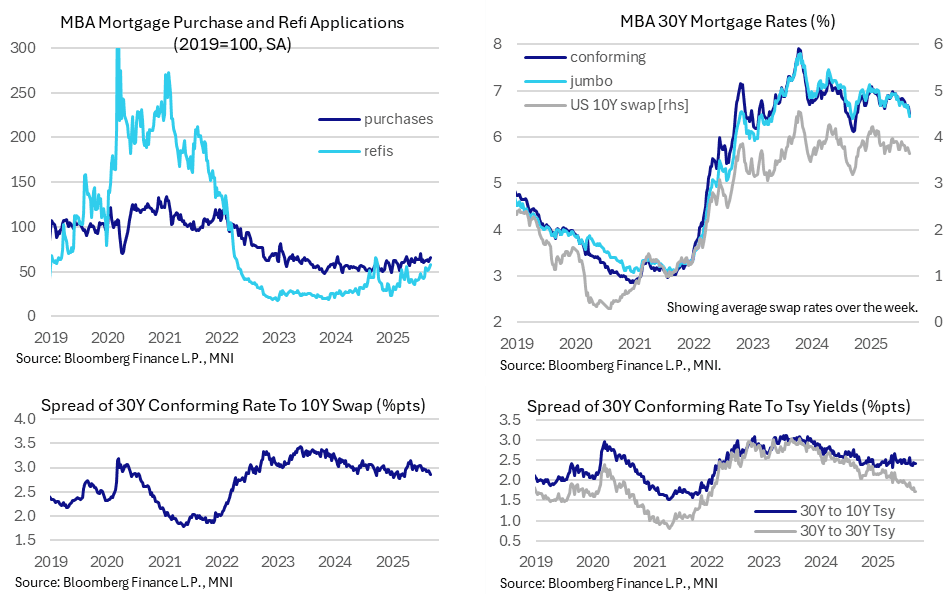

US DATA: Mortgage Applications See A Latest Step Higher On Rates Drop

MBA mortgage applications saw some traction from lower rates last week, with the level of composite applications at its highest since mid-2022 after 30Y mortgage rates fell 15bp to the lowest since Oct 2024.

- MBA composite mortgage applications stepped 9.2% higher last week (sa), following three small declines that had only chipped away at a solid 11% increase earlier in August.

- It was led by refis rising 12% M/M, but as opposed to that early Aug 11% increase when refis jumped 23%, there was a more broad-based contribution with new purchase applications rising 6.6% (vs 1.4% in that previous composite step higher).

- Bear in mind still very subdued levels relative to 2019 averages though: composite 63% (highest since Jul 2022), new purchases 65% and refis 58%.

- The push to new recent highs followed a sizeable drop in the 30Y conforming mortgage rate to 6.49% (-15bps) for a 35bp decline since mid-July and its lowest level since Oct 2024.

- The decline in mortgage rates exceeded the 7bp decline in the average 10Y swap rate over the week, pushing the 30Y mortgage to 10Y swap rate spread down to 285bp.

- That’s the tightest spread since reciprocal tariffs were first announced in early April at which point it widened to 315bp in the month that followed and then held around 300bp +/-5bp for some time. It’s also coincidentally back to where it averaged through 1Q25.

- Note that this follows US Tsy Sec Bessent in recent weeks talking on wanting to keep the spread between mortgage rates and treasuries flat or even bring it down.